Africa Tech Rising — 2026-05-08

African startup funding raced toward the $1 billion mark in the first half of 2026, with $887 million raised across four months despite a 51% drop in deal volume driven largely by debt financing. Nigerian fintech BFREE secured a new growth round to scale its distressed-credit business, while new data confirms April 2026 saw the lowest monthly funding in 12 months at $110 million across just 32 startups. A broader trend is emerging: local African investors now fund nearly 40% of all tech investment on the continent, and debt is increasingly displacing equity as the dominant capital instrument.

Top Stories

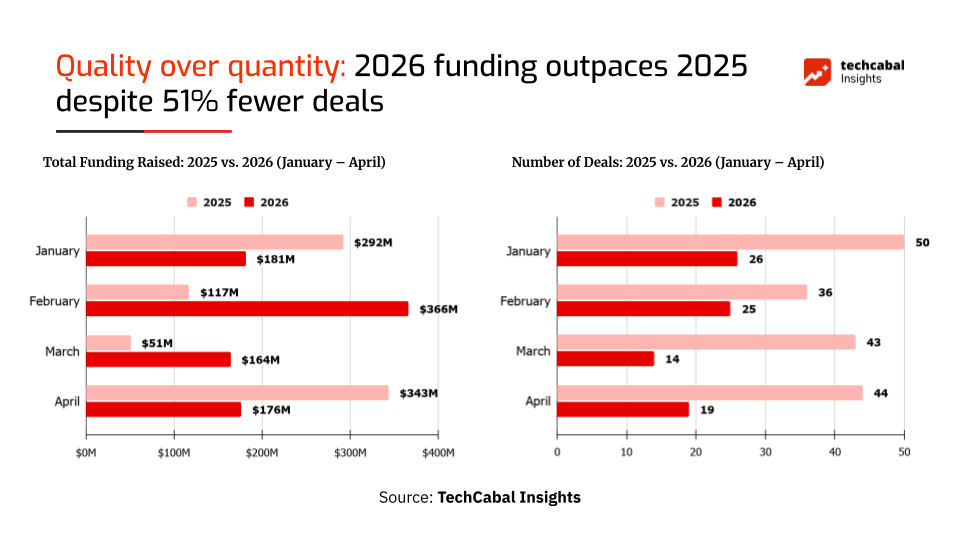

African Startup Funding 2026: The $1B Race — With Half the Deals

- What happened: African startups raised $887 million across four months (January–April 2026), putting H1 on track to potentially cross the $1 billion threshold, according to TechCabal Insights. However, deal volume has collapsed by 51% compared to the same period in 2025. Debt financing is the primary driver of the surge in dollar value.

- Why it matters: The gap between rising capital volumes and shrinking deal counts signals that large-ticket debt rounds are masking a difficult fundraising environment for early-stage founders. The structural shift toward debt may reshape how African startups think about capital access and growth strategy.

April 2026 Was the Worst Month for African Startup Funding in a Year

- What happened: Only 32 African startups raised a combined $110 million in April 2026, making it the lowest monthly total in the past 12 months, according to Technext24. Despite the low volume, more startups than usual appear to have received smaller checks compared to prior months.

- Why it matters: The April dip underscores the persistent pressure on deal activity even as aggregate dollar figures trend upward. Founders seeking early-stage capital face a difficult market, while investors concentrate capital into fewer, larger transactions.

Nigerian Fintech BFREE Secures Growth Round to Scale Distressed Credit Business

- What happened: Nigerian fintech startup BFREE has closed a new growth round to expand its ability to purchase non-performing loan (NPL) portfolios and deepen partnerships with lenders across the continent. The company is now expanding its presence beyond Nigeria.

- Why it matters: BFREE's raise signals growing investor appetite for credit infrastructure plays in Africa — a segment that has historically been underfunded. As more African consumers take on formal debt, the market for distressed-credit resolution is expected to grow significantly.

Funding Tracker

- BFREE (Nigeria) — Undisclosed growth round: Nigerian fintech focused on acquiring and managing non-performing loan portfolios; expanding partnerships with banks and lenders across Africa.

Fewer than three individual funding rounds were confirmed published after May 1, 2026. Broader ecosystem context: New VC funds launched in early 2026 — including Partech Africa II, VestedWorld, and Mirova Gigaton — have each logged only two deals in the period, suggesting a slow deployment pace from newer vehicles. This deployment lag is contributing to the deal-count slump even as aggregate capital from debt instruments remains elevated.

Sector Spotlight: Fintech — Moving Beyond Payments Into Credit and Infrastructure

Africa's fintech sector is entering a new phase. While payments infrastructure powered the first decade of African fintech growth, credit, financial services, and distressed-debt resolution are emerging as the next major frontier. Nigeria, Kenya, and Egypt have each intensified regulatory efforts to promote digital capital markets and wealthtech, according to fintech leaders surveyed in early 2026. Africa remains the world's fastest-growing fintech market by revenue, with projections pointing to a nearly 13-fold expansion to approximately $65 billion by 2030. The BFREE raise and the rising dominance of debt financing in Africa's startup ecosystem both reflect this structural shift toward more sophisticated financial plumbing.

Policy & Regulation

New VC Funds Are Missing in Action — A Signal About Market Confidence

A new analysis from Launch Base Africa published May 6, 2026, finds that Africa's newly launched VC funds — including Partech Africa II, VestedWorld, and Mirova Gigaton — have been conspicuously absent from early 2026 dealmaking, each logging only two deals. This pattern suggests fund managers are taking a cautious stance, potentially waiting for clearer macroeconomic signals or more favorable deal valuations before deploying capital at scale. For founders, this translates to fewer active check-writers in the market even as headline fundraising numbers appear robust. The business impact is direct: deal scarcity at the early stage, while large debt tranches inflate the aggregate figures.

Ecosystem Pulse

-

Local investors now fund ~40% of African tech: Since 2023, African investors have become an increasingly important source of capital for local startups, accounting for nearly 40% of total funding — up from 25% — as global investors continue to pull back. This localization trend is reshaping deal terms and investor expectations across the continent.

-

Six reasons African fintech startups shut down: A new analysis published May 6, 2026, breaks down the most common failure modes for African fintech companies, using real case studies and ecosystem data. Regulatory friction, premature scaling, and thin unit economics top the list.

What to Watch

-

Will H1 2026 cross $1 billion? With $887 million raised in just four months, the milestone is within reach — but deal velocity needs to recover from April's 12-month low for the number to mean anything structurally positive for the ecosystem.

-

Deployment pace of new African VC funds: Partech Africa II, VestedWorld, and Mirova Gigaton have all launched but remain largely on the sidelines. Watch for their first major deals in Q2 2026 as indicators of market confidence and sector priorities.

-

Debt financing normalization: As debt displaces equity across the continent, founders and investors alike are navigating new structures — revenue-based financing, asset-backed lending, and NPL acquisitions. The BFREE model may become a template others follow as Africa's credit infrastructure matures.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by