Industrial/Supply Chain Daily Update — 2026-05-06

Markets saw a broad rally today with the S&P 500 up 0.81% to 7,259.22, but supply chains are reeling after a CMA CGM container ship was hit in the Strait of Hormuz. G7 trade ministers have gathered for emergency talks on critical mineral supply chains, while new data shows a 25% quarterly surge in global semiconductor sales.

Industrial/Supply Chain Daily Update — 2026-05-06

1. Commodities Market Trends

-

Crude Oil (WTI/Brent): Oil futures remain under tension as the supply shock triggered by the war with Iran persists. Since the blockade of the Strait of Hormuz began, 8.2 billion barrels of inventory have been depleted, creating a dual-price structure where spot prices significantly exceed futures benchmarks.

-

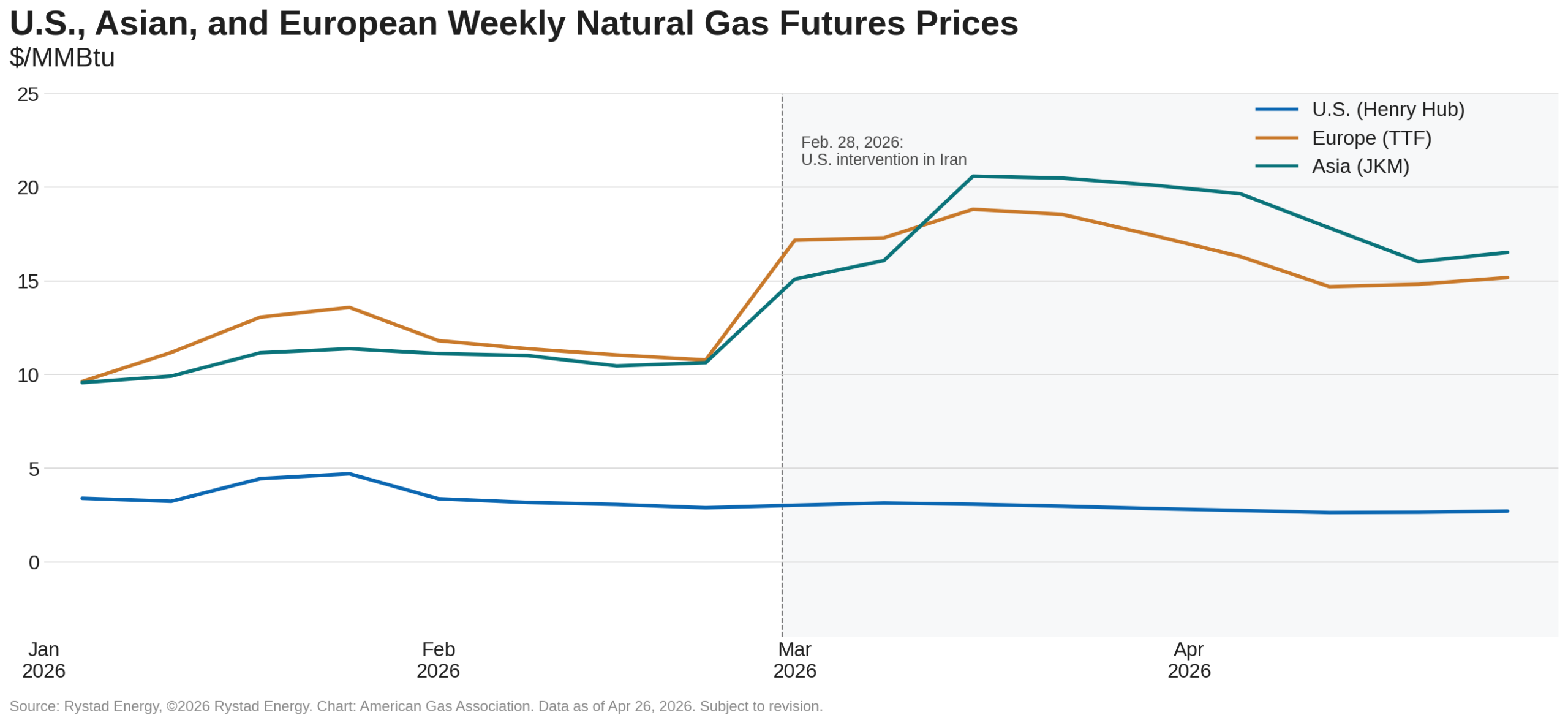

Natural Gas / LNG: The U.S. natural gas market is seeing prices trade sideways after Henry Hub futures hit a 5-month low of $2.63 per MMBtu due to the shoulder season. Upward pressure is limited as domestic demand softens and storage replenishment intensifies.

-

Industrial Metals (Copper, Aluminum, Iron Ore): Supply chain disruptions linked to the war with Iran continue to drive up global factory input costs. While Reuters real-time agricultural data shows declines in major commodities like CBOT corn (-0.97%), CBOT wheat (-1.01%), and MDX palm oil (-0.69%), industrial metals including iron ore are feeling the squeeze from logistics bottlenecks.

-

Battery Metals (Lithium, Nickel, Cobalt): Battery storage capacity is seeing record growth, with AI data centers emerging as a major new demand source. Despite increased investment in U.S.-based battery storage production by automakers, dependence on Chinese cells remains high.

2. Supply Chain Issues

-

CMA CGM Ship Hit in Hormuz: A CMA CGM container ship was hit in the Strait of Hormuz on May 6, 2026, resulting in crew injuries. With 8.2 billion barrels of global oil reserves already drained during the two-month blockade, this incident further escalates maritime logistics instability.

-

G7 Trade Ministers Discuss Critical Minerals: A French minister confirmed on May 6 that the security of critical mineral supply chains is a top agenda item at the G7 trade ministers' meeting in Paris. This indicates that China’s export control risks are now a priority security issue for G7 nations.

-

AI Chip Supply Delays and Data Center Bottlenecks: A combination of physical and geopolitical constraints is deepening the AI chip shortage. Bruce Bateman, a senior analyst at Omdia, warned of a "perfect storm" of surging AI demand and supply constraints, noting that data center construction schedules are facing cascading delays.

3. Core Industry Trends

Semiconductors

- Global Sales Surge 25%: According to the latest quarterly data from the Semiconductor Industry Association (SIA), global chip sales jumped 25% between Q4 2025 and Q1 2026, driven by AI demand and data center expansion.

- China Accelerates Localization: Major Chinese automakers are preparing to launch models with 100% domestically-produced chips starting in 2026. China's current domestic share in non-power and discrete automotive semiconductors is only 5-10%, but it is growing rapidly.

Batteries & EVs

- Chinese EV Exports Surge Amid Oil Crisis: Chinese EV exports are spiking due to the oil crisis sparked by the war with Iran. However, the Atlantic Council has warned that the internet connectivity in these vehicles poses cyber vulnerabilities, placing importing countries in a dilemma.

- U.S. Battery Production Grows, But Reliance on China Persists: Despite increased investment in U.S. storage production, developers remain reliant on imported cells, facing ongoing tariff and policy risks. AI data center power demand is becoming a new growth driver for the storage market.

Automotive, Shipbuilding & Steel

- Vestas Q1 Operating Profit Beats Expectations: Wind turbine manufacturer Vestas announced that its Q1 2026 operating profit significantly beat forecasts, driven by increased offshore turbine production—a sign of recovery in the energy transition supply chain.

- European Solar Entering Over-Supply Phase: Oversupply of solar energy in Europe is pushing the power system into a complex new transition phase, highlighting the urgent need for battery storage investment to stabilize the grid.

4. Corporate Moves

- CMA CGM: Following the incident in the Strait of Hormuz, the company faces rising insurance premiums and potential rerouting costs for global logistics.

- Vestas: Reported Q1 2026 results that exceeded market expectations, confirming that the renewable energy supply chain remains resilient despite the global energy crisis.

- Ahold Delhaize: The Dutch-Belgian supermarket chain beat quarterly operating profit expectations thanks to strong results from its U.S. division, which helped offset the negative impact of a weaker dollar.

5. Insight for Today

The attack on the CMA CGM ship in the Strait of Hormuz underscores the fragility of global supply chains. With 8.2 billion barrels of oil reserves exhausted during the two-month blockade, the energy price signaling mechanism is effectively paralyzed by the widening gap between spot and futures prices. The G7's focus on critical minerals suggests that Middle East risks are evolving into a "multi-crisis" affecting semiconductors and batteries as well. As AI data centers drive demand for power, supply chain vulnerabilities are deepening, even as global semiconductor sales reach new heights.

6. What to Watch Next

- G7 Outcomes: Monitor the results and any joint statements from the G7 trade ministers' meeting regarding critical mineral supply chains.

- Hormuz Tension & Oil Inventory: Keep an eye on U.S.-Iran negotiations and the spread between oil spot and futures prices following the attack.

- European Solar/Battery Policy: Watch for EU announcements on battery storage and grid stabilization, which may impact related raw materials and company stocks.

7. Reader Action Items

- Secure Alternative Routes: Supply chain managers for Middle Eastern goods should urgently verify options for bypassing the Cape of Good Hope and review transport insurance terms.

- Diversify Battery/Semiconductor Suppliers: Procurement teams should accelerate the diversification of their supplier portfolios and initiate long-term supply contract negotiations to mitigate China-dependency and bottleneck risks.

- Prepare for G7 Policy Shifts: Investors and procurement teams should prepare for price volatility in lithium, cobalt, and rare earths, and adjust hedging strategies based on upcoming G7 announcements regarding mineral export controls or stockpiling.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by