Industry & Raw Material Supply Chain Daily Briefing — 2026-05-05

The Hormuz Strait blockade, triggered by the conflict with Iran, continues, pushing average U.S. gasoline prices to a record $4.45 per gallon. While Chinese EV exports are surging amid the oil crisis, cybersecurity concerns are creating a dilemma for importing nations. Global semiconductor sales have jumped 25% from the previous quarter, raising fears of supply chain bottlenecks fueled by AI demand.

Industry & Raw Material Supply Chain Daily Briefing — 2026-05-05

1. Commodities Market Trends

-

Crude Oil (WTI/Brent): Oil prices have hit a four-year high as the Hormuz Strait remains blockaded for approximately two months due to the war with Iran. It is reported that 8.2 billion barrels of inventory have been depleted so far, with Asian countries bearing the brunt of the supply shortage. Ahead of the summer driving season, the average U.S. gasoline price reached a record $4.45 per gallon, up $1.28 from the same period last year.

-

Natural Gas / LNG: Reuters reported that surging U.S. energy exports, combined with rising domestic fuel prices, are leading to increased social scrutiny. Pressures to reorganize the LNG supply chain are intensifying amid rising tensions in the Middle East.

-

Industrial Metals (Copper, Aluminum, Iron Ore): Reuters reported on May 5 that an explosion at Kazakhstan’s largest zinc smelter resulted in two deaths. The market is closely watching for potential disruptions to zinc production. Volatility persists across raw material supply chains due to Middle East tensions.

-

Battery Metals (Lithium, Nickel, Cobalt): According to the World Bank’s latest commodity outlook, energy prices are expected to surge 24% this year due to the aftermath of the Middle East war. This is likely to drive up production costs for battery metals, with indirect impacts expected on lithium and cobalt supply chains.

2. Supply Chain Issues

-

Hormuz Strait Blockade Enters 2nd Month — Global Supply Chain Crisis Deepens: The U.S. and Iran are at odds over control of the Hormuz Strait, with peace talks in the Middle East remaining uncertain. While Asia has been the primary victim of oil shortages thus far, warnings are emerging that Europe could become the next target of the supply crisis as inventories deplete.

-

Surge in Chinese EV Exports — The Cybersecurity Dilemma: Amid the oil crisis, exports of Chinese electric vehicles are skyrocketing globally. However, the Atlantic Council analyzed on May 5 that the cybersecurity vulnerabilities inherent in internet-connected vehicles are creating a dilemma for importing countries between trade and energy security.

-

Semiconductor Supply — Bottlenecks Intensify Amid AI Demand and Geopolitical Clashes: Global semiconductor sales surged 25% in the first quarter of 2026 compared to the fourth quarter of 2025. Analysts suggest a "perfect storm" of supply crises is becoming reality due to the intersection of explosive AI demand and geopolitical constraints. Shortages of medical-grade helium continue to affect semiconductor manufacturing processes.

3. Core Industry Trends

Semiconductors

-

Global Semiconductor Sales Jump 25% (Q4 2025 → Q1 2026): Reports citing the latest data from the Semiconductor Industry Association (SIA) show a 25% quarterly surge in global semiconductor revenue due to the AI boom. However, as supply fails to keep pace with demand, delays in data center deployments are becoming apparent.

-

AI Chip Supply Bottleneck — The 'Era of Data Center Delays': Bruce Bateman, senior analyst at Omdia, warned that AI chip shortages have become a reality as physical and geopolitical constraints act in tandem. Rare earth shortages and increased automotive demand are pressuring the availability of semiconductor components across the board.

Secondary Batteries and EVs

-

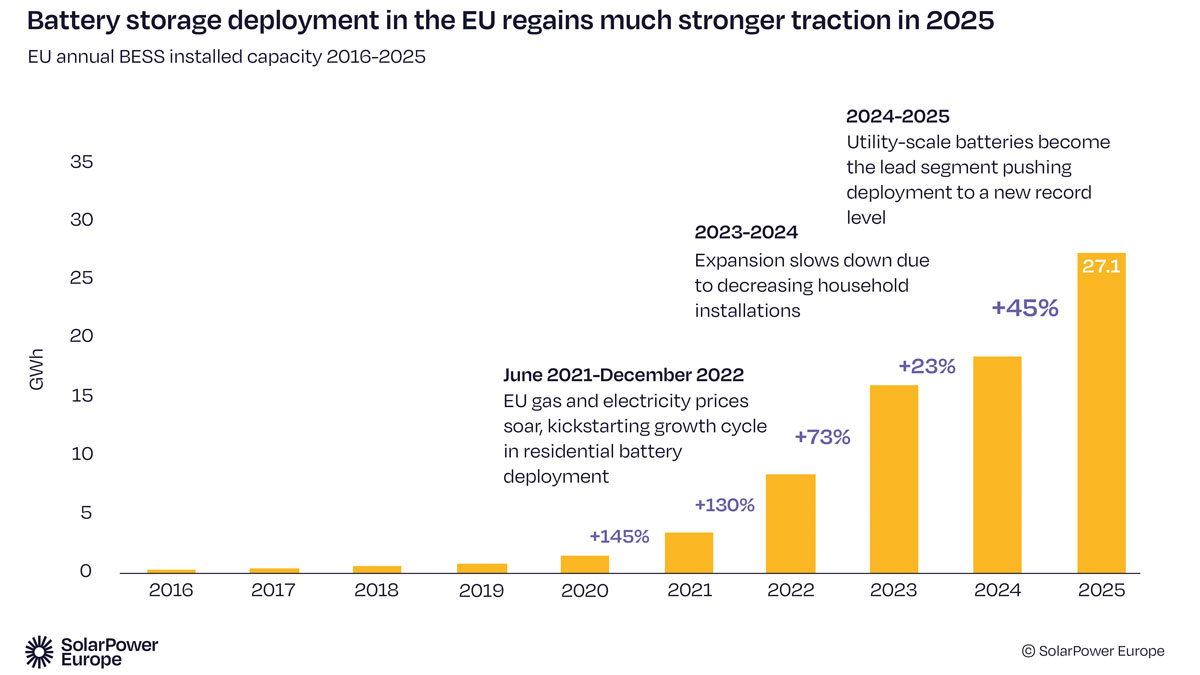

Record Growth in Battery Energy Storage Capacity: The deployment of Battery Energy Storage Systems (BESS) is seeing record growth in 2026. The power demand from AI data centers is emerging as a new driver for battery storage, with cell shipments surging as well.

-

Chinese EVs Gain Global Share Amid Oil Crisis — Import Security Dilemma: Chinese EV exports are accelerating during the oil shock. While demand for EVs in European and Asian markets is surging—increasing the market share for Chinese manufacturers—governments are considering stricter regulations citing cybersecurity vulnerabilities.

Automotive, Shipbuilding, and Steel

-

Thailand-Cambodia Joint Energy Development Agreement Terminated: Reuters reported on May 5 that Thailand has terminated a 25-year-old joint energy exploration agreement with Cambodia. The possibility of regional energy supply chain reorganization is drawing attention.

-

Explosion at Kazakhstan’s Largest Zinc Smelter — Production Disruption Fears: An explosion at Kazakhstan’s largest zinc smelter killed two people. The impact on global zinc supply is currently being assessed, and disruptions in raw material procurement for the steel and galvanizing industries are expected.

4. Corporate Moves

-

Fox Business / U.S. Energy Companies: As energy prices soar due to the Iran conflict, U.S. refineries are responding to the surge in demand for the summer driving season. The national average gasoline price has hit a record $4.45 per gallon, up $1.28 from the same period last year, increasing the burden on households.

-

World Bank: In its latest commodity market outlook, the World Bank warned that energy prices could jump 24% this year due to the Middle East war, reaching levels not seen since Russia’s invasion of Ukraine in 2022.

-

Atlantic Council (Think Tank): In an analysis report published on May 5, the council noted that while global exports of Chinese EVs are expanding rapidly amid the oil crisis, the cybersecurity vulnerabilities created by vehicle connectivity pose a new security dilemma for importing governments.

-

Government Pension Fund Global (Norway): Reuters reported on May 5 on an exclusive report from an environmental NGO, which points out that Norway’s sovereign wealth fund is falling short of its climate goals.

5. Daily Insight

As the blockade of the Hormuz Strait exceeds two months, the vulnerabilities of the global raw material supply chain are being laid bare. With over 8.2 billion barrels of oil inventory already depleted, U.S. gasoline prices have hit a record $4.45, and the explosion at the Kazakhstan zinc smelter has added further strain to industrial metal supply chains. The World Bank projects that energy prices will rise by 24% this year—the largest increase since 2022—making rising production costs for energy-intensive sectors like batteries and semiconductors inevitable.

Paradoxically, this energy crisis is driving explosive demand in the EV and battery industries. While the global expansion of Chinese EVs accelerates, semiconductor sales have jumped 25% from the previous quarter due to AI demand. Yet, supply chain bottlenecks remain unresolved due to simultaneous physical and geopolitical constraints. We are seeing a chain reaction: energy crisis → rising raw material costs → pressure on manufacturing costs → supply chain reorganization. In particular, the cybersecurity issues surrounding Chinese EVs deserve attention as they may evolve from simple technical concerns into broader trade and diplomatic frictions.

6. What to Watch Next

-

Hormuz Strait Ceasefire Negotiations: The outlook for oil prices and energy supply chains could change rapidly depending on the progress of negotiations between the U.S. and Iran regarding control of the strait and Middle East ceasefire discussions. If the current stalemate persists, a European energy crisis may become reality.

-

Assessments of Kazakhstan Zinc Smelter Damage: Announcements regarding the scale of production disruptions and recovery schedules for the damaged zinc smelter are expected. Industry players should monitor this as it may affect global zinc supply and the procurement of steel and automotive parts.

-

OPEC+ Meetings and Trump Administration Energy Export Policies: As surging U.S. energy exports push domestic fuel prices to record highs, calls for policy reviews are mounting. OPEC+ trends and discussions on U.S. government energy export regulations are key variables for the oil and LNG supply chain outlook.

7. Reader Action Items

-

Procurement Managers for Energy-Intensive Materials: Given that oil prices have hit a 4-year high and U.S. gasoline prices have reached a record $4.45, please immediately upwardly adjust fuel and logistics cost projections and review long-term energy hedging strategies. Further supply shocks from Europe are expected if the Hormuz blockade continues.

-

Semiconductor & Electronic Parts Purchasing Managers: Despite a 25% surge in semiconductor sales, supply bottlenecks remain. As priority allocation to AI data centers intensifies, availability for industrial and automotive chips may become even tighter. Consider scouting alternative suppliers and expanding inventory buffers.

-

EV & Battery Industry Stakeholders and Investors: Monitor the risks of both surging Chinese EV exports and the strengthening of cybersecurity regulations in various countries. Depending on the direction of import regulations, pressure for supply chain rerouting or localization may increase; follow the Chinese EV policy trends in the EU, U.S., and Southeast Asia closely.

Source Principle: All figures, company names, and contract details in this briefing are cited exclusively from the original text provided above. No information not found in the original research is included.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by