Commodity Watch — 2026-06-02

Energy markets face upward pressure amid Middle East tensions, with Brent crude expected to hold around $106/barrel through June as global inventories tighten. Natural gas remains well-supplied heading into summer, while precious metals and agricultural commodities show mixed movement as geopolitical uncertainty sustains safe-haven demand.

Commodity Watch — 2026-06-02

Today's Price Snapshot

| Commodity | Price | Change | Trend |

|---|---|---|---|

| WTI Crude Oil | ~$106/bbl | Stable | Flat |

| Brent Crude | $106/bbl | Stable | Flat |

| Natural Gas | $3.00+ MMBtu | Modest growth | Up |

| Gold | ₹155,919 | -0.64% | Down |

| Silver | ₹266,686 | -1.06% | Down |

| Crude Oil (INR) | ₹8,356 | -2.12% | Down |

Top Stories

Energy Prices Projected to Surge 24% Amid Middle East War Shock

Energy prices are expected to surge by 24% in 2026, reaching their highest level since Russia's 2022 invasion of Ukraine, driven by the ongoing Middle East conflict. The World Bank's latest commodity outlook warns that the war has sent a severe shock through global markets, affecting oil supply chains and pricing across all energy commodities. This marks a critical inflection point for energy-dependent economies worldwide.

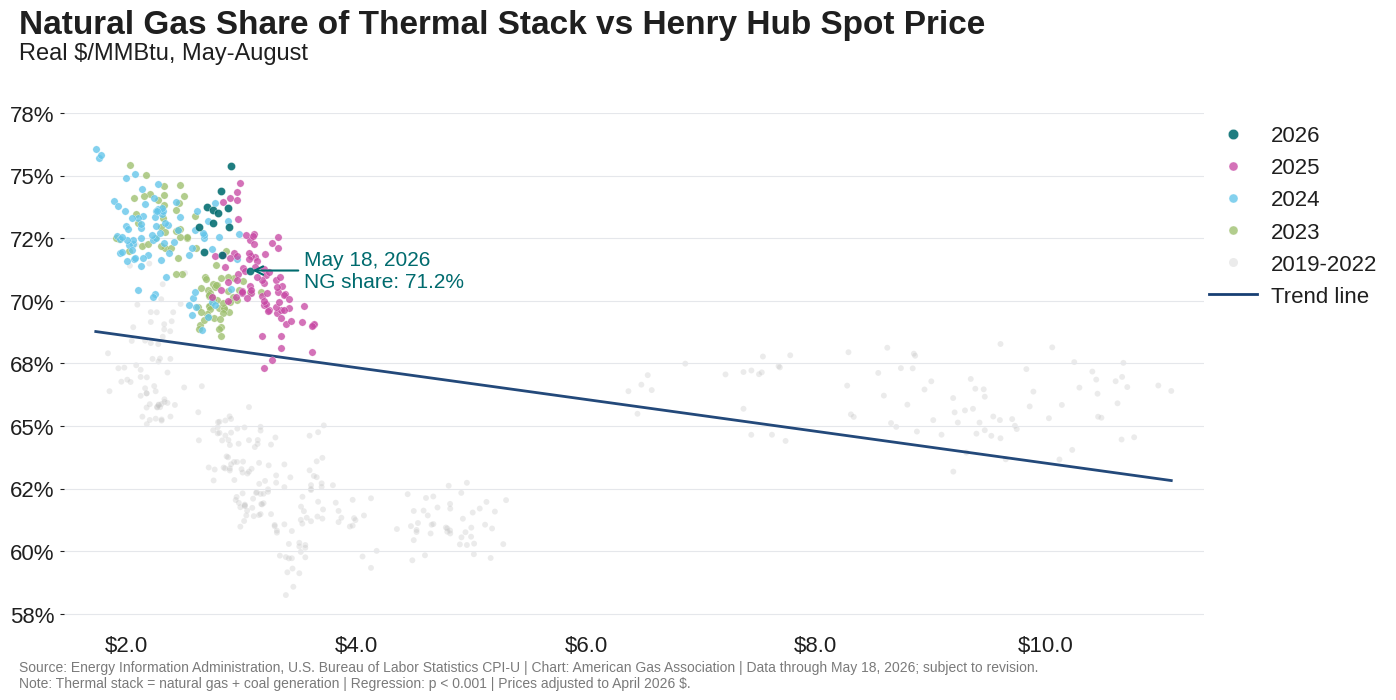

U.S. Natural Gas Market Remains Well-Supplied Despite Rising Summer Demand

The U.S. natural gas market shows signs of strengthening demand ahead of summer, yet remains well-supplied with modest price growth expected. The June Henry Hub contract expired slightly above the $3 per MMBtu mark on May 27, after several weeks trading below that threshold. Adequate storage levels and cooling demand should keep prices in check through the season, according to the American Gas Association.

Strait Uncertainty Creates Oil Supply Risk for Q2-Q3 2026

Commodity analysts note that uncertainty regarding the Strait of Hormuz remains elevated, with current expectations that the waterway will reopen from June onward. However, if the strait remains effectively closed, the risk of serious shortages grows substantially. This geopolitical variable will remain a key price driver through mid-year as markets assess the likelihood of supply disruptions.

Energy Markets

The U.S. Energy Information Administration's latest Short-Term Energy Outlook (STEO) projects that global oil inventories will fall by an average of 8.5 million barrels per day in Q2 2026, supporting Brent prices around $106/barrel in May and June. As oil production gradually increases in the Middle East, crude prices are expected to decline to an average of $89/barrel in Q4 2026 and further to $79/barrel by year-end, reflecting normalization as conflict-related supply shocks ease. The energy market remains vulnerable to additional geopolitical developments, particularly any escalation affecting Middle Eastern production.

Natural gas demand is rising seasonally ahead of summer cooling season, with spot prices strengthening from several weeks below $3.00 MMBtu. Despite tightening storage conditions, the market remains adequately supplied to prevent runaway price spikes. Expect continued modest upward pressure on natural gas through June as air-conditioning demand builds and some industrial demand persists.

Precious Metals & Industrial

Precious metals traded lower on June 2, with gold declining 0.64% to ₹155,919 and silver falling 1.06% to ₹266,686 in late-session trading. The weakness reflects a pullback from safe-haven premium pricing, though geopolitical tension remains supportive of longer-term gold demand. Central bank activity and dollar strength will continue to anchor precious metals prices; any escalation in Middle East tensions could reignite safe-haven flows into gold and silver.

Copper, while not reflecting today's intraday moves in available data, remains pressured by concerns over industrial demand amid broader economic uncertainty tied to the Middle East conflict and its supply chain implications.

What to Watch

- OPEC+ Production Data (June 2026): Any announced increases in production will be critical for validating the EIA's forecast decline in oil prices by Q4.

- U.S. Energy Storage Reports: Weekly crude and natural gas inventory data could signal tightening conditions that support prices.

- Middle East Supply Developments: Further geopolitical events, particularly involving the Strait of Hormuz, remain a tail-risk driver for oil markets.

- Fed Interest Rate Expectations: Higher-for-longer rates could weaken industrial demand for copper and other metals; watch for June FOMC communications.

- Summer Weather Forecasts: Heat waves could accelerate natural gas demand and air-conditioning load, supporting price strength through July-August.

Note: Market data reflects prices and trends from June 2, 2026. Real-time pricing and additional commodity details are available on trading platforms referenced in this report.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by