Emerging Markets Pulse — July 4, 2026

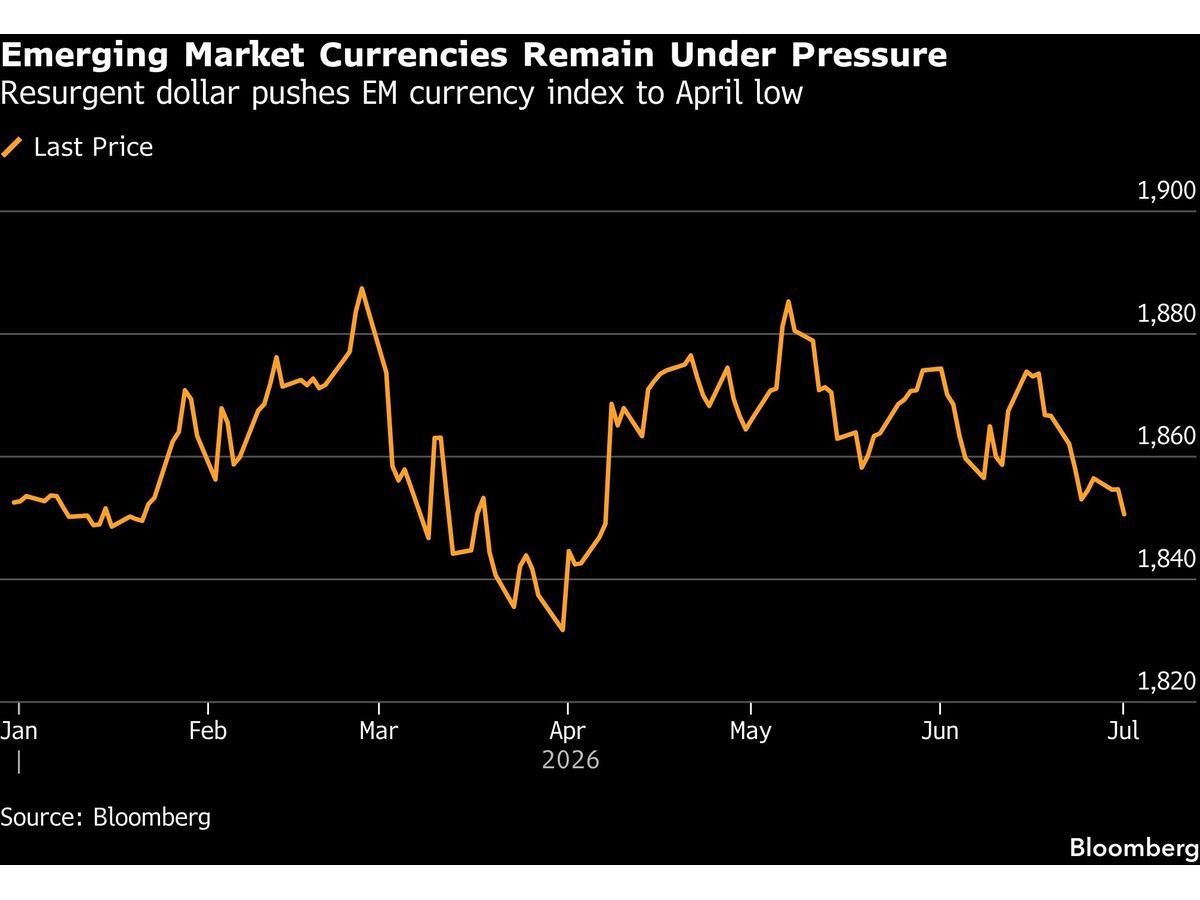

Emerging-market currencies have erased their 2026 gains as the US dollar surges on renewed rate-hike speculation, while softer US jobs data (57,000 June positions vs. 180,000+ expected) triggered a brief rally in EM equities and Indian bonds. Global stocks climbed Friday as Fed tightening fears receded, but EM FX weakness persists amid capital flow headwinds and dollar strength.

Emerging Markets Pulse — July 4, 2026

Market Snapshot

| Benchmark | Level | Weekly Change | Driver |

|---|---|---|---|

| MSCI EM Index | — | Mixed, rotation out of tech | US jobs disappointment eases Fed hike bets; risk-on flows into non-tech EM |

| EMBI Global Spread | — | Tightening | Lower oil prices, foreign inflows to Indian govt bonds supporting EM credit |

| Emerging Market Currency Basket | Down ~2.5% YTD | Erased 2026 gains | Dollar strength on higher US rate expectations; speculative outflows |

| EM Local Currency Bond Index | Steady | Modest support | Falling oil, Bloomberg index inclusion hopes lift Indian bonds |

| Nifty 50 (India) | — | Up week-to-date | Foreign investor flows, lower commodity costs boost sentiment |

This Week's Big Story

EM Currencies in Freefall; Dollar Resurgence Wipes Out YTD Gains

Emerging-market currencies have collapsed to erase all gains accumulated since the start of 2026, driven by renewed speculation over higher US interest rates and a resurgent US dollar. The DXY (US Dollar Index) has surged as markets price in the possibility of Fed tightening, reversing months of relative EM currency strength. From Mexico's peso to Brazil's real to India's rupee, nearly every major EM currency has lost ground. The selloff reflects a classic "risk-off" dynamic: as US rates rise in expectation, US-based investors repatriate capital and reduce emerging-market allocations. However, on Friday (July 3), a softer-than-expected US jobs report—just 57,000 positions created in June versus consensus expectations of 180,000+—jolted markets in the opposite direction. The unemployment rate held steady at 4.2%, signaling labor-market cooling. This data prompted a swift repricing: investors scaled back bets on near-term Fed rate hikes, triggering a short-lived EM equity bounce and renewed interest in Indian government bonds. Equity markets globally rose Friday, with Europe's Stoxx 600 hitting a 52-week high as rotation from technology stocks into broader value and EM-sensitive sectors gained traction.

Central Bank Watch

-

Reserve Bank of India (RBI): Foreign inflows and lower oil prices are supporting Indian government bonds; no rate decision this week, but market focus remains on Bloomberg bond index inclusion expectations and the RBI's tightening cycle trajectory.

-

Federal Reserve (US): Held rates steady at its June meeting but signaled willingness to hike later in 2026; softer July jobs data has dialed back immediate rate-hike odds. The market repricing on Friday reflects expectations for a later tightening cycle than previously priced.

Country Spotlights

India — Bonds Strengthen on Foreign Flows and Oil Relief

- What happened: Indian government bonds rallied Thursday despite a rise in US Treasury yields, bucking the broader correlation between EM and US debt. Foreign investors increased positions ahead of potential Bloomberg bond index inclusion, while global oil prices declined materially, reducing headline inflation pressure.

- Market impact: Rupee weakness persisted (down ~1.5% YTD), but local-currency bond yields fell 10–15 bps as foreign buying accelerated. The bond market outperformance reflects differentiated capital flows based on index inclusion mechanics.

- What's next: Watch for any RBI policy signals on inclusion timing and the next inflation print (early August) to gauge whether disinflation momentum sustains. Further oil declines would support EM debt broadly.

United States (Fed Policy Spillovers) — Jobs Miss Triggers EM Relief Rally

- What happened: The June US nonfarm payrolls report released Friday showed only 57,000 new jobs, sharply below the 180,000+ consensus, while the jobless rate steadied at 4.2%. This was the weakest monthly print since mid-2024 and signaled cooling labor demand.

- Market impact: Equity markets rallied: the Dow jumped over 600 points to a record, and the S&P 500 posted gains for the week despite the tech selloff. Nasdaq fell as mega-cap tech retreated, but broad rotation into value and international (EM-exposed) sectors supported risk sentiment. The repricing lowered near-term Fed hike probability.

- What's next: July's jobs data (due early August) and the Fed's next rate decision (late July) are critical; if the softness persists, the Fed's hiking timeline could extend into late 2026, potentially reducing upside pressure on EM currencies.

Capital Flows & Positioning

No recent high-frequency ETF flow data (EEM, VWO, EMB) was disclosed in fresh reports; however, reports from July 1–3 note that rotation away from technology into broader equity and fixed-income markets has supported EM asset classes on a relative basis. Foreign inflows into Indian government bonds accelerated ahead of potential index inclusion, offsetting currency weakness. Softer US jobs data has likely reduced dedicated EM outflows that had dominated late June.

Institutional View

The World Bank projects global growth to ease to 2.6% in 2026 as demand-supportive factors wane, with emerging-market and developing economies particularly vulnerable to Middle East tensions and dollar strength. The IMF's January 2026 update forecast 3.3% global growth for 2026, with EMDE growth just above 4%. However, the deteriorating labor market in the US (as evidenced by Friday's jobs miss) may temporarily ease the Fed's tightening bias, potentially relieving near-term pressure on EM currencies and reducing refinancing risks for dollar-denominated EM debt. Analysts warn that if the US slowdown deepens, commodity demand could weaken further, pressuring commodity-exporting EMs (Brazil, Colombia, South Africa).

What to Watch Next

- Fed Interest Rate Decision (July 30): The July FOMC meeting will be critical; should the Fed signal a pause or dovish pivot, EM currencies (especially high-beta pairs like BRL, MXN) could stage a relief rally.

- China Services PMI (July 3–4): Already released Friday showing a slowdown in services growth; weakness could weigh on Asian EM demand and commodity prices.

- India Inflation Print (Early August): CPI data will confirm whether lower oil prices are translating to headline disinflation, supporting the RBI's narrative on future rate cuts.

- Brazil's Central Bank Decision (Early August): BCB guidance on Selic trajectory will determine if fiscal-inflation pressures are being contained; a hold or pivot toward cuts would support BRL.

Reader Action Items

- Rebalance EM Currency Exposure: The 2.5% YTD decline in the EM FX basket has created valuation dislocations; consider selectively adding to high-conviction EM currencies (e.g., Indian rupee, Mexican peso) on any Fed-dovish signals, as positioning has become crowded in USD longs.

- Monitor India's Bond Inclusion: Track any Bloomberg announcement on formal inclusion of Indian sovereign bonds; if confirmed, foreign inflows could accelerate 20–30% above current levels, supporting both the rupee and local-currency bond markets into Q4 2026.

- Watch Brazil's Fiscal Path: Keep tabs on Brazilian fiscal policy developments (diesel subsidy phase-out, Pix regulation) ahead of the October 2026 presidential election; political risks remain elevated and could trigger BRL volatility.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by