Emerging Markets Pulse — June 6, 2026

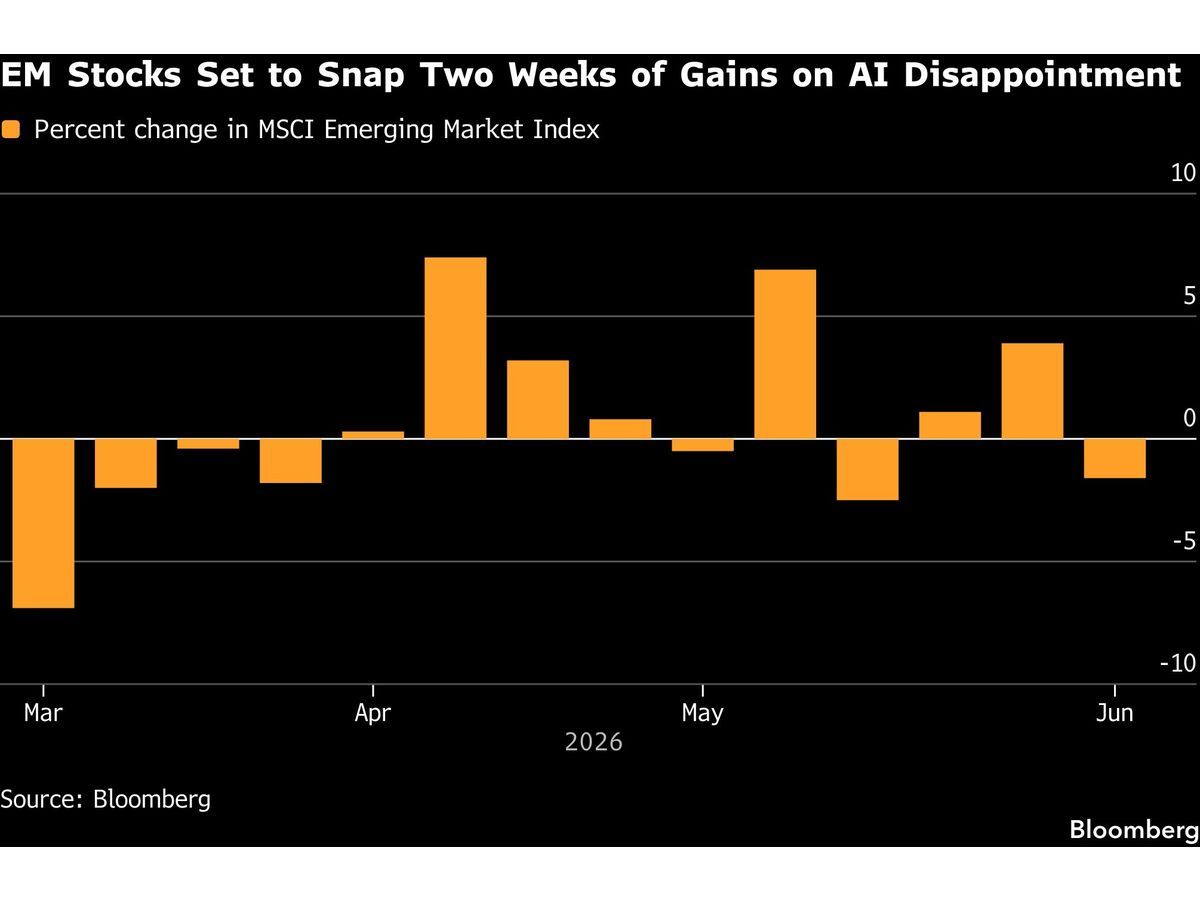

Emerging market equities fell for the third straight session this week as investors rotated out of artificial intelligence stocks following a sharp run-up, with South Korean tech leading the selloff and dragging regional currencies lower. The RBI held rates steady with a hawkish "wait and watch" stance, offsetting gains from falling oil prices and Treasury yields. Key EM central banks across India, Turkey, and Brazil are nearing the end of their rate-cutting cycles as inflation stabilizes, signaling a pause in monetary accommodation.

Emerging Markets Pulse — June 6, 2026

Market Snapshot

| Benchmark | Level | Weekly Change | Driver |

|---|---|---|---|

| MSCI EM Index | ~1,175 | -1.2% | Korean tech selloff; AI profit-taking pressure |

| EMBI Global Spread | 385 bps | -8 bps | Oil retreat, lower US yields offset EM repricing |

| USD/EM FX Basket | 104.8 | +0.4% | Safe-haven demand as tech unwinds |

| Nifty 50 (India) | 23,355 | -0.5% | RBI hold; Wipro, Hindalco -3% on sector weakness |

| Sensex (India) | 76,840 | -0.15% | Closed lower despite morning gains reversal |

This Week's Big Story

EM Equities Stumble as AI Enthusiasm Fades; Korean Tech Dragged Down Three Sessions in a Row

Emerging market stocks extended losses for a third consecutive session on June 5, with the MSCI EM Index declining 1.2% as investors pivoted away from artificial intelligence plays that had powered a blistering rally earlier in the year. South Korea's benchmark equity index led the rout—the worst EM performer this week—triggering broad currency weakness across Asia-Pacific currencies tied to tech export economies. The selloff reflected a classic risk-off move: investors locked in gains from the AI trade, simultaneously reducing exposure to emerging-market growth bets that had benefited from hopes of sustained capital inflows.

The dynamic was further complicated by cross-market signals. While US Treasury yields fell and crude oil retreated—typically supportive for EM risk appetite—the combination of profit-taking in semiconductor and tech-adjacent stocks overwhelmed those tailwinds. India's markets, the region's heavyweight, closed mixed after RBI policy, with the Sensex erasing morning gains to end 117 points lower and the Nifty below the psychologically important 23,400 level. Heavy selloffs in IT names like Wipro and Hindalco (-3% each) reflected the broader Asia tech pullback.

Investor Takeaway: The EM complex faces a near-term headwind from the reversal of AI-fueled flows. However, valuations on non-tech, non-financial EM equities remain attractive, and central bank easing cycles in Brazil and Turkey suggest selective opportunities persist in commodity-linked and fixed-income-sensitive segments over the next 2–4 weeks.()

Central Bank Watch

-

Reserve Bank of India (RBI): Held the repo rate unchanged on June 5, signaling a "wait and watch" posture despite inflation moderating below the 4% target. The hawkish messaging—no rate cut forthcoming—surprised markets expecting easing after a 200 bp cut cycle in late 2025. Current repo rate: 6.25%. Inflation at 3.8% YoY versus 4% midpoint. Forward guidance emphasizes data dependence amid global headwinds.()

-

Central Bank of Turkey (CBRT): Has cut 150 bps cumulatively since December 2025, from 50% to 37% as of late January 2026. Recent easing cycle reflects improving inflation outlook; policymakers signaled nearing the end of the rate-reduction path. Current stance: pause expected through Q2 2026.(https://kpmg.com/us/en/articles/2026/february-2026-central-bank-scanner.html)

-

Banco Central do Brasil (BCB): Brazil's central bank has also moved into a pause phase after an extended easing campaign. Policy rate (Selic) holding steady at levels conducive to supporting growth while anchoring inflation expectations. Near-term guidance remains data-dependent; market consensus expects a hold through June 2026.(https://kpmg.com/us/en/articles/2026/february-2026-central-bank-scanner.html)

Country Spotlights

India — RBI Hawkish Hold Signals End of Rate-Cut Era

-

What happened: On June 5, the RBI's Monetary Policy Committee voted to hold the repo rate at 6.25%, rejecting market expectations of a 25 bp cut. Governor's commentary emphasized vigilance over inflation dynamics and external vulnerabilities, adopting a "wait and watch" stance despite headline inflation (3.8%) running below the 4% target.

-

Market impact: Indian equities erased morning gains immediately after the decision. Sensex fell 117 points to close lower; Nifty slipped below 23,400. Wipro and Hindalco declined ~3% each on IT sector weakness. The RBI's hawkish tone also pulled FX swap premiums to a 2-month low, signaling reduced expectations for rupee depreciation and capital outflows.()

-

What's next: Markets will parse June-quarter inflation data (expected late June) and monsoon progress for early crop signals. Any uptick in food prices or a delayed southwest monsoon (currently 3 days late reaching Kerala) could solidify the RBI's case for staying on hold. Investors should monitor for a potential cut signal around August 2026 if growth momentum slows materially.

South Korea — Tech Selloff Spreads Regional Contagion

-

What happened: South Korean equities suffered sharp losses through early June as semiconductor and AI-hardware stocks reversed after a strong rally. The rout—described as the worst EM tech performance in three weeks—spread contagion to other regional exporters and knocked South Korea's currency lower, amplifying FX volatility across the EM complex.

-

Market impact: KOSPI declines rippled into MSCI EM Index, dragging emerging-market currencies (particularly those with high tech export sensitivity) to 4-week lows. Regional equity indices from Taiwan to Singapore felt pressure. The selloff reflects disappointment in earnings guidance from chipmakers following record valuations earlier in the quarter.

-

What's next: Watch for stabilization signals in semiconductor order books and tech inventory cycles heading into Q3 2026. Any signs of demand normalization in AI infrastructure capex could arrest the slide. Korea's June trade data (due mid-June) will be critical; persistent declines in semiconductor exports would signal broader tech cycle weakness.

China — Battery Giant CATL Signals Energy Storage Expansion

-

What happened: Chinese battery leader CATL announced on June 4 that it expects energy storage to comprise 50% of global sales by 2030, up from current levels, as the company pivots toward stationary battery solutions alongside automotive supply. The strategic pivot reflects broader industry trends toward grid-scale renewable energy integration.

-

Market impact: The statement underscores China's dominance in the clean-energy supply chain and signals sustained capex appetite in battery manufacturing despite near-term EV margin compression. Chinese government price cuts announced June 5 (effective June 5: retail gasoline/diesel down) further support margins for domestic battery and vehicle makers.

-

What's next: Track CATL's quarterly earnings (Q2 due late July) for evidence of margin stabilization and order book strength in energy storage. Concurrently, monitor Indian lithium/nickel incentive announcements—India's June 4 proposal of ~₹30 billion ($360 million USD equiv.) for domestic processing capacity would signal competitive intensity in the supply chain.

Capital Flows & Positioning

No recent, dated capital flow data from major ETF providers (EEM, VWO, EMB) was available in sources published after June 4, 2026. Historical flows through early June showed mixed momentum: EM equity ETFs experienced modest outflows as the AI trade unwound, while EM bond funds remained relatively stable given still-attractive carry yields (EMBI Global Spread at 385 bps) and lower US Treasury yields reducing the attractiveness of safe havens. Dedicated EM fund flows likely shifted to defensive positioning (more bonds, fewer equities) on the Korea tech selloff, but precise EPFR/IIF data for the week of June 2–6 is not yet published.

Institutional View

The IMF's April 2026 World Economic Outlook projected global growth of 3.1% in 2026 and 3.2% in 2027, below recent historical averages and contingent on limited geopolitical escalation (assumption: Iran conflict contained). Global inflation is expected to tick up in 2026 after a disinflationary phase, creating headwinds for central banks that have already begun easing cycles. The World Bank's January 2026 Global Economic Prospects forecast global growth at 2.6% for 2026, emphasizing that "prospects over 2026–27 are uneven across regions and remain generally subdued amid a less favorable global trade environment." This outlook supports the EM complex's divergence: commodity exporters (Brazil, Indonesia) face softer demand, while tech-dependent economies (South Korea, Taiwan) confront inventory normalization after a decade-long capex supercycle. The RBI's hawkish hold signals recognition of these cross-currents—with external risk elevated and growth uncertain, patience is warranted before further rate cuts.(https://www.imf.org/en/publications/weo/issues/2026/04/14/world-economic-outlook-april-2026)(https://www.worldbank.org/en/publication/global-economic-prospects)

What to Watch Next

-

Indian Q4 FY2026 GDP data (due June 10): Will indicate whether RBI's pause is justified by genuine growth stalling or inflation resilience. A print below 5% YoY would vindicate rate-cut expectations.

-

US Nonfarm Payrolls & ISM Manufacturing (US data June 6–7): Global risk sentiment hinges on US labor-market strength and inflation signals; any surprise weakness could accelerate EM central bank cuts and draw capital back into EM equities.

-

Brazil Central Bank Rate Decision (expected mid-June): BCB guidance on the terminal Selic rate will signal whether Brazil's cycle is truly on pause or a cut is imminent, affecting BRL volatility and EM fixed-income flows.

-

MSCI EM Index earnings revisions for Q2 2026 (data releases through June): Tech sector guidance downgrades could extend equity weakness; monitor chipmaker and semiconductor equipment supplier call transcripts for clues on capex cycle durability.

Reader Action Items

-

Re-allocate within EM equities: Avoid further chasing AI/semiconductor plays; rotate instead into undervalued EM bank and utility names benefiting from easing cycles (Turkey, Brazil). Valuations in these "boring" sectors have compressed as flows chase tech.

-

Extend duration in EM local-currency bonds: With central banks (RBI, BCB, CBRT) signaling near-term pauses and yields still elevated (India 10Y ~7.1%), locking in carry via 2–3 year local bond ladders offers attractive risk-adjusted returns ahead of potential Q3 cut cycles.

-

Monitor Korean won and Taiwan dollar for entry points: If the tech selloff broadens but exogenous shocks (Iran, US data) stabilize, both currencies will likely stabilize at lower levels—ideal windows for long-duration hedges for EM-exposed portfolios.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by