Europe Markets Weekly — 2026-05-20

European equities faced renewed pressure this week as persistent inflation fears tied to the ongoing U.S.-Iran war weighed on sentiment, with major indices recording losses across the board. The euro continued to slide toward six-week lows against the dollar as risk aversion mounted, while G7 finance ministers convened in Paris to address the escalating energy shock. Investors now look ahead to potential ceasefire developments and upcoming central bank signals for direction.

Europe Markets Weekly — 2026-05-20

Market Snapshot

- STOXX 600: Down on the week — logged weekly losses driven by Iran war-linked inflation concerns

- DAX: Fell 1.15% to approximately €23,670 on Monday open as sentiment deteriorated

- FTSE 100: Slipped 0.37% for the week

- CAC 40: Declined 1.97% for the week; futures fell 1.17% to €7,860 at Monday's open

Key Drivers

-

Iran war inflation overhang: European shares fell on Monday as markets found no sign of a deal to end the three-month-old U.S.-Iran conflict, with lingering inflation fears keeping investors defensive. The STOXX 600 recorded its second consecutive week of losses.

-

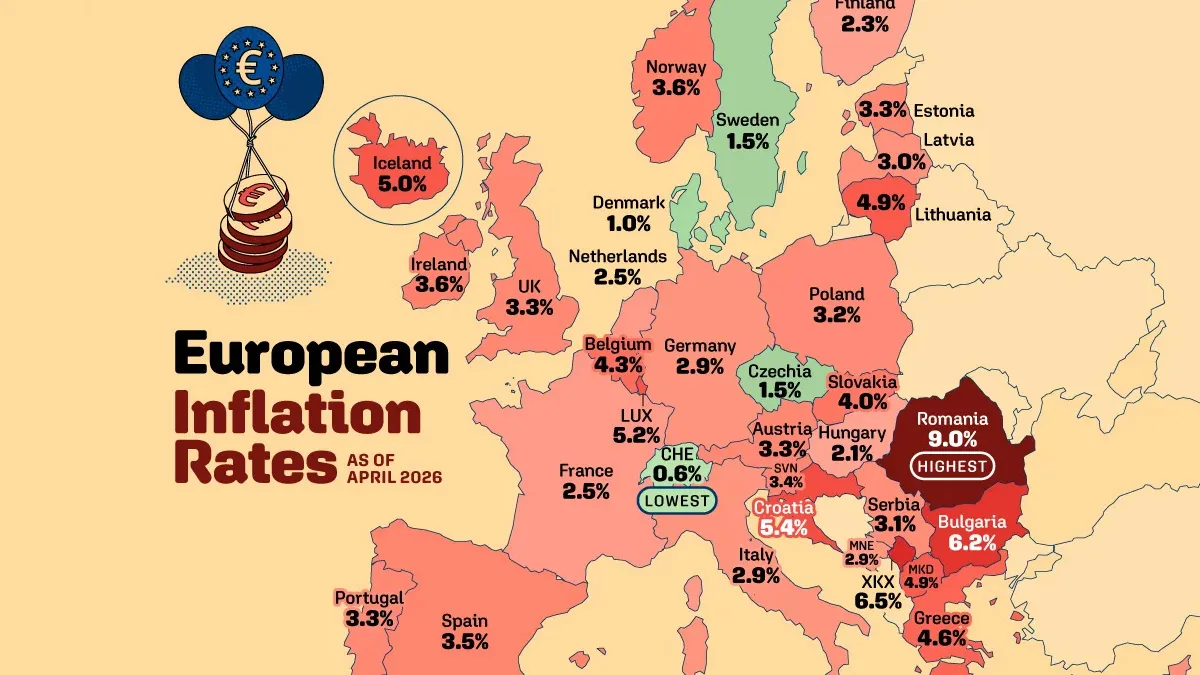

Broad-based European inflation above target: A newly published map from Visual Capitalist (published May 20) confirms that virtually no eurozone economy is within the ECB's 2% inflation target, with energy-driven price pressures evident across the continent, deepening the central bank's policy dilemma.

-

Hawkish ECB tone, euro under pressure: EUR/USD remained subdued, trading around 1.1620 during early week as the US Dollar gained on growing Federal Reserve rate hike expectations. The euro had earlier hit fresh six-week lows just above 1.1600, despite a hawkish ECB tone. Rising oil prices and Middle East uncertainty continued to weigh on the single currency.

-

Mixed sector performance: Financial services firms provided some support — Allianz, Nordea, AXA, and Munich Re each gained over 1%, and Deutsche Boerse surged 5% on reports that activist fund TCI increased its position in the exchange operator. On the other hand, ASML fell 3.2% in line with a broader plunge in AI infrastructure stocks globally.

-

Eurozone industrial production: Eurozone industrial production grew by just 0.2% month-over-month in March 2026, falling slightly short of the 0.3% consensus estimate, adding to concerns about the region's economic momentum.

Earnings & Corporate

- European blue-chips on track for strongest earnings growth since late 2022: According to the latest LSEG I/B/E/S data released May 15, STOXX 600 blue-chip companies are set to deliver the strongest earnings growth since Q4 2022. However, revenue is still expected to fall, underscoring that profit gains are being driven primarily by cost-cutting rather than top-line expansion — a fragile foundation given ongoing macroeconomic uncertainty.

- Deutsche Boerse surges on activist investor move: Shares in Deutsche Boerse jumped 5% after reports emerged that TCI Fund Management increased its stake in the exchange operator, signalling confidence in the group's long-term earnings power despite the turbulent market environment.

Geopolitics & Energy

- G7 finance ministers convene in Paris over energy shock: G7 finance ministers gathered in Paris for a second day of emergency talks on rising energy prices, Strait of Hormuz disruptions, and sanctions policy. Italian Prime Minister Giorgia Meloni publicly urged the EU to treat the energy crisis with the same urgency as defence spending — a sign of deepening political tension within the bloc over crisis response.

- Russia fossil fuel sanctions under review: A report from the Centre for Research on Energy and Clean Air (CREA) published this week found that while existing sanctions have reduced Russia's fossil fuel export revenues and constrained its war financing capacity, analysts argue significantly more should be done to tighten the regime. The findings come as European policymakers debate their next steps at the Paris G7 summit.

What to Watch Next Week

- ECB speakers and rate guidance: With eurozone inflation running above target and growth nearly stalled, any forward guidance from ECB officials will be closely scrutinised for signals on whether the current 2% policy rate hold is sustainable.

- U.S.-Iran war developments: Any movement toward ceasefire negotiations — or escalation — in the Strait of Hormuz remains the single biggest macro risk for European energy prices and market sentiment.

- G7 Paris outcome: The Paris G7 finance ministers' communiqué on energy price coordination and sanctions policy is expected, with markets watching for any concrete measures to ease Europe's energy cost burden.

- Nvidia and US retail earnings spillover: European tech and semiconductor stocks, including ASML, will likely take direction from Nvidia's results, which investors are watching for clues on global AI infrastructure demand.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by