Global Stock Market Trends — 2026-05-03

On Friday, May 1st, U.S. markets saw the S&P 500 and Nasdaq reach all-time highs, marking five consecutive weeks of gains. Strong earnings from tech giants like Apple and falling oil prices fueled the rally, with the S&P 500 recording its best monthly gain since 2020. In South Korea, the KOSPI maintained record levels, pushing the total market capitalization past 6,000 trillion won ($4.1 trillion). This week, key variables include employment data, ongoing earnings reports, and risks from surging oil prices.

Global Stock Market Trends — 2026-05-03

Global Indices at a Glance

| Region | Index | Closing (or Recent) Price | Trend | Change |

|---|---|---|---|---|

| 🇰🇷 South Korea | KOSPI | ~6,740 | ▲ | Record maintained |

| 🇰🇷 South Korea | KOSDAQ | ~1,200 range | ▲ | Continued rise |

| 🇺🇸 USA | S&P 500 | Over 7,200 | ▲ | All-time high |

| 🇺🇸 USA | Nasdaq Composite | 24,663.80 (as of 4/29) | Variable | Near record |

| 🇺🇸 USA | Dow Jones | 49,141.93 (as of 4/29) | ▼25.86pt | -0.05% |

| 🇯🇵 Japan | Nikkei 225 | Recent | — | — |

| 🇭🇰 Hong Kong | Hang Seng | Recent | — | — |

| 🇨🇳 China | Shanghai Comp | Recent | — | — |

| 🇬🇧 UK | FTSE 100 | Recent | — | — |

| 🇩🇪 Germany | DAX | Recent | — | — |

Based on U.S. closing prices on Friday, May 1st, and the most recent Asian prices (April 29–30). Markets in South Korea, Europe, and Asia are closed or inactive as of Sunday, May 3rd.

🇰🇷 South Korean Market

KOSPI / KOSDAQ Overview

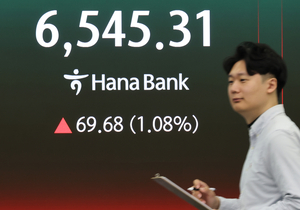

On April 30, the KOSPI surpassed the 6,740 mark during intraday trading, marking its fourth consecutive day of gains and setting a new all-time intraday record. It opened at 6,739.39, up 48.49 points (+0.72%) from the previous close. Driven by a bull market, the total market capitalization of domestic listed companies exceeded 6,000 trillion won (approximately $4.1 trillion) for the first time in history. The KOSDAQ also maintained its upward trend around the 1,200 mark. Strong earnings from U.S. big tech and expanded global investment in AI continue to support the semiconductor and IT sectors.

Trading Trends (as of April 29)

- Foreign investors: Continued net selling

- Institutional investors: Net buying (offsetting foreign sell-off)

- Retail investors: Net buying (confirmed intraday purchases of 268.5 billion won, leading SK Hynix to reclaim 130,000 won)

Key Sectors & Stocks (Recent session)

- Semiconductors (SK Hynix): Strong — SK Hynix reclaimed the 130,000 won per share level, reflecting expectations for AI demand. It is now ranked 17th globally by market cap.

- IT/Tech Sector: Rising — Bolstered by strong global big tech earnings and increased AI investment.

- KOSDAQ Growth Stocks: Continued rise — Retail buying inflows around the 1,200 mark, with some bio and secondary battery stocks showing momentum.

🇺🇸 U.S. Market

Three Major Indices Closing (Friday, May 1st)

On May 1st, the S&P 500 and Nasdaq reached all-time closing highs, finishing their fifth consecutive week of gains. Apple (AAPL) saw a strong rebound, lifting the tech sector, while falling international oil prices improved investor sentiment. The S&P 500 recorded its best monthly gain since November 2020. On April 29, the indices saw a minor correction—S&P 500 at -0.49% (7,138.80) and Nasdaq at -0.9% (24,663.80)—following the Fed's interest rate freeze, but they rebounded starting the next day to hit new record highs on May 1st.

%3Amax_bytes(150000)%3Astrip_icc()%2FGettyImages-2274018123-3550244f15a74fcc893d03217ea1a33a.jpg)

Major Market Moves (May 1st)

- Apple (AAPL): Strong — Surged after its earnings report, lifting the entire market and reigniting the tech rally.

- Nvidia (NVDA): Near all-time high — Continued expectations for accelerated AI infrastructure demand led to further gains after its April 27 record intraday high.

- Oil-related Stocks: Mixed — Energy sector weakened due to a drop in international oil prices (WTI decline). Meanwhile, President Trump's rhetoric regarding Iran has kept geopolitical risks in play.

Sector Trends

The tech and AI sectors led the rally throughout the week. In contrast, the energy sector struggled due to falling oil prices, and defensive stocks remained relatively weak. Immediately following the Fed's rate freeze, rate-sensitive sectors (utilities, REITs) faced short-term pressure, but the overall market remained buoyant thanks to strength in tech and consumer staples.

🌏 Asian & European Markets

Asia (Japan, China, Hong Kong)

As of April 29, Asian markets showed mixed results amid uncertainty regarding the Fed's rate freeze and U.S.-Iran negotiations. While the South Korean KOSPI maintained record strength, the Nikkei 225 and Hang Seng reacted sensitively to geopolitical variables and the Fed's stance. The Shanghai Composite fluctuated between hopes for domestic recovery and external risks. As of May 3, markets in Japan, China, and Hong Kong are closed for the weekend and will resume on Tuesday, May 5.

Europe (UK, Germany, France)

European markets finished last week with gains, tracking the strength of U.S. indices. Both the German DAX and the UK's FTSE 100 maintained a positive trend, supported by improved corporate earnings and stable energy prices. However, risks from surging oil prices and the possibility of a more hawkish Fed have kept investors cautious. When European markets reopen on Monday, May 5, the release of U.S. employment data will be a key factor.

📊 Market Drivers

-

Strong Big Tech Earnings & Accelerated AI Investment: Large-cap tech stocks like Apple and Nvidia exceeded market expectations, driving global markets. Increased investment in AI infrastructure is providing strong momentum for the semiconductor and cloud sectors.

-

Fed Rate Freeze & Hawkish Signals: Following the April 29 rate freeze, Chair Powell expressed caution regarding inflation risks, including rising oil prices. Markets are recalibrating rate-cut expectations, and this week's non-farm payroll data will be a critical trigger for reassessing the Fed's path.

-

Surging Oil Prices & Geopolitical Risk: President Trump's instructions for a long-term blockade of Iran have heightened fears over oil supply. Surging oil prices are now a key market risk, raising concerns about inflation and a potential hawkish pivot by the Fed.

-

South Korea’s Market Cap Hits 6,000 Trillion Won: Driven by the KOSPI's strength, the total market cap of the South Korean stock market crossed the 6,000 trillion won ($4.1 trillion) milestone for the first time. Despite foreign selling, retail and institutional buying have supported the index, maintaining a steady inflow of global funds.

🔭 What to Watch

Key Events This Week

- U.S. Non-Farm Payrolls (NFP): Expected to be released in the first week of May. Will directly impact Fed policy reassessments and market volatility.

- Additional S&P 500 Earnings: First-quarter results from energy, financial, and consumer goods companies to be released.

- International Oil Price Trends: Monitoring potential volatility in WTI/Brent prices linked to the Iran blockade.

- KOSPI 6,800 Breakthrough: Potential for a further rally if foreign investment recovers; otherwise, profit-taking remains a concern.

- Fed Member Statements & Minutes: Potential shifts in hawkish/dovish sentiment affecting dollar and bond markets.

Investor Checklist

- Review portfolios against a scenario of high oil prices → inflation → delayed Fed rate cuts.

- Reassess exposure to AI/semiconductor sectors: Earnings momentum remains, but valuation pressures persist.

- Look for signs of a reversal in foreign investment in the KOSPI; buying from institutions and retail alone has limits for sustaining a rapid climb.

💬 One-Line Insight

While the AI momentum proven by big tech remains strong, rising oil prices and a potential hawkish pivot from the Fed are setting up the next hurdle for this "record rally."

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by