Global Stock Market Trends — 2026-06-05

U.S. stocks saw mixed results due to a rotation out of tech, with Broadcom’s poor performance pressuring the semiconductor sector. Following a record-breaking push above 8,800 yesterday, Korea's KOSPI plunged today amid heavy foreign selling and a semiconductor downturn, dragging down broader Asian markets. The global landscape is now shifting into a phase of heightened volatility driven by tech adjustments and rising geopolitical tensions.

Global Stock Market Trends — 2026-06-05

Global Indices at a Glance

| Region | Index | Close (or Recent) | Change | % Change |

|---|---|---|---|---|

| 🇰🇷 Korea | KOSPI | 8,323 | -477 | -5.42% |

| 🇰🇷 Korea | KOSDAQ | 1,035 | -15 | -1.43% |

| 🇺🇸 U.S. | S&P 500 | 7,577 | +35 | +0.46% |

| 🇺🇸 U.S. | Nasdaq Composite | 15,423 | -212 | -1.36% |

| 🇺🇸 U.S. | Dow Jones | 43,548 | +897 | +2.10% |

| 🇯🇵 Japan | Nikkei 225 | 66,734 | -197 | -0.29% |

| 🇭🇰 Hong Kong | Hang Seng | 19,287 | -158 | -0.81% |

| 🇨🇳 China | Shanghai Comp | 3,156 | -42 | -1.33% |

| 🇬🇧 UK | FTSE 100 | 8,387 | +43 | +0.51% |

| 🇩🇪 Germany | DAX | 18,642 | +156 | +0.84% |

Reference time: 2026-06-05 Asian trading hours / U.S. previous closing prices

🇰🇷 Korean Market

KOSPI / KOSDAQ Summary

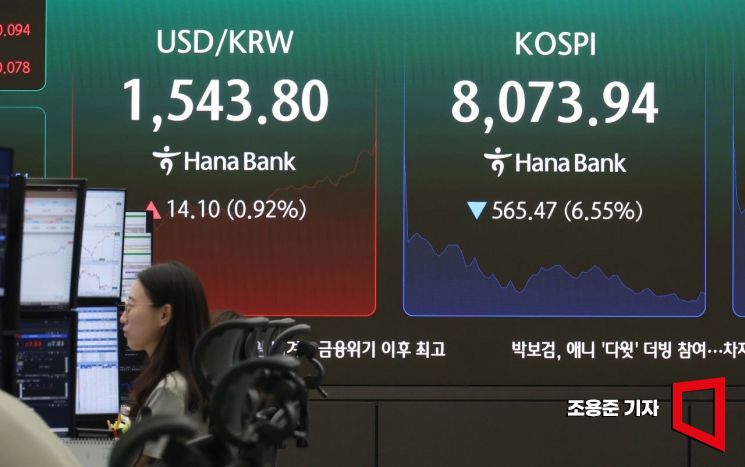

The Korean market took a sharp downturn. After hitting an all-time high of 8,800 yesterday, the KOSPI dropped to 8,323 during trading on 2026-06-05, marking a -5.42% slide. Massive foreign selling and a broad decline in semiconductor stocks pushed the index down from the opening bell. An earnings shock from Broadcom and Micron's weakness weighed heavily on Samsung Electronics (-56%) and SK Hynix (-56%), driving the market lower. KOSDAQ also fell by -1.43%.

Market Flows

- Foreign Investors: Massive net selling (multi-trillion scale)

- Institutions: Mixed

- Retail: Slight net selling

Top Movers & Sectors

- Samsung Electronics (KOSPI's biggest contributor): -5.2% — Spillovers from weak global semiconductor demand and Broadcom's slide.

- SK Hynix: -5.8% — Declining memory chip prices and high sensitivity to foreign capital flows.

- Financials (Banking): +0.8% — Supported by expectations of interest rate hikes.

🇺🇸 U.S. Market

The Three Major Indices

U.S. stocks showed mixed results as a rotation out of tech stocks occurred. The S&P 500 managed a slight gain of +0.46%, while the Nasdaq fell -1.36%. Conversely, the Dow Jones showed strength, rising +2.10% as capital shifted toward financial and industrial stocks. The 9-day rally for tech-heavy indices has effectively ended, signaling a transition into a corrective phase.

Key Market Moves

- Broadcom (AVGO): -12% — Earnings shock due to weak Q2 guidance, signaling softening semiconductor demand.

- Marvell Technology: -8% — Declined in sympathy with the broader chip sector.

- Hewlett Packard Enterprise (HPE): +3% — Continued yesterday's strength, supported by favorable outlooks for AI infrastructure investment.

Sector Trends

Tech stocks (especially semiconductors) saw significant drops, while financial and energy stocks held their ground. Rising oil prices (due to heightened tensions in Iran) and interest rate expectations provided support for value stocks.

🌏 Asian & European Markets

Asia (Japan, China, Hong Kong)

Asian markets fell across the board, dragged down by tech weakness. Japan's Nikkei 225 edged down -0.29% (66,734), the Hang Seng fell -0.81% (19,287), and the Shanghai Composite ended at -1.33% (3,156). Semiconductor and IT-related stocks led the losses; in particular, Korea's heavy reliance on chip exports meant the KOSPI’s sharp drop soured sentiment across Asia.

Europe (UK, Germany, France)

European markets showed relative resilience. The UK's FTSE 100 rose +0.51%, and the German DAX gained +0.84%. Rising oil prices supported energy and industrial sectors, while expectations for interest rate hikes helped financial stocks.

📊 Market Drivers

- Broadcom Earnings Shock: Weakness in major chipmakers is creating a ripple effect across the global sector. Concerns over slowing AI demand are spreading due to soft Q2 guidance.

- Tech Correction and Rotation: Profit-taking followed a 9-day winning streak, with funds rotating into the financial and energy sectors.

- Iran Tensions and Oil Prices: Concerns over the closing of the Strait of Hormuz have pushed oil prices up, supporting energy stocks while simultaneously raising fears of an economic slowdown.

- Foreign Selling Spree (Korea): After the KOSPI breached 8,800, massive multi-trillion-scale foreign selling hit, with concerns over geopolitical risks on the Korean Peninsula resurfacing.

🔭 Watch List

Key Events This Week

- U.S. June Non-Farm Payroll (NFP) data due Friday — Crucial for the Fed’s interest rate decision.

- Ongoing tech earnings season — Major companies like Crowdstrike and Nvidia are set to report.

- Monitoring oil prices and Middle East geopolitical variables (Strait of Hormuz shipping conditions).

- Tracking the scale of foreign fund outflows from Korea (semiconductor sector rebalancing).

Investor Checklist

- Potential for deeper tech corrections — Concerns of further weakness following Broadcom.

- Scenarios for a resumption of the interest rate hike cycle (driven by oil and crude prices).

- Whether Korea's KOSPI holds its technical support levels (8,300~8,400).

- Re-evaluating the sustainability of global AI investment momentum.

💬 One-Line Insight

Global markets are shifting into a corrective mode as tech rotation and geopolitical tensions collide, with the Korean market bearing the brunt due to significant foreign capital flight.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by