Korean Stock Market Briefing: KOSPI Volatility 07-09

Daily Market Brief: Essential Updates for Local Stocks|13 min read8.9AI quality score — automatically evaluated based on accuracy, depth, and source quality

The KOSPI rebounded on the 9th after a two-day slide, though it remains highly volatile due to concerns over semiconductor "peak" theories and renewed tensions in the Middle East. While U.S. chip stock gains spurred bargain hunting, fears of a global economic slowdown continue to weigh on the market.

Korean Stock Market Briefing — 2026-07-09

Market Snapshot

- KOSPI: 7,290 level (estimated +44 points, +0.6% from previous day) — Surged over 4% intraday on the 9th but gains narrowed due to Middle East conflict fears.

- KOSDAQ: 785 level (partial recovery after a 5% plunge).

- KRW/USD Exchange Rate: 1,506.1 won (slightly stronger than the previous day).

- Market Sentiment: Continued extreme volatility. Rapid fluctuations persist as U.S. chip stock rebounds clash with bargain hunting. Option expiration and Middle East variables are amplifying supply-demand instability.

Top 5 Key News Stories

1. KOSPI opens 3% higher following U.S. chip rebound

- What's happening?: On the 9th, the KOSPI recovered the 7,450 level, jumping over 3% at the open after a two-day slide. The rebound in U.S. semiconductor stocks triggered bargain hunting for domestic names like Samsung Electronics and SK hynix. However, intraday volatility remained extreme due to option expiration and geopolitical fears.

- Market Impact: The semiconductor sector led the gains. While major players like Samsung Electronics and SK hynix drove the index up, supply instability capped the upside.

2. Bank of Korea: "Semiconductor boom to last, downside limited"

- What's happening?: In a report to the National Assembly's Finance and Economy Committee on the 9th, the Bank of Korea stated that "the possibility of a trend reversal toward a downtrend in domestic stock prices is limited." They expect the semiconductor export boom to continue through the second half of the year and anticipate that foreign selling will subside. Governor Shin Hyun-song expressed an optimistic outlook.

- Market Impact: Acting as a floor for the semiconductor sector. Official policy commentary helped calm market nerves.

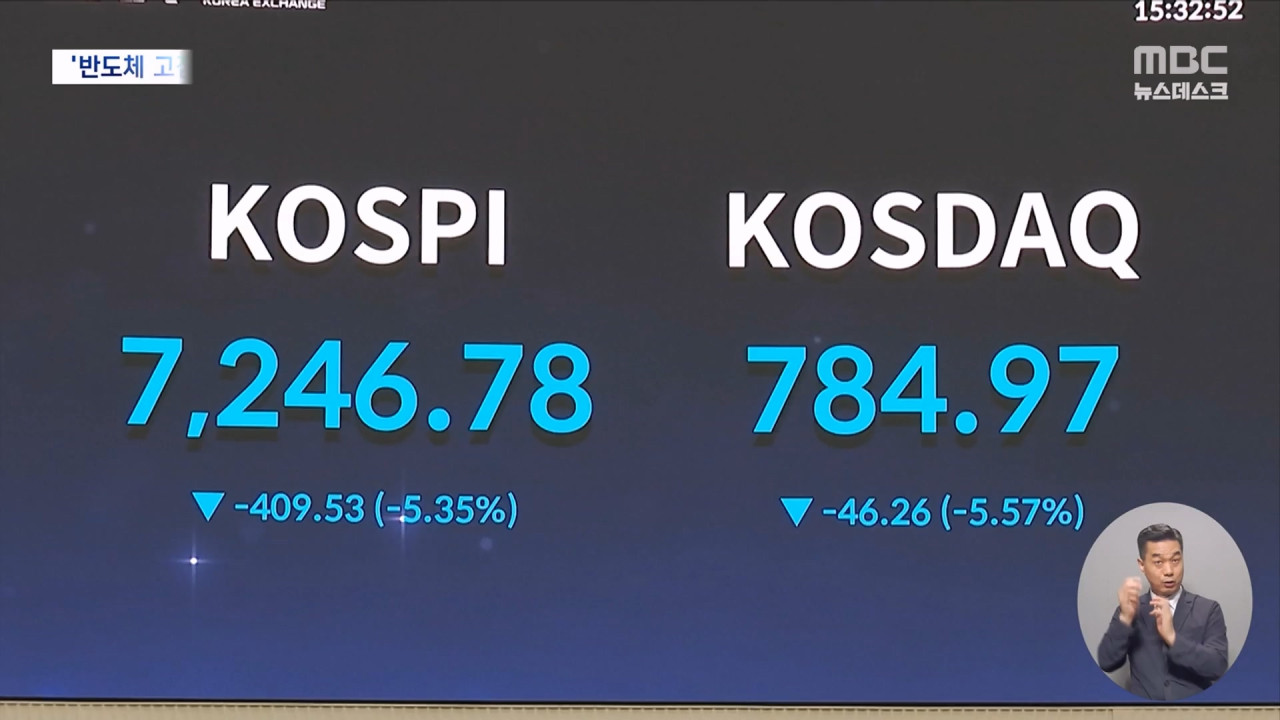

3. KOSPI slides 5% over two days on "semiconductor peak" fears

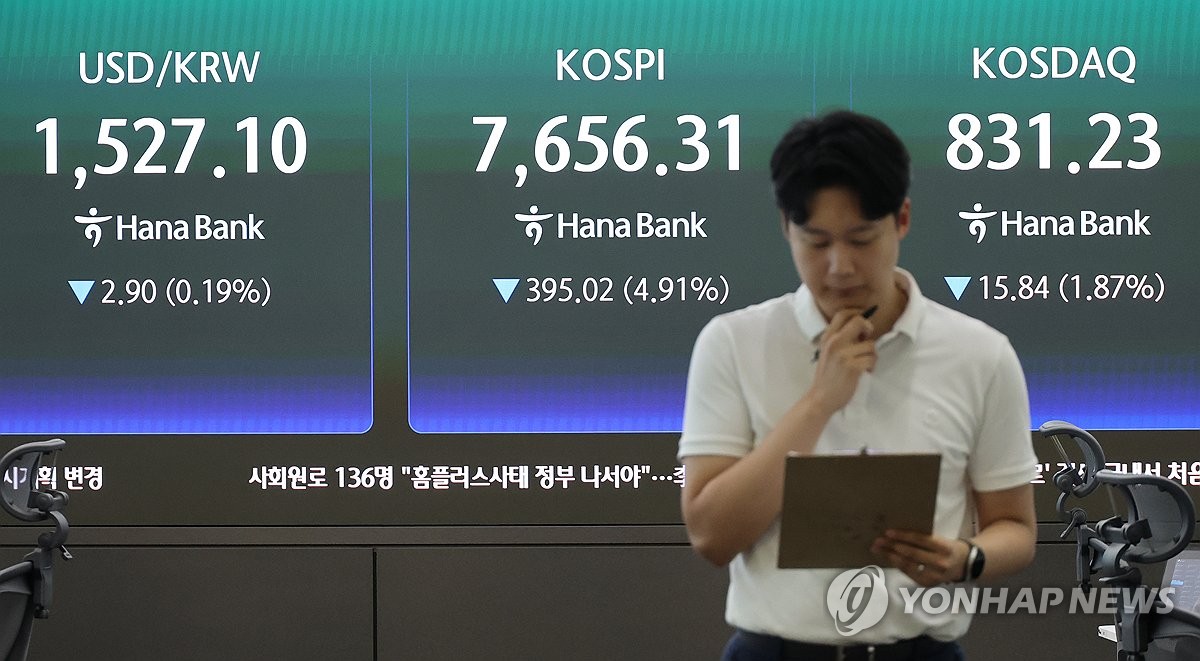

- What's happening?: Between the 7th and 8th, the KOSPI plummeted 5% over two consecutive days, triggering sidecars and circuit breakers. A combination of global economic slowdown concerns, Morgan Stanley’s "peak" warning for semiconductors, and Middle East conflict fears led to heavy selling by foreign and institutional investors. The KOSPI closed at 7,656 on the 7th (-4.91%) and 7,246.79 on the 8th (-5.35%).

- Market Impact: Broad losses across tech and semiconductors, with Samsung Electronics and SK hynix falling over 5%.

4. Circuit breakers hit three times in two weeks — volatility becomes "the new normal"

- What's happening?: Extreme volatility has become the norm, with circuit breakers or sidecars triggered three times in the first half of July. The rapid oscillation between rallies driven by the semiconductor boom and sell-offs caused by "peak" fears has left investor sentiment shaken.

- Market Impact: Deepening mismatch in supply-demand between retail, institutional, and foreign investors. The Volatility Index (VIX) is on the rise.

5. Foreigners turn to net buying for two days — KRW/USD stabilizes in 1,500 range

- What's happening?: Foreign investors turned to net buying on the KOSPI for the second consecutive day on the 9th, signaling interest in bargain hunting. The KRW/USD exchange rate closed at 1,506.1, showing a stable trend as bargain-hunting sentiment improved foreign inflows.

- Market Impact: A sign of improved liquidity and easing pressure from foreign selling.

Leading Sectors & Themes

Semiconductors

- Trend: Bullish early on the 9th thanks to U.S. chip gains. However, volatility remains extreme due to "peak" concerns.

- Key Stocks: Samsung Electronics (partial recovery after 5%+ drop), SK hynix (also slid).

Tech (IT & Telecom)

- Trend: Widely sold off as a target for foreign institutional selling. Rebounding on the 9th, but profit-taking pressure persists due to Middle East factors.

- Key Stocks: High volatility across large-cap IT.

Defensive & Value Stocks

- Trend: Relatively stronger amid tech weakness. With the second-half performance split between tech and value expected to be 47% vs. 53%, preference for value stocks is growing.

- Key Stocks: Financials and transport equipment.

Global Market Links

U.S. semiconductor rebound signals

- Despite global weakness on the 7th, U.S. chip stocks showed signs of a rebound, which sparked bargain hunting in Seoul on the morning of the 9th. However, Morgan Stanley’s "sell-off" warning continues to weigh on sentiment.

Renewed Middle East conflict fears

- Heightened Iran-Israel tensions are fueling risk aversion globally, limiting the KOSPI's upside and serving as a key driver of intraday volatility on the 9th.

Tomorrow's Checkpoints

- Sustainability of foreign net buying — Monitor whether buying continues or if Middle East escalations trigger renewed selling.

- U.S. July Employment Report (NFP) trends — Positive data is needed to soothe global slowdown fears.

- Volatility post-option expiration — Check for signs that supply-demand disruptions from weekly options are subsiding.

Investor Action Items

- Re-evaluate semiconductor entry points — Perspectives differ between the BOK (boom) and Morgan Stanley (peak). Consider mid-to-long-term bargain hunting if technical support (7,200–7,400) is retested.

- Monitor Middle East news — Real-time monitoring is essential, as escalating Iran-Israel tensions trigger risk-off sentiment.

- Track foreign supply-demand signals — Use the shift to net buying on the 9th as a benchmark for the next two weeks of market liquidity.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Explore related topics

Powered by