KOSPI hits record high: 2026-04-29 report

The KOSPI index is on a record-breaking rally, fueled by solid corporate earnings and easing geopolitical tensions, even breaking the 6,600 mark during intraday trading. Key variables to watch this week include the U.S. FOMC meeting, big tech earnings, and potential "Sell in May" seasonal pressure.

KOSPI Market Volatility and Influencing Factors — 2026-04-29

1. KOSPI Market Indicators and Flow Status

-

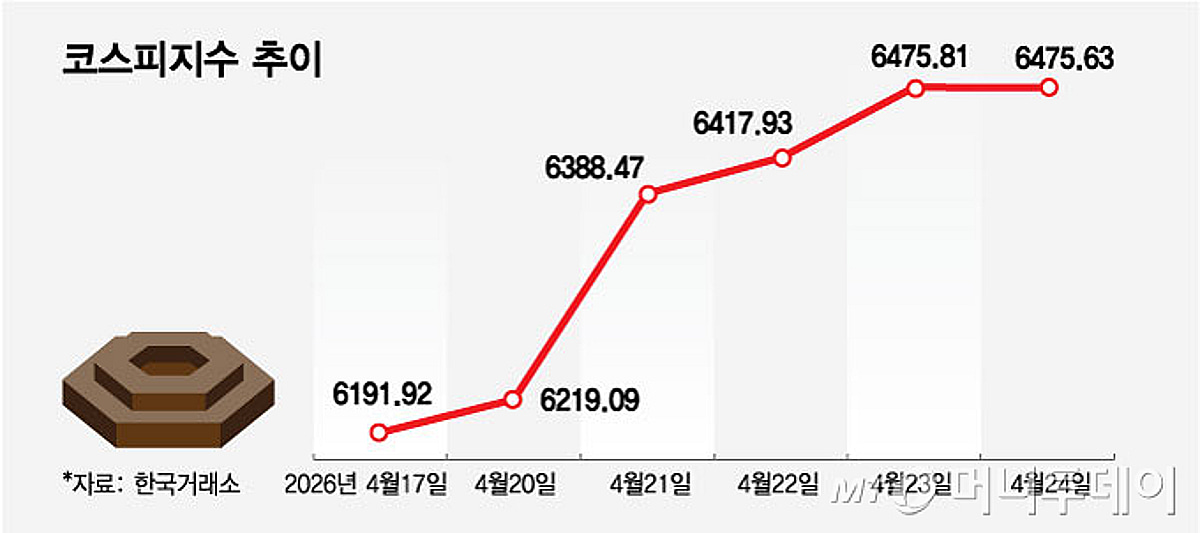

KOSPI Index: On April 27, the index hit an all-time high of 6,657.22 points during intraday trading. KOSPI opened at 6,533.60, up 57.97 points (0.90%) from the previous day, and maintained its strength throughout the session.

-

KOSPI Forward P/E: Despite breaking the 6,500 level, the forward P/E ratio dropped to 7.3x, leading to analysis that further upside potential remains.

-

KOSPI Annual Operating Profit Outlook: Forecasts have been adjusted upward by 29.8% compared to late March, now reaching 177.5 trillion KRW.

-

KRW/USD Exchange Rate: As of April 27, the USD/KRW rate stood at 1,474.0 KRW, a 0.18% drop from the previous day (a stronger won). Over the past month, the won has strengthened by 2.87%.

2. Key Volatility Factors Today

① Corporate Earnings Momentum — Growth Driver

Earnings outlooks for key sectors—such as semiconductors (with SK Hynix reporting record results), shipbuilding, defense, power equipment, MLCCs, and secondary batteries—are being revised upward, serving as the core engine for KOSPI's growth. An analyst at KB Securities noted, "We are currently in the period where the earnings of market-leading stocks, which have driven the domestic market, are being announced." More results from defense, power equipment, and MLCC firms are scheduled for this week.

② U.S. FOMC and Big Tech Earnings — Potential Volatility

Earnings releases from U.S. big tech giants like Alphabet and Amazon, along with the U.S. Federal Open Market Committee (FOMC) meeting scheduled for April 28–29 (local time), are considered the biggest volatility variables this week. A researcher at Samsung Securities analyzed, "The dominant driving force for the domestic market is AI; the AI theme, centered on semiconductors, has spread to power equipment, ESS, solar energy, and shipbuilding."

③ 5th Month "Sell in May" and Technical Burdens — Short-term Downside Risks

IBK Securities expects the KOSPI to follow a "weak early-to-mid month, rebound in late month" pattern in May. Technical pressure following April’s surge, the seasonal "Sell in May" pattern, and uncertainties surrounding Kevin Warsh as a candidate for the next Fed Chair are identified as potential short-term correction factors. However, analysts suggest that dip-buying during a mid-month pullback would be a sound strategy.

3. Macro Factors and Economic Indicators

① KRW/USD Exchange Rate — Trend toward a stronger Won

On April 27, the rate fell 0.18% to 1,474.0 KRW, continuing a trend where the won has strengthened by 2.87% over the last month. A stronger won typically encourages foreign capital inflows into the domestic market.

② Easing Geopolitical Risks — Reduced Market Impact

With renewed hopes for peace negotiations with Iran, the impact of geopolitical risk on the market has lessened, while profit outlooks for major domestic sectors are being rapidly upgraded. A division head at Daishin Securities explained, "The KOSPI is reflecting the improvement in industrial conditions and earnings that were previously overshadowed by geopolitical risks."

③ AI and Semiconductor-led Improvement — Expanding Sector Rotation

The improvement in the semiconductor sector, driven by the AI theme, is seeing a "rotation" into sectors like power equipment, ESS, solar, and shipbuilding. A researcher at Mirae Asset Securities stated, "We maintain our 'overweight' stance on semiconductors, defense, power equipment, nuclear energy, securities, banking, and holding companies, and suggest paying attention to KOSDAQ stocks that have become more attractive in price compared to KOSPI."

4. Summary and Investor Notes

The KOSPI continues its record-breaking rally, supported by fundamental growth in corporate earnings, a stronger won, and reduced geopolitical tensions. However, potential for short-term corrections remains due to technical overheating from the April surge, uncertainties surrounding the FOMC results, and the seasonal "Sell in May" pattern. Investors should keep a close eye on the FOMC results (April 28–29 local time) and upcoming big tech earnings, while keeping the strategy of buying the dip in early-to-mid May in mind.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by