Global & Korea Equity Market Intelligence — 2026-05-22

KOSPI closed at 7,847.71 on May 22, 2026, up +0.41% (+32.12 points), extending momentum from the previous day's historic rally that surged over 600 points (+8.42%). Global tailwinds came from Nvidia's strong earnings and expectations around U.S.-Iran negotiations, driving oil prices sharply lower and bond yields down—the Dow Jones finished at a new record high. Asia's next session saw Nikkei 225 jump +2.68% and Hang Seng rise +0.90%, making semiconductor strength led by Samsung Electronics and SK Hynix the key variable for sustained rallies.

Global & Korea Equity Market Intelligence — 2026-05-22

Market Snapshot — By the Numbers

| Index | Close | Change | % Change |

|---|---|---|---|

| KOSPI | 7,847.71 | +32.12 | +0.41% |

| KOSDAQ | No data | — | — |

| S&P 500 | 7,445.72 | +12.75 | +0.17% |

| Nasdaq | 26,293.10 | +22.74 | +0.09% |

| Dow Jones | 50,285.66 | +276.31 | +0.55% |

| Nikkei 225 | 63,339.07 | +1,654.93 | +2.68% |

| Hang Seng | 25,614.56 | +228.04 | +0.90% |

Korea Market Deep Dive

KOSPI

- Close: 7,847.71 (+0.41%, +32.12 pt)

- Intraday range: 7,780.13 – 7,886.64

- 52-week range: 2,589.51 – 8,046.78

- Market context: Following May 21's single-day surge of over 600 points to 7,815.59 (+8.42%), May 22 saw a modest continuation of the rally. Samsung Electronics' labor agreement and improving semiconductor outlook were the main drivers.

KOSDAQ

- Close: Detailed data unavailable for this report as of May 22. As of May 21, trading occurred around the 1,100 level following a buy-side circuit breaker trigger, with semiconductors and biotech dominating volume.

Top Movers (Korea)

Gainers — Major Stocks

- Samsung Electronics (005930) (+Up): Labor union wage agreement finalized and AI memory supercycle expectations drove historic rally on May 21. Korea Investment Securities set a target price of 570,000 KRW.

- SK Hynix (000660) (+Up): Nomura raised its target price to 4,000,000 KRW. Surging HBM demand from AI applications triggered valuation re-rating.

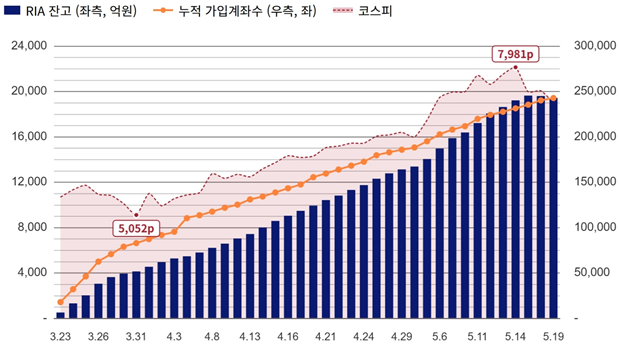

- Samsung Securities client buy concentration (+Up): As of May 21, approximately 24–25% of Samsung Electronics and SK Hynix shareholders aggressively added positions near all-time highs. RIA account balances broke through 1.94 trillion KRW.

Decliners — Major Stocks

- Continuous foreign net selling (KOSPI-wide) (−Down): Foreign investors maintained at least 9 consecutive trading days of net selling through May 20, applying profit-taking pressure on semiconductors.

- U.S. mega-cap tech ETF-linked stocks (−Down): Korean investors pivoted from U.S. tech and leveraged ETF positions into Samsung Electronics and SK Hynix, creating relative weakness in linked domestic products.

- May 20 decline-related stocks (−Adjustment): May 20 saw foreign investor exodus push KOSPI to 7,000 levels early session, with semiconductors experiencing profit-taking sales.

Sector Flows

- Semiconductors: Samsung Electronics (005930) and SK Hynix (000660) led KOSPI's May 21 surge. Samsung's catalyst: labor agreement resolution plus strong AI memory demand; SK Hynix: HBM boom. Nomura raised its 2025 KOSPI target to 10,000–11,000, setting Samsung Electronics at 590,000 KRW and SK Hynix at 4,000,000 KRW, declaring an "AI-driven memory supercycle."

-

Battery & EV: No recent data available for this report period (post-May 20)—no new sector catalysts confirmed.

-

Biotech & Healthcare: No major biotech momentum data confirmed for this report period.

-

Retail investor rotation: Korean investors exited U.S. mega-cap tech and leveraged ETF positions to concentrate in Samsung Electronics and SK Hynix. RIA account balances reached 1.94 trillion KRW, with 24–25% of Samsung Securities clients adding positions near all-time highs.

Global Drivers Behind Today's Tape

- Nvidia earnings surprise: Nvidia reported results after market close on May 20, beating both revenue and profit expectations. Stock dipped in after-hours trading post-release. Strong AI chip demand confirmation provided tailwind to Korean semiconductor names.

- U.S.-Iran nuclear talks expectations → oil plunge: Reports of imminent U.S.-Iran negotiation agreement drove May 20 oil prices sharply lower and bond yields down—supportive for equities, sparking a 650-point Dow surge. Geopolitical tension relief expectations extended into May 21.

- U.S. Treasury yield trends: May 19 saw 10-year yields hit 1-year highs, dragging S&P 500 and Nasdaq down 3 straight sessions; May 20–21 saw yields ease alongside oil declines, driving equity rebound.

- Dow hits new high: May 21 saw Dow Jones close at 50,285.66, a new record. Solid economic data and AI rally underpinned resilience amid oil and rate volatility.

- Nikkei 225 sharp rebound (+2.68%): May 22 Nikkei closed at 63,339.07, up 1,654.93 points in a single session. Taiwan's weighted index also rallied +2.17%, reconfirming Asia's semiconductor rally.

Asia Read-Through

May 22's Asia session saw Nikkei 225 surge +2.68%, Hang Seng rise +0.90%, and Taiwan's weighted index climb +2.17%, spreading semiconductor strength across the region. With U.S. Dow at record highs and oil/rate volatility moderating, risk-on sentiment revived; dollar index (DXY) held steady at 99.26. Korea's next session hinges on foreign investor selling flow reversal, Nvidia earnings follow-through, and Samsung Electronics labor agreement momentum sustainability.

What to Watch Next

- Economic data: U.S. weekly jobless claims (due May 22), Bank of Korea policy meeting schedule, and Korean CPI monitoring.

- Earnings focus: Nvidia earnings reverberations continue / Korea's major semiconductor and battery firms' 2Q guidance and business conference calls.

- Key technical levels: KOSPI 7,800 support hold (vs. 8,000 retest attempts), 7,500 as near-term support zone. Watch for demand-supply inflection after 9+ consecutive days of foreign selling.

- Macro watch: KRW/USD rate moves, U.S. 10-year Treasury yield, WTI crude (U.S.-Iran negotiation progress), HBM spot pricing trends.

Reader Action Items

-

Korean retail investors: 24–25% of Samsung Electronics and SK Hynix shareholders are showing strong conviction, adding near all-time highs. However, 9+ consecutive days of foreign net selling is a short-term volatility warning. Plan partial profit-taking and rebalancing above 8,000, but AI memory supercycle theme remains valid on a medium-term view.

-

Global Korea exposure investors: Hedge costs for KRW and directional KRW/USD positioning need review. With dollar index at 99.26 parity, foreign outflows risking won weakness could widen ADR (KB Financial, POSCO, etc.) vs. local stock spreads. Taiwan weighted index correlation (+2.17%) monitoring is essential.

-

Contrarian take: Foreign selling for 9+ days while KOSPI closed +0.41% signals domestic demand (retail + institutional) absorption strength. Market consensus reads "foreign return = more upside," but reality shows retail and institutions already digesting foreign flows entirely—meaning foreign re-entry's upside runway may be tighter than consensus expects.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by