InsurTech Innovation — 2026-04-24

Global InsurTech funding hit its lowest point of 2026 in March, with only 10 deals raising roughly $237 million — a steep drop from February's $1 billion-plus — while the broader market projects explosive growth toward $460 billion by 2035. The dominant theme this week is the accelerating mainstreaming of AI across underwriting, claims, and parametric products, moving from experimental to strategic necessity. European insurtechs are also quietly staging a comeback, with VCs flagging a new cohort of AI-native startups worth watching.

InsurTech Innovation — 2026-04-24

Headline Deals (at least 3)

Note: The freshest verified funding data available within the 7-day window is limited. The items below represent the most current confirmed events from research published after April 17, 2026.

Global InsurTech — March 2026 Funding Cooldown (Reported This Week)

- What they do: Sector-wide review of InsurTech investment activity

- Segment: Cross-sector

- Investors or partners: Multiple VCs across P&C, Health, and Reinsurance

- Valuation / traction: 10 deals, ~$237M raised in March 2026 — lowest monthly total of the year; down sharply from $1B+ in February and $420M in January

- Why it matters: The funding cooldown signals a flight to quality rather than volume, with investors becoming more selective after the 2025 rebound. Incumbents should see this as an opportunity to acquire cash-constrained insurtechs at favorable terms before the next funding cycle.

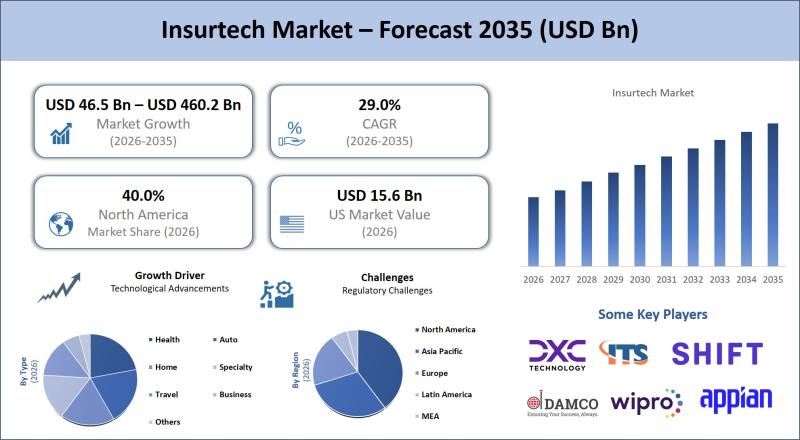

InsurTech Market — $460.2 Billion Projection by 2035 (Published This Week)

- What they do: Market sizing and growth trajectory analysis for the global InsurTech sector

- Segment: Cross-sector / AI-led transformation

- Investors or partners: N/A (market research)

- Valuation / traction: Market expected to rise from $46.5 billion in 2026 to $460.2 billion by 2035, at a 29.0% CAGR

- Why it matters: A near-tenfold growth projection in under a decade reflects the pace at which AI is compressing insurance's traditionally slow transformation cycle. Carriers that delay digital core investment risk being structurally uncompetitive by 2028–2030.

Federato — $100M Series D (Confirmed in Trade Press This Week)

- What they do: AI-powered underwriting workbench that helps carriers manage portfolio risk exposure in real time

- Segment: P&C / Reinsurance / Broker-tech

- Investors or partners: Goldman Sachs (lead)

- Valuation / traction: Not disclosed

- Why it matters: Goldman Sachs leading an insurtech underwriting round is a strong signal that institutional capital is converging on AI-native risk management infrastructure. Competitors in the underwriting workflow space — including legacy vendors — face accelerating displacement pressure.

Product & Technology Launches (at least 3)

- AI in P&C Insurance — Cross-Carrier Adoption Wave: Digital Insurance's opinion piece published this week confirms that in 2026, AI is "no longer an experimental technology — it is a strategic necessity embedded across the insurance value chain." Key deployment zones include claims triage, fraud detection, underwriting scoring, and customer service automation. What's novel is the speed of convergence: carriers that piloted AI in one function are now deploying it enterprise-wide.

-

Parametric Products — Satellite + AI Goes Mainstream: According to Qover's 2026 predictions report (cited this week), "parametric products powered by satellite imagery analytics and AI-driven catastrophe models are no longer experimental." These contracts pay out automatically upon trigger events, removing adjuster touchpoints entirely. The novelty is scale: what was a niche offering for specialty risk is now entering SME and retail distribution channels.

-

Roots Automation — Straight-Through Claims Processing Forecast: Roots Automation projects that by late 2026, AI will handle 70%–90% of simple claims through straight-through processing with zero adjuster involvement. The target segment is personal lines and small commercial claims. What's novel is the specificity of the projection — and the implied workforce restructuring required at tier-1 carriers.

Incumbent Carrier Moves

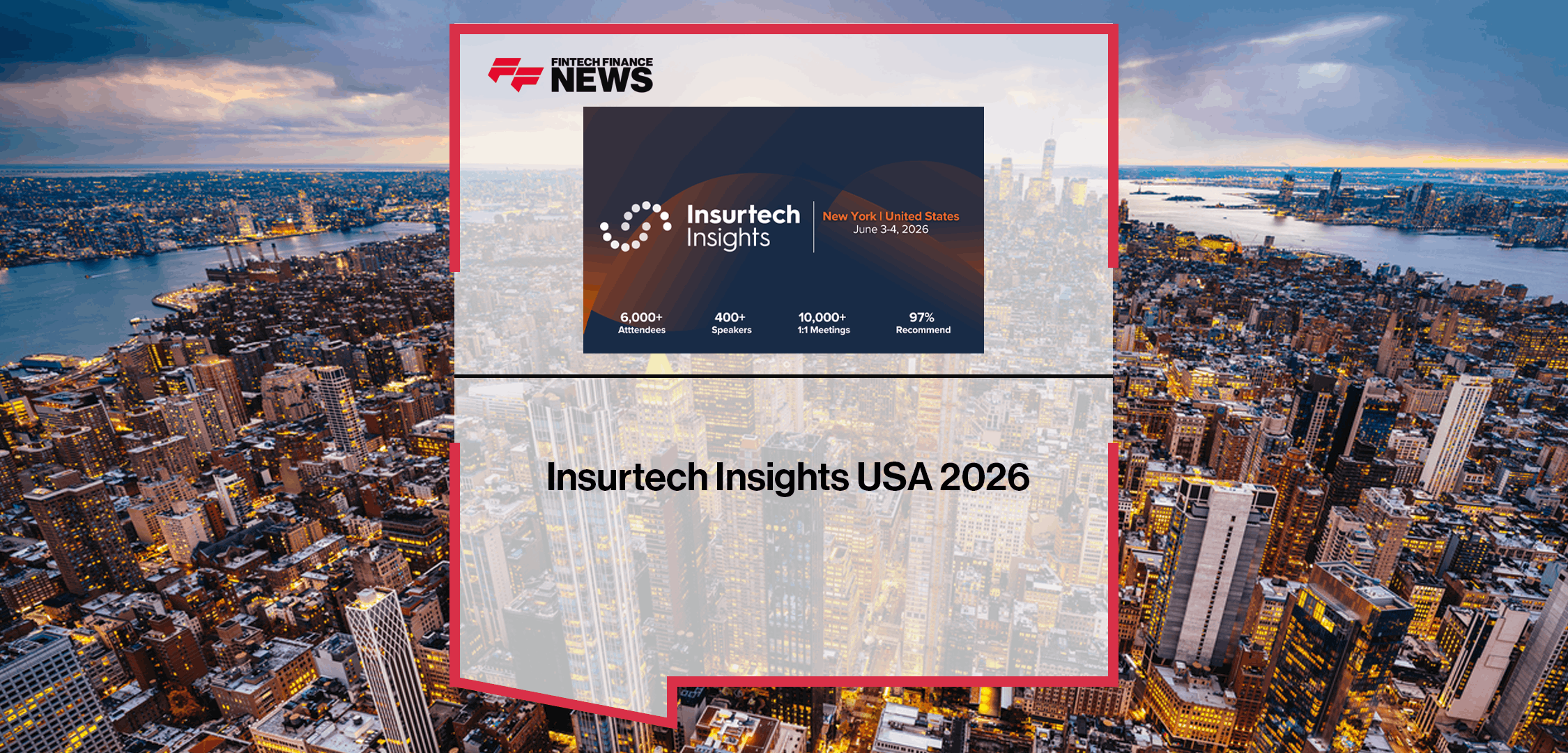

- Insurtech Insights USA 2026 — Carrier-Startup Convergence Event: The leading U.S. InsurTech conference, bringing together 6,000+ insurance professionals and C-level executives, is confirmed active this week per FF News. The event functions as a live deal-making and partnership formation venue where incumbent carriers formally engage the startup ecosystem. Strategic rationale: carriers use the event to evaluate acquisition targets, pilot technology vendors, and signal digital transformation priorities to the market.

- European Carrier Ecosystem — VC-Backed Restart: Sifted's updated VC watchlist (published approximately one week ago) confirms that "European insurtechs are on the rebound after a tricky few years, with investor interest in the sector steadily ticking up amid an AI-powered boom." Multiple incumbent-adjacent startups in the EU are receiving fresh backing, with VCs explicitly naming AI-native architecture as the primary differentiator. This signals that European carriers — historically slow to partner externally — are facing renewed competitive pressure from venture-backed challengers.

Theme Deep-Dive: AI Across the Insurance Value Chain

The week's dominant theme is unambiguous: AI has crossed from pilot to production across the insurance industry, and the competitive gap between early adopters and laggards is widening rapidly.

Two contrasting approaches are emerging.

Approach 1 — Horizontal AI Infrastructure (Federato model): Companies like Federato are building AI-native operating layers beneath the carrier's existing systems. Their $100M Series D, led by Goldman Sachs, funds a platform that sits in the underwriter's workflow and optimizes portfolio exposure in real time. The bet here is that underwriters will never be replaced — but their tools will be entirely rebuilt. Federato's approach targets the complexity problem: large commercial and specialty lines where human judgment remains essential, but data synthesis is too slow without AI assistance.

Approach 2 — Autonomous Claims Processing (Roots Automation model): Roots Automation takes the opposite philosophical stance. Rather than augmenting humans, it targets the elimination of human touchpoints in simple claims. Their projection of 70%–90% straight-through processing by late 2026 is aggressive — but credible given the maturity of document AI and NLP. The target segment is high-volume, low-complexity personal lines claims where speed and cost-per-claim matter more than nuanced judgment.

Parametric insurance represents a third convergence point. Per Qover's 2026 report (cited in FinanceX Magazine this week), satellite imagery + AI catastrophe models are enabling truly automated parametric contracts at scale. These products remove the claims process entirely — payout is triggered by a verified external event, not an adjuster's assessment. The implication for incumbents is structural: if parametric products expand from specialty into mainstream property cover, the claims workforce footprint shrinks dramatically.

Digital Insurance's opinion piece this week captures the synthesis: "In 2026, artificial intelligence is no longer an experimental technology — it is a strategic necessity embedded across the insurance value chain." The velocity of this shift means carriers that treated AI as a 2027–2028 priority are already behind the frontier.

M&A, Exits & Shutdowns

- Quiet week for confirmed M&A transactions and IPO activity within the verified 7-day window. The broader context is that March's funding drought ($237M across only 10 deals) may be accelerating quiet acquisition conversations, but no transactions have been publicly confirmed post-April 17. Watch for announcements at Insurtech Insights USA 2026.

By the Numbers

- Disclosed funding this period (March 2026, reported this week): ~$237M (10 deals) — lowest monthly total of 2026

- Largest confirmed round (reported this week): Federato ($100M Series D)

- Most active investor(s): Goldman Sachs (Federato Series D); Peak XV Partners (Plum Series B, India — reported earlier but worth noting as context)

- Hottest sub-segment: AI underwriting infrastructure — Goldman Sachs' entry into the space confirms institutional conviction

- Geographies in focus: United States (Federato, Roots Automation), Europe (VC rebound per Sifted), India (Plum)

What to Watch Next

-

Insurtech Insights USA 2026: With 6,000+ attendees and C-suite concentration, expect partnership and pilot announcements to emerge in the days following the event. Carrier-startup deal flow typically accelerates in the two weeks post-conference.

-

AI Claims Automation Milestones: Roots Automation's 70%–90% straight-through processing target for late 2026 will face its first real stress tests as summer CAT season approaches. Watch for carriers publicly disclosing claims AI performance metrics for the first time.

-

European InsurTech Funding Rebound: Sifted's VC watchlist signals that 16 European insurtechs are poised for breakout years. Monitor for Series A and B announcements from AI-native European players over the next 30–60 days, particularly in embedded and parametric verticals.

Reader Action Items

-

For incumbent carrier strategy teams: The Federato/Goldman Sachs deal is a wake-up call — AI underwriting infrastructure is attracting tier-1 institutional capital. Audit your current underwriting workflow tooling immediately: if it isn't AI-native or integrating with AI-native platforms, you are building technical debt against a $460B market trajectory. Prioritize vendor evaluations for underwriting AI and claims straight-through processing before Q3 2026.

-

For founders / operators: The funding drought (only 10 deals in March at $237M total) reveals a white space: capital is concentrating in proven, revenue-generating insurtechs with clear ROI stories. Founders building in claims automation, parametric infrastructure, or AI underwriting augmentation should position their pitch around loss ratio improvement metrics — not technology novelty. Carriers are buyers, not experimenters, in 2026.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by