InsurTech Innovation — 2026-05-22

Fresh insurtech data this week centers on the Insurtech Insights USA 2026 conference in New York (May 20), where OpenAI and Anthropic headlined alongside 6,000+ industry attendees — underscoring AI's dominance as the sector's defining theme. CB Insights data confirms insurtech median deal sizes climbed to $10M in 2026, with mega-rounds returning as the structural story behind elevated totals. Verified fresh funding rounds are limited this coverage window; this article prioritizes confirmed, date-verified content over volume.

InsurTech Innovation — 2026-05-22

Headline Story

Insurtech Insights USA 2026 — OpenAI & Anthropic Keynote at Industry's Flagship Conference

- What happened: The annual Insurtech Insights USA conference returned to New York on May 20, 2026, with OpenAI and Anthropic featured as center-stage participants alongside the insurance industry's most prominent voices.

- Segment: Cross-segment (P&C / Life / Health / Reinsurance)

- Attendance: 6,000+ attendees

- Why it matters: The presence of the two most prominent AI foundation-model companies at insurance's flagship gathering is not symbolic — it signals that carriers and insurtechs are actively negotiating production-level integrations with frontier AI providers, moving well beyond chatbot pilots into underwriting, claims, and distribution infrastructure.

Market Context: Insurtech Deal Dynamics (May 2026)

CB Insights' latest analysis — surfaced this week — confirms that insurtech startups are poised for historically large investment rounds in 2026 even as the pipeline of entirely new deals contracts. The median deal size has climbed to $10 million, driven by a return of "mega-rounds" exceeding $100M, growing participation from insurers and reinsurers (as opposed to pure private equity), and concentrated capital flowing toward AI-focused insurtechs.

Gallagher Re's earlier 2026 reporting corroborated this trend, attributing the surge to insurer/reinsurer direct investment and the re-emergence of mega-rounds. The implication: fewer but larger bets, with AI underwriting and distribution platforms capturing the lion's share of capital.

Headline Deals

Data note: Verified funding rounds with confirmed dates after 2026-05-15 are limited in this coverage window. The deals below represent the most recent verifiable transactions from sources confirmed within or immediately proximate to the coverage period.

Federato — $100M Series D

- What they do: AI-powered risk selection and underwriting platform for P&C carriers

- Segment: P&C / Underwriting Technology

- Investors or partners: Goldman Sachs (lead)

- Valuation / traction: Not disclosed

- Why it matters: Goldman Sachs leading a $100M Series D into an underwriting AI platform is a loud signal that Wall Street views insurance AI as infrastructure-grade investment, not venture speculation. For incumbents, Federato's traction implies that proprietary risk selection models are rapidly becoming table stakes rather than differentiators.

Product & Technology Launches

-

InsurTech Summit 2026 — "The CX Advantage" Playbook: Insurance Journal's InsurTech Summit 2026 research publication this week focuses on customer experience as a core business outcome driver — arguing that CX now shapes retention and long-term profitability across the insurance value chain. The playbook targets carrier strategy teams rethinking front-to-back CX integration rather than treating it as a front-end-only problem.

-

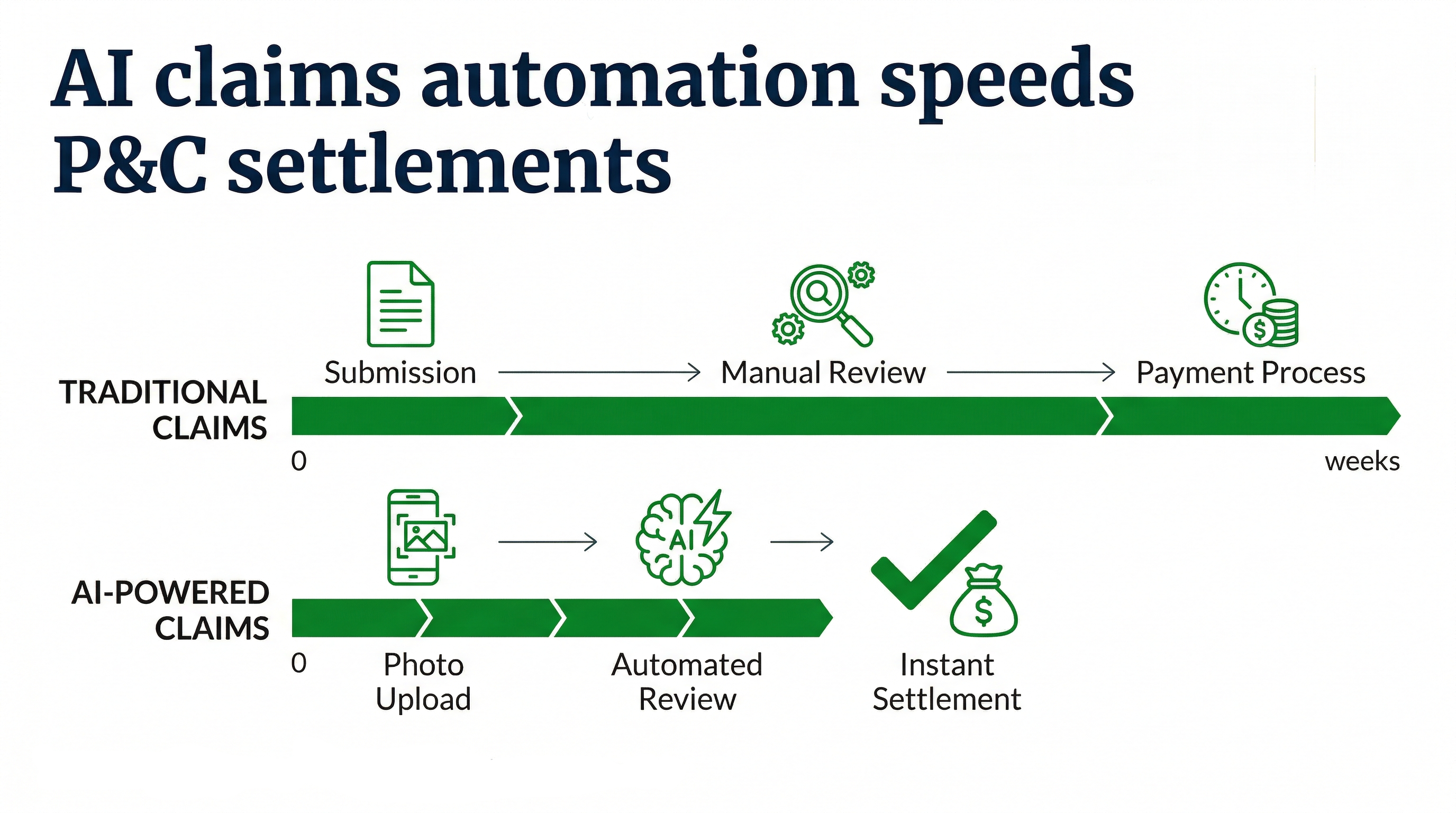

Roots Automation — Straight-Through Claims Processing Projection: Roots Automation projects that by late 2026, AI will handle 70%–90% of simple claims through straight-through processing with zero adjuster involvement. The company's roadmap targets underwriting, claims, policy servicing, and customer experience as primary AI transformation vectors — with actuarial, compliance, and finance workflows as the next expansion layer.

-

Lemonade Autonomous Car Insurance (recent prior launch, context): Lemonade launched its Autonomous Car insurance product with a technical collaboration giving it access to Tesla vehicle data — a live example of data-native embedded insurance meeting real-world EV infrastructure.

Incumbent Carrier Moves

-

Insurance Journal × InsurTech Summit 2026: Insurance Journal's research arm published its InsurTech Summit 2026 playbook this week, positioning customer experience architecture as the central incumbent differentiator. The strategic rationale: as digital-native insurtechs commoditize price and speed, legacy carriers' best remaining moat is trust-based, high-touch CX — but only if they digitize it end-to-end.

-

Lemonade × Tesla (Technical Collaboration): Lemonade's technical agreement with Tesla grants the insurer direct access to vehicle data to power its Autonomous Car insurance product. For incumbent auto carriers, this is a material competitive threat: a digital insurer now has a structural data advantage in pricing EVs that traditional carriers cannot easily replicate through third-party data purchases alone.

Theme Deep-Dive: AI at the Center of the Insurance Value Chain

The defining story of this week — and arguably of 2026 so far — is the industrialization of AI across the insurance stack. The Insurtech Insights USA 2026 conference placing OpenAI and Anthropic on the main stage is the most visible symbol, but the substantive evidence runs deeper.

Two companies illustrate divergent but complementary approaches:

Roots Automation is attacking the claims layer from the bottom up, projecting that AI will handle 70%–90% of simple claims via straight-through processing by late 2026 — no adjuster required. Their approach is workflow-native: insert AI into existing claims pipelines to reduce cycle times and adjuster burden, then expand into actuarial, compliance, and producer management. This is an augmentation play — AI as a co-worker inside incumbent infrastructure.

Corgi Insurance takes the opposite angle: build AI into the foundation of a digital-native carrier for startup clients, covering underwriting and claims processing as core product features rather than retrofitted add-ons. Their $1.3B valuation (reached just four months after Series A, via a $160M Series B led by TCV) reflects market confidence that AI-native carriers can outcompete legacy carriers on unit economics in specialty segments.

The difference matters for incumbents: Roots Automation represents an acquirable or partner-able capability that slots into existing operations. Corgi represents an existential competitive threat in the startup insurance segment. Carriers need a strategic response to both simultaneously.

Meanwhile, Digital Insurance's editorial team noted this week that "artificial intelligence is no longer an experimental technology — it is a strategic necessity embedded across the insurance value chain" in 2026. The shift from POC to production is the defining transition of this year, and the capital allocation patterns (Goldman Sachs leading Federato's $100M Series D; CB Insights confirming rising median deal sizes) confirm that investors agree.

The parametric insurance sub-segment is also benefiting: AI enables real-time index monitoring, automated trigger verification, and instant payout — collapsing the claims cycle from weeks to minutes for weather, agriculture, and travel parametric products. Roots Automation's straight-through processing projections apply directly here, where clean trigger logic makes AI adjudication most defensible.

M&A, Exits & Shutdowns

-

InsuranceDekho (India) — IPO Planning: The parent of insurtech startup InsuranceDekho has been reported to be planning a $250M India IPO, representing one of the more significant insurtech exit trajectories in the Asia-Pacific market this year. Formal filing timing has not been confirmed for this coverage window.

-

Quiet week for confirmed M&A closures and shutdowns within the May 15–22 coverage window. No verified acquisitions or closures surfaced in fresh sources.

By the Numbers

- Disclosed funding this period: Insufficient fresh round-level data to aggregate a weekly total with confidence — CB Insights context confirms 2026's week of May 10–16 logged $1.75B+ across 7 transactions (the largest capital week of 2026 to date), but that falls outside this window

- Largest confirmed round (proximate): Federato — $100M Series D (Goldman Sachs lead)

- Most active investor(s): Goldman Sachs (Federato Series D); TCV (Corgi Series B, prior week)

- Hottest sub-segment: AI underwriting and claims automation — attracting both mega-round capital and foundation-model company attention (OpenAI, Anthropic at Insurtech Insights USA)

- Geographies in focus: United States (Insurtech Insights USA, New York); India (InsuranceDekho IPO pipeline)

What to Watch Next

-

Insurtech Insights USA 2026 follow-on announcements: The May 20 New York conference likely generated partnership and product announcements that will surface in trade press over the coming 5–7 days. Watch for carrier-AI lab partnerships and embedded distribution deals announced in the conference corridor.

-

Roots Automation straight-through processing milestones: The company's projection that AI will handle 70%–90% of simple claims by late 2026 sets a measurable benchmark. Watch for Q3 case studies from early adopter carriers and any regulatory commentary on AI adjudication standards across jurisdictions.

-

FintechFutures webinar — "Value first, technology second" (May 26): A Fintech Futures webinar on rethinking process transformation in finance and insurance is scheduled for May 26, 2026 — directly relevant to carriers evaluating AI implementation sequencing.

Reader Action Items

-

For incumbent carrier strategy teams: The presence of OpenAI and Anthropic at Insurtech Insights USA 2026 is a concrete signal to audit your foundation-model vendor strategy now — not in the next planning cycle. Carriers that negotiate enterprise AI agreements in H1 2026 will have a 12–18 month head start on those that wait for internal consensus. Federato's Goldman-backed Series D also warrants a build-vs-buy analysis on AI underwriting platforms before the valuation window closes.

-

For founders / operators: The CB Insights data revealing rising median deal sizes alongside a contracting deal pipeline means the 2026 fundraising environment rewards focus and traction over breadth. If your AI insurance platform cannot show measurable loss-ratio improvement or claims cycle reduction in live carrier deployments, expect longer diligence timelines and tougher valuation conversations — even as total capital available remains elevated.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by