Small Business & Franchise — 2026-04-28

The dominant story this week is the SBA's shift in contracting priorities — moving toward veteran-owned firms and anti-fraud efforts — alongside a near-finalized CFPB rule that will mandate demographic data collection on small-business borrowers. On the franchise front, the buildout and real estate timeline guide from 1851 Franchise is drawing attention from prospective buyers navigating a complex opening environment, while a veteran franchisee story out of the lawn care sector offers a concrete success template for operators considering a second-career pivot.

Small Business & Franchise — 2026-04-28

Key Highlights

-

SBA pivots contracting goalposts toward veteran-owned firms and fraud prevention. The Small Business Administration is publicly signaling a bigger focus on contracts with veterans-owned businesses and is stepping up efforts to root out fraud within its contracting programs. The shift could meaningfully alter which small businesses capture federal contract dollars in 2026.

-

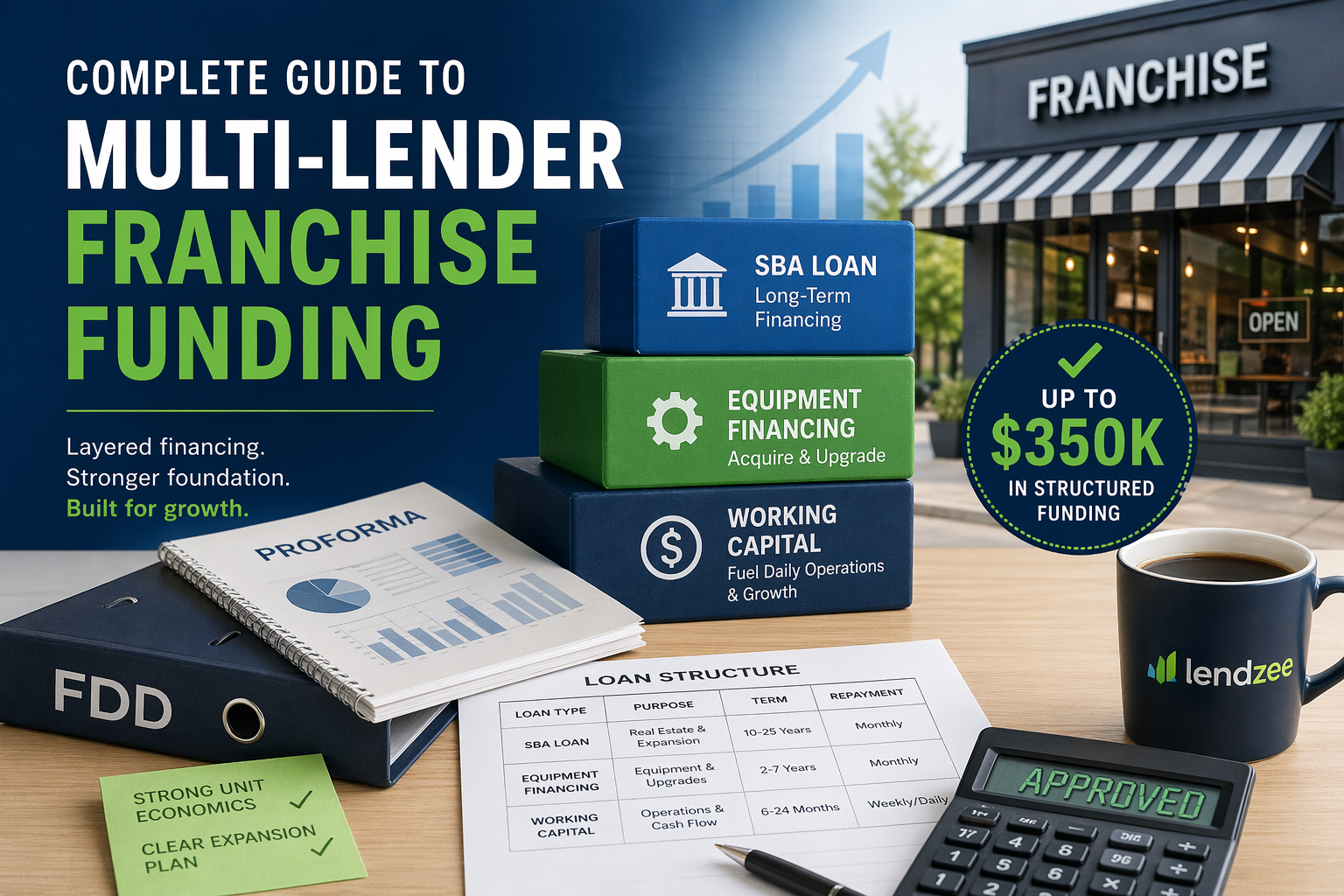

Multi-lender franchise funding stacks are reshaping how first-time franchisees get deals done. A detailed 2026 guide from Lendzee explains how buyers can layer SBA 7(a) loans with soft-credit pre-approvals and secondary lenders to cover the full investment, reducing the barrier to entry for franchisees who fall short of traditional single-lender requirements.

- Franchised restaurant chains underperform corporate-operated locations in current market. Restaurant Business Online reports that top 500 chains operating their own locations generated more than three times the median sales growth compared to franchised counterparts — a data point that will matter to anyone underwriting franchise deals right now.

- Real estate and buildout timelines are the hidden franchise killer in 2026. A new guide from 1851 Franchise highlights the full 18-month site-approval-to-opening journey, warning prospective buyers that construction delays and permitting snags remain the most common reasons new franchise locations miss their projected launch dates.

%2Fstory1%2F2731743%2Fdcade9d6ea679cbf40701a9d35fb2d9f2259.jpg)

- Field support quality in the first 90 days is becoming a top franchisee selection criterion. 1851 Franchise's latest buyer guide spotlights how franchisor field support during training, opening, and the critical first-90-day ramp period increasingly differentiates high-performing systems from underperformers — a due-diligence checklist item that many FDD readers still skip.

%2Fstory1%2F2731697%2F1773763483_2731697.png)

Policy & Funding Watch

1. CFPB's small-business demographic data rule is near the finish line. The Consumer Financial Protection Bureau is expected to soon finalize a rule mandating that lenders collect demographic data on small-business borrowers — including data on women- and minority-owned businesses. The goal is to ensure equal credit access, but the rule has faced sustained opposition from banks and lenders who argue it creates compliance burdens. Effective date: Not yet set; finalization imminent per American Banker reporting this week. Affects all depository and non-depository lenders making small-business loans.

2. SBA contracting rules are shifting to favor veteran-owned firms. The SBA is recalibrating how small-business federal contracting goals are set, with a stated emphasis on increasing contracts awarded to veteran-owned businesses and tightening fraud-detection mechanisms. This affects small businesses that rely on set-aside contracts, particularly in defense and professional services sectors. Watch for updated SBA guidance in coming weeks.

3. SBA 7(a) loan requirements for franchise buyers remain a critical filter. MBB Management published an updated explainer this week on SBA 7(a) eligibility for franchise buyers, stressing that franchisors must appear on the SBA Franchise Directory (reinstated June 2025) for their franchisees to access SBA financing. Buyers whose target franchise brand is not on the directory face a significant funding gap. Affects any prospective franchisee using SBA financing.

Franchise Spotlight

1. Lawn Doctor — Veteran-friendly franchise finding a second-career audience Landscape Management's 2026 Franchise Guide featured the story of Rafael Valle, a long-time military veteran who transitioned into green industry franchising via Lawn Doctor. The brand is positioning itself as a top destination for veterans seeking franchise ownership, an audience that frequently benefits from SBA's Patriot Express and veteran-loan advantage programs. Lawn Doctor is a recurring pick in franchise rankings for its recurring-revenue model (residential lawn care contracts). Specific investment figures were not disclosed in the coverage; prospective buyers should request the current FDD for Item 7 (initial investment) and Item 19 (financial performance representations). The story highlights that field support and the brand's existing customer base were the decisive factors for Valle.

2. The franchise buildout reality check — what operators don't budget for 1851 Franchise's updated real estate guide is essentially a buyer's brief on the hidden costs and timelines that derail new franchise openings. Key insight: the guide notes a typical 18-month runway from site approval to a functioning store, with permitting and construction snags as the primary schedule risks. This is especially relevant in hot secondary and tertiary markets where contractor availability is constrained. For any concept with significant build-out costs (QSR, fitness, healthcare), understanding this calendar before signing a lease is non-negotiable. Buyers should cross-reference Item 11 and Item 12 of the FDD for territory rights and renewal terms.

Owner Success Stories

1. Rafael Valle, Lawn Doctor franchisee — Military veteran finds profitable second chapter in green industry After a long career in the U.S. military, Rafael Valle became a Lawn Doctor franchisee and is now featured as a model case in Landscape Management's 2026 Franchise Guide. Valle credits the brand's built-in recurring-revenue model and robust field support for the business's early stability. His experience underscores a broader trend: veterans transitioning to franchise ownership at above-average rates, supported by favorable SBA lending programs. Specific revenue figures were not disclosed in the coverage.

2. Multi-unit franchisee financing evolution — the layered capital stack approach Lendzee's 2026 guide profiles first-time franchise buyers successfully using multi-lender stacks — combining an SBA 7(a) primary loan with a soft-credit pre-approval and a secondary lender — to close deals that would otherwise be declined by a single lender. While this guide does not name a specific operator, its data-backed framework represents a documented shift in how buyers at the $300K–$800K total investment range are structuring their financing.

Market & Capital Pulse

Franchise lending conditions in late April 2026 remain shaped by two converging forces: the SBA Franchise Directory (reinstated June 2025) continues to serve as a critical gateway for SBA-backed franchise financing, and multi-lender capital stacks are increasingly common as buyers bridge the gap between single-lender qualification ceilings and actual investment requirements. The pending CFPB demographic-data rule is injecting uncertainty into small-business lending compliance costs, which could incrementally tighten credit availability for minority- and women-owned businesses in the near term — the opposite of the rule's intent — before long-run data collection normalizes. On the M&A front, IFA's earlier 2026 forecast called for franchise-sector output exceeding $920 billion this year, with increasing deal activity at both the platform and franchisee levels as cost structures ease and valuation gaps narrow. Restaurant Business Online's data showing corporate-operated chains outperforming franchised locations by 3x in median sales growth could suppress some franchise acquisition multiples in QSR, a segment worth watching for buyers and sellers alike. [Sources: | | https://www.restaurantbusinessonline.com/financing/market-franchising-disadvantage]

What to Watch Next

-

CFPB small-business data rule finalization — American Banker reports the rule is imminent. Once finalized, lenders will face a compliance clock; expect the effective date and implementation timeline to dominate small-business lending news in the next 30–60 days.

-

SBA contracting goal realignment — Federal News Network's reporting indicates the SBA is actively reshaping how veteran-owned and fraud-prone contracting programs are structured. Watch for formal rulemaking notices or policy guidance from SBA in late Q2 2026.

-

Restaurant franchise M&A multiples — With corporate-operated chains now demonstrably outperforming franchised locations on sales growth (per Restaurant Business Online), private equity buyers may begin pricing franchise platform acquisitions at a discount. Track deal flow in QSR and fast-casual for signals.

-

SBA Franchise Directory updates — Any brand not yet listed on the reinstated SBA Franchise Directory is effectively locked out of SBA 7(a) financing for franchisees. Brands seeking to grow through SBA-backed buyers should monitor directory update cycles and submit applications promptly.

Reader Action Items

-

Verify your target franchise brand is on the SBA Franchise Directory. Before committing to any franchise opportunity requiring SBA 7(a) financing, confirm the brand is listed at sba.gov. Brands delisted or not yet listed cannot access SBA-backed loans for franchisees.

-

Request the FDD and specifically read Items 7, 11, and 19. Item 7 covers initial investment ranges (including buildout costs), Item 11 covers franchisor obligations and field support, and Item 19 covers financial performance representations. These three items, cross-referenced with the 1851 Franchise buildout guide, will give you the most realistic opening timeline and cost picture.

-

Explore the multi-lender capital stack if a single lender has declined you. Lendzee's 2026 guide outlines how layering an SBA 7(a) primary with a soft-credit pre-approval and secondary lender can close financing gaps for deals in the $300K–$800K investment range. If you've been declined on a single-lender basis, this framework is worth a conversation with a franchise-focused finance broker.

-

Veterans: check SBA Patriot Express and OVBD programs before signing anything. Rafael Valle's success as a Lawn Doctor franchisee was partly enabled by veteran-friendly financing. The SBA's Office of Veterans Business Development offers specific loan advantages for veteran franchise buyers — confirm eligibility before selecting a lender or capital structure.

-

Monitor the CFPB data rule for lender compliance shifts. If you are a small-business borrower (especially minority- or women-owned), the pending demographic-data collection rule may change how lenders ask questions and document your application. Familiarize yourself with the rule's intent so you can advocate for equitable treatment during the loan process.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by