Venture Capital Pulse — 2026-04-20

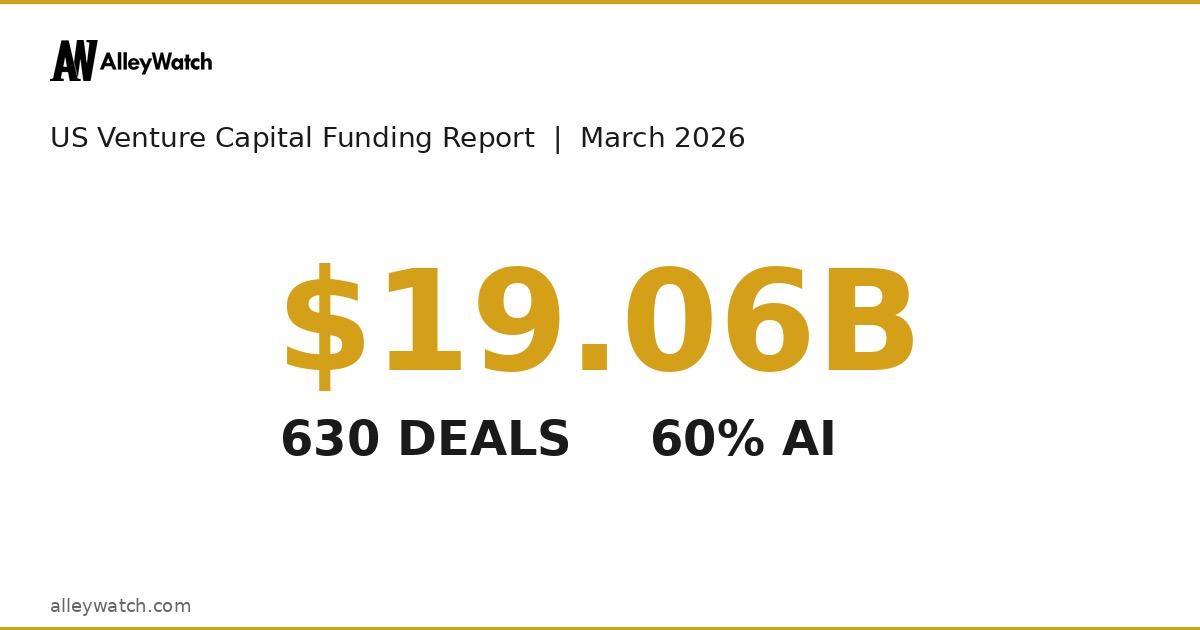

This week's VC landscape continues to be defined by AI concentration, with March 2026 data showing AI companies capturing 60.1% of all US venture capital ($11.46B across 316 deals out of a total $19.06B). The standout deals remain defense-AI and autonomous systems, led by Shield AI's $2.0B raise and Saronic's $1.75B. The dominant sector trend is a clear pivot from frontier model funding toward applied AI deployment in defense, autonomous systems, and life sciences.

Venture Capital Pulse — 2026-04-20

Top Deals This Week

Shield AI — $2.0B (Series-stage)

- Sector: Defense AI / Autonomous Systems

- Lead investor(s): Undisclosed

- What they do: AI-powered autonomy software for military aircraft and unmanned systems

- Why it matters: One of the largest defense-tech rounds ever closed, signaling that sovereign AI infrastructure spending is accelerating beyond the commercial sector. Shield AI's raise reflects growing institutional appetite for dual-use AI platforms amid geopolitical tensions.

Saronic — $1.75B (Series-stage)

- Sector: Defense Tech / Autonomous Maritime

- Lead investor(s): Undisclosed

- What they do: Autonomous surface vessels for naval and defense applications

- Why it matters: Saronic's round is among the largest ever for maritime defense tech. Combined with Shield AI's close, the week underscores that autonomous systems — not just generative AI software — are now commanding mega-round valuations.

Mind Robotics — $500M (Series-stage)

- Sector: AI Robotics

- Lead investor(s): Undisclosed

- What they do: AI-driven robotic systems for enterprise and defense environments

- Why it matters: The $500M raise for Mind Robotics signals that the next investment wave after large language models is embodied AI — physical robots that can reason and act in the real world. Investors are positioning early in what many see as the next $1T platform shift.

Cerebras — IPO Filing (S-1)

- Sector: AI Chips / Semiconductors

- Lead investor(s): N/A (public offering)

- What they do: Custom AI silicon (wafer-scale chips) designed as a direct Nvidia rival for AI training and inference

- Why it matters: Cerebras' S-1 filing — highlighted by PitchBook as the week's lead story — reveals significant UAE revenue concentration and special agreements with OpenAI, raising both strategic and geopolitical questions for prospective investors. This is one of the most closely watched AI chip IPOs in years.

- Valuation: Undisclosed (S-1 pending)

New Funds & LP Moves

-

African Fintech VC Recovery: PitchBook reported this week (April 16) that VC funding for African fintech "is back in business," suggesting renewed LP interest in emerging-market fintech after a multi-year pullback. No single fund size was disclosed, but the trend signals that frontier market allocators are returning to the continent's digital finance ecosystem as mobile money and embedded finance mature.

-

European VC Fundraising Recovery — Selective: According to PitchBook (April 15), European VC fundraising is recovering but access is narrowing sharply. Established managers are closing funds while newer or smaller GPs face a dramatically harder LP environment. The headline: "Not everyone is invited." This mirrors a broader global trend of LP concentration among brand-name managers.

-

UK Sovereign AI Fund Launch: The UK government launched a sovereign AI fund offering direct capital support to startups, per PitchBook (April 17). However, VCs surveyed expressed skepticism, noting that deeper structural problems — talent flight, regulatory friction, and thin late-stage capital — remain unresolved despite the government's intervention.

Exits & Acquisitions

-

Cerebras — S-1 Filed (IPO): AI chipmaker Cerebras filed its S-1 this week, positioning itself as a direct Nvidia rival with a wafer-scale architecture optimized for AI inference. Key revelations include disproportionate UAE revenue exposure and special commercial agreements with OpenAI. The filing is drawing intense scrutiny from analysts on both geopolitical and valuation grounds.

-

Biotech IPO Window Re-Opening — Selectively: PitchBook reported (April 15) that biotech IPOs are "poised for a comeback — but only for some." Clinical-stage companies with strong Phase 2/3 data and differentiated platforms are finding receptive public markets, while earlier-stage or single-asset biotechs remain locked out. The Fierce Biotech Fundraising Tracker (updated April 16) continues to log significant $50M+ VC rounds, including recent raises for Storm and Beeline (Bain-backed, $300M Series C).

Sector Spotlight

Defense AI & Autonomous Systems: The New Frontier Lab

March 2026 data from AlleyWatch confirms what many VCs have been telegraphing for months: capital is pivoting hard from frontier AI model labs toward applied, defense-adjacent autonomous systems.

Of the top US deals in March, two of the three largest were in defense tech — Shield AI ($2.0B) and Saronic ($1.75B) — compared to just one in more traditional enterprise AI (Mind Robotics, $500M). Total US VC in March reached $19.06B across 630 deals, with AI broadly capturing 60.1% of that volume.

This is a meaningful shift from Q1 2026's earlier weeks, which were dominated by foundation model mega-rounds (OpenAI, Anthropic, xAI). Now that the frontier model land-grab appears to be slowing, dollars are flowing downstream into companies that deploy AI in physical and defense contexts — drones, naval vessels, autonomous vehicles, and mission-critical battlefield software.

What this signals for founders and investors:

- Defense-AI companies with DoD contracts or adjacency are commanding valuation multiples previously reserved for frontier labs

- Autonomous systems are the "picks and shovels" play of the next AI cycle — less philosophical risk, clearer government procurement pathways

- Investors without cleared vehicles or national security expertise may find themselves locked out of the most competitive deals in this vertical

- The GPU access crunch (see: PitchBook's April 16 story on startups "auctioning GPU access like eBay") is creating new secondary market dynamics within the defense AI buildout

What to Watch Next Week

-

Cerebras IPO roadshow: With its S-1 now public, Cerebras is expected to begin investor meetings. Watch for price range disclosures and analyst commentary on the UAE revenue concentration risk — this could set the tone for the broader AI chip IPO pipeline.

-

OpenAI life sciences push: PitchBook (April 17) flagged that OpenAI's new life sciences model ("GPT Rosalind") is energizing life science VCs and could trigger a fresh wave of AI-biology startup formation and funding. Expect announcement activity from specialist bio-AI funds within the next 10 days.

-

SPAC market activity in quantum and AI infrastructure: PitchBook noted a cluster of SPAC mergers in quantum computing and AI infrastructure closing in early-to-mid April (story published April 10). Additional closings in this cluster may be announced in the coming week, offering an exit path for pre-revenue infrastructure plays.

-

UK VCT tax relief impact on deal flow: A cut to UK Venture Capital Trust tax relief took effect in early April (PitchBook, April 7). Observers are watching closely for signs of deal volume compression in the UK mid-market, which could accelerate founder migration to US or EU funding ecosystems.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by