Venture Capital Pulse — 2026-04-17

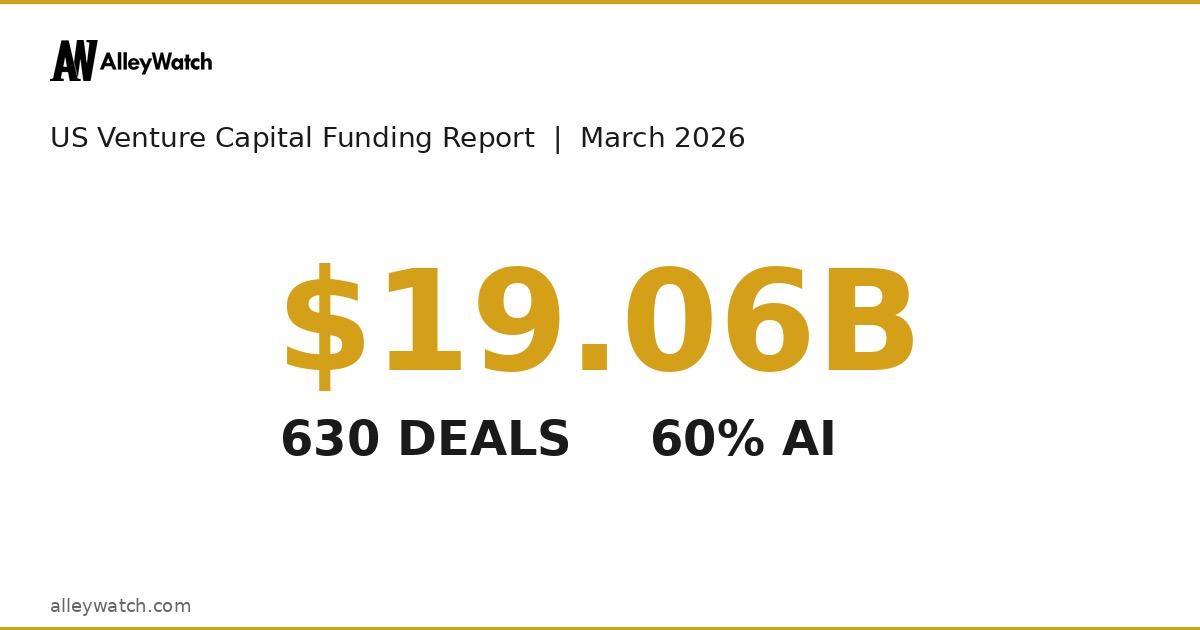

The week of April 10–17, 2026 continued to underscore a defining theme of the current VC era: capital is abundant but radically concentrated. US venture funding reached $19.06B across 630 deals in March alone, with AI companies capturing 60.1% of all dollars. Meanwhile, a cybersecurity startup raised $70M just six months after launch, Anthropic turned down new funding offers at an $800B+ valuation, and PitchBook's Q1 2026 Venture Monitor confirmed that 73.1% of all LP capital raised in Q1 went to just five VC firms.

Venture Capital Pulse — 2026-04-17

Top Deals This Week

Artemis — $70M Seed/Early-Stage

- Sector: Cybersecurity / AI-Driven Defense

- Lead investor(s): Not disclosed

- What they do: Israeli-founded platform targeting AI-driven cyberattacks with a new defensive security architecture

- Why it matters: Raising $70M just six months after launch signals extraordinary investor appetite for AI-native cybersecurity. As Anthropic's new Mythos model claims to detect threats that decades of researchers missed, the cybersecurity startup funding landscape is being reshaped — and valuations are under scrutiny

Shield AI — $2.0B (March 2026)

- Sector: Defense Tech / Autonomous Systems

- Lead investor(s): Not disclosed

- What they do: AI-powered autonomous defense systems for military applications

- Why it matters: One of three defense/autonomous systems giants that dominated March 2026 US VC, alongside Saronic ($1.75B) and Mind Robotics ($500M). The defense tech cluster accounted for a disproportionate share of AI dollars outside frontier models, signaling a sustained shift of VC attention toward dual-use and national security applications

Saronic — $1.75B (March 2026)

- Sector: Defense Tech / Autonomous Naval Systems

- Lead investor(s): Not disclosed

- What they do: Autonomous naval vessel technology for defense applications

- Why it matters: Part of the same defense-tech wave as Shield AI; Saronic's massive round reflects how autonomous systems are now a marquee VC category. Capital is clearly shifting from pure frontier AI model labs toward physical-world autonomy with defense applications

Spektr — $20M Series A

- Sector: Fintech / Regulatory Compliance

- Lead investor(s): NEA

- What they do: Copenhagen-based AI compliance platform that automates the manual drudgery of financial compliance workflows

- Why it matters: Repeat founders, NEA backing, and a focus on AI-native compliance automation make this an emblematic deal. While mega-rounds dominate headlines, this deal illustrates active Series A market in European fintech compliance — a sector seeing strong tailwinds from expanding regulatory requirements across the EU

news.crunchbase.com

news.crunchbase.com

news.crunchbase.com

news.crunchbase.com

Global Venture Funding In 2025 Surged As Startup Deals And Valuations Set All-Time Records

A Growing Share Of Seed And Series A Funding Is Going To Giant Rounds

The Week’s 10 Biggest Funding Rounds: World Labs Leads Another AI-Heavy Lineup

Gizmo — $22M Series A

- Sector: EdTech / AI Learning

- Lead investor(s): Not disclosed

- What they do: AI-powered learning platform with over 13 million users

- Why it matters: Gizmo's 13M-user base gives it distribution leverage that most EdTech startups lack when raising Series A. The deal is a data point for AI-native consumer education: capital is flowing to platforms demonstrating real retention and growth, not just AI wrappers on existing curricula

New Funds & LP Moves

-

VC Concentration at the Top: Per the Q1 2026 PitchBook-NVCA Venture Monitor, 73.1% of all LP capital raised in Q1 2026 went to just five venture firms. This marks an extreme bifurcation in fund-raising power, where brand-name multi-stage funds command the lion's share of institutional LP commitments while smaller and emerging managers face a structurally tougher environment. The trend reinforces what Axios described as a shift "from underdogs and moonshots" to "front-running" — where the biggest VCs back the most already-proven companies.

-

European VC Fundraising Recovery — Selective: PitchBook analysis published April 15 shows European VC fundraising is recovering after years of weakness, but access is narrowing. LP capital is concentrating in top-tier European managers, leaving mid-market and emerging fund managers behind. France-based LP secondaries activity is also increasing as a liquidity mechanism amid the still-constrained IPO window.

Exits & Acquisitions

-

Biotech IPO Comeback — Selective: A PitchBook analysis published April 15 reports that biotech IPOs are poised for a comeback in 2026, but only for a narrow category of companies — those with late-stage clinical assets and clear near-term catalysts. The broader biotech IPO window remains largely shut for earlier-stage or platform-only companies. This mirrors a broader pattern in which public markets are selectively reopening for VC-backed companies with proven revenue or imminent catalysts, while the IPO drought continues for most.

-

Private Market Secondaries Hit Record $226B in 2025: Secondary transaction volumes in private markets reached $226 billion last year — up 41% from 2024 — as US investors turn to secondaries for portfolio liquidity during the ongoing IPO slowdown. This trend is continuing into 2026, with secondaries increasingly functioning as the primary liquidity mechanism for VC LPs in an environment where traditional exits remain constrained.

Sector Spotlight: Defense Tech & AI — The New Venture Duopoly

The March 2026 US VC data crystallizes a story building all year: AI and defense tech have become the twin poles of venture capital, with everything else fighting for the remainder.

AI companies raised $11.46B across 316 deals in March 2026, capturing 60.1% of all US venture capital for the month. But the composition has shifted meaningfully. As Crunchbase's "capital concentrated at the top" analysis published April 16 notes, capital is moving from frontier AI model labs toward applied and physical AI — particularly defense, autonomous systems, and robotics.

The March data tells the story precisely:

- Shield AI: $2.0B

- Saronic: $1.75B

- Mind Robotics: $500M

These three deals alone — all in defense/autonomous systems — account for over $4.25B in a single month.

What this signals for founders and investors: The barbell is becoming more pronounced. Mega-rounds continue flowing to established AI names (Anthropic, OpenAI) and to defense/dual-use autonomy. Mid-market AI infrastructure and pure software plays face growing pressure to show enterprise traction quickly. Founders outside AI or defense are increasingly competing for a shrinking proportional share of overall dollars, even as absolute dollar volumes remain elevated.

The Crunchbase Q1 2026 analysis notes that while global startup deal count has fallen, dollar volumes are at all-time highs — driven almost entirely by a handful of US-based AI companies.

news.crunchbase.com

alleywatch.com

news.crunchbase.com

news.crunchbase.com

alleywatch.com

news.crunchbase.com

Global Venture Funding In 2025 Surged As Startup Deals And Valuations Set All-Time Records

A Growing Share Of Seed And Series A Funding Is Going To Giant Rounds

The Week’s 10 Biggest Funding Rounds: World Labs Leads Another AI-Heavy Lineup

What to Watch Next Week

-

Anthropic's Next Fundraise: Anthropic has reportedly turned down VC funding offers that would value it at $800B+, choosing to wait rather than accept dilution at peak froth. Watch for any announcement of a formal fundraising process — when it comes, it is expected to be one of the largest private funding rounds in history and will set a new benchmark for AI valuations.

-

PitchBook-NVCA Q1 2026 Venture Monitor Digestion: The full Q1 2026 Venture Monitor (released April 14) is still being absorbed by the industry. Expect follow-on analysis and LP/founder reactions through next week — particularly around the 73.1% concentration figure and what it means for emerging fund managers.

-

European VC Tax Policy Shifts: The UK's VCT (Venture Capital Trust) tax relief cut took effect this month, with PitchBook reporting April 7 that UK startup funding has already been hit. Watch for data on whether UK deal flow softens further in April reporting and whether founders accelerate moves toward continental Europe or US incorporation.

-

Defense Tech IPO Pipeline: PitchBook's April 10 analysis flagged that SpaceX isn't the only defense tech IPO VCs should watch. With defense and dual-use companies now commanding massive private rounds, pressure to deliver IPO exits is building. Any defense tech filing or S-1 announcement would be closely watched as a barometer for whether this category can generate public market liquidity.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by