Samsung Electronics 주가 및 시장 동향 — 2026-05-14

On May 14, 2026, Samsung Electronics (005930) closed at 296,000 KRW, up 12,000 KRW (+4.23%), sitting just 500 KRW shy of the 300,000 KRW milestone. Global investment banks like JPMorgan and Citigroup have raised target prices to the 400,000–500,000 KRW range, citing massive AI memory demand and the resumption of the DS division’s next-gen semiconductor programs. Investors should keep a close eye on the potential labor strike scheduled for May 21 and the HBM4 mass production timeline.

Samsung Electronics 주가 및 시장 동향 — 2026-05-14

오늘의 핵심 지표

| 지표 | 값 | 비고 |

|---|---|---|

| 종가 (KRW) | 296,000 | +12,000 (+4.23%) |

| 거래량 | — | 다음 포털에서 확인 권장 |

| 시가총액 | — | KOSPI 비중 — |

| 52주 최고/최저 | — / — | — |

| PER / PBR | — / — | — |

| 외국인 보유율 | — | 전일 대비 — |

⚠️ Screen capture limitations: Please check major portals directly for data on trading volume, market cap, and foreign ownership.

수급 동향

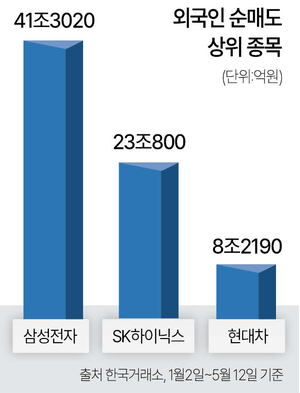

- Foreign investors' net selling at 41 trillion KRW: According to Herald Business, foreign investors have been the biggest sellers of Samsung Electronics among all KOSPI-listed stocks in 2026, with annual net selling reaching 41 trillion KRW.

- 14 trillion KRW sold in May alone: Despite the KOSPI’s rally toward the 8,000 level, foreign investors have net-sold approximately 14 trillion KRW in the broader KOSPI market this month, with heavy focus on large-cap semiconductor stocks like Samsung Electronics and SK Hynix.

- Labor risks as a variable: Despite the bull market, the potential for a total semiconductor strike due to stalled labor negotiations is weighing on foreign investor sentiment, as reported by Herald Business.

주요 뉴스 및 촉매

JP모간 "조정 시 사라"…'30만전자' 고지 500원 앞으로

Global IB firms including JPMorgan and Citigroup, along with domestic securities firms, have issued a series of buy ratings with target prices reaching 400,000 to 500,000 KRW. As of 10:49 AM, Samsung Electronics was trading at 296,000 KRW, a 4.23% increase, putting the "300,000-won" threshold within reach.

삼성 DS사업부, 차세대 반도체 사업 재개

According to TechTimes, Samsung's DS (Device Solutions) division has wrapped up its one-year emergency normalization period and is restarting investments in next-gen NAND flash, compound semiconductors, and advanced packaging. However, an 18-day strike potentially starting May 21 remains a key variable.

삼성·SK하이닉스 AI 메모리 수요 폭증, 증설 경쟁 가속

Samsung Electronics and SK Hynix are engaged in unprecedented expansion efforts to meet the surge in AI memory demand. Digitimes reports that both firms are accelerating capacity expansion for HBM (High Bandwidth Memory) and DRAM.

반도체 업황 및 경쟁사 비교

The surge in memory demand driven by the AI inference boom is creating exceptionally strong conditions for both Samsung Electronics and SK Hynix. Digitimes notes that margins for certain DDR5 products have improved, and next-gen HBM has emerged as the central battleground for 2026. While Samsung is developing technology to integrate NAND-style logic circuits under memory arrays for next-gen DRAM, SK Hynix is leveraging vertical stacking to gain an edge. HBM shortages are straining the entire chip supply chain, with clients pre-ordering capacity years in advance. CNBC reported that TSMC, Samsung, and SK Hynix are locked in intense regional competition for AI chip supremacy, while also flagging risks associated with market reliance on a small number of AI-linked semiconductor giants.

글로벌 시각

CNBC highlighted that Samsung Electronics has surpassed a 1 trillion USD market cap, with shares rising over 15% on the back of the AI craze, fueled directly by an 8-fold increase in Q1 operating profit. Both CNBC and Digitimes warned that supply shortages could persist beyond 2027 despite the current capacity expansion. Furthermore, the upcoming launch of 2x leveraged DRAM ETFs in the U.S. that include Samsung and SK Hynix reflects growing global interest in South Korean semiconductors.

투자자가 주목할 포인트

- Short-term (1 week): Monitor the labor union strike scheduled for May 21 and its impact on DS division production. Watch for the psychological "300,000-won" breakthrough.

- Mid-term (Q1): HBM4 mass production timeline and qualification for NVIDIA supply. Look for price inflection points in DRAM/HBM due to AI demand, and the visibility of new growth engines from resumed R&D in NAND and compound semiconductors.

- Risk factors: ① Labor risks: Potential production disruptions if the strike occurs. ② Foreign supply burden: Sustained selling pressure (41 trillion KRW annual scale) could sap upward momentum. ③ Concentration risk: Potential for increased volatility as KOSPI and Taiwan markets remain highly dependent on a few AI semiconductor stocks.

독자 액션 아이템

- Monitor the May 21 Samsung Electronics labor strike: Keep an eye on breaking news and KRX filings to assess potential production disruptions.

- Track daily foreign net buying/selling on KRX: The key to the mid-term trend is whether the 41 trillion KRW annual selling trend continues or reverses. Data available at krx.co.kr.

- Cross-reference with SK Hynix’s earnings and HBM output: SK Hynix's HBM4 progress and NVIDIA supply status are vital benchmarks for evaluating Samsung's competitive position. Regularly check the semiconductor sections on Digitimes and CNBC.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by