Korean Market Briefing: KOSPI Reclaims 8,100, 외국인 귀환

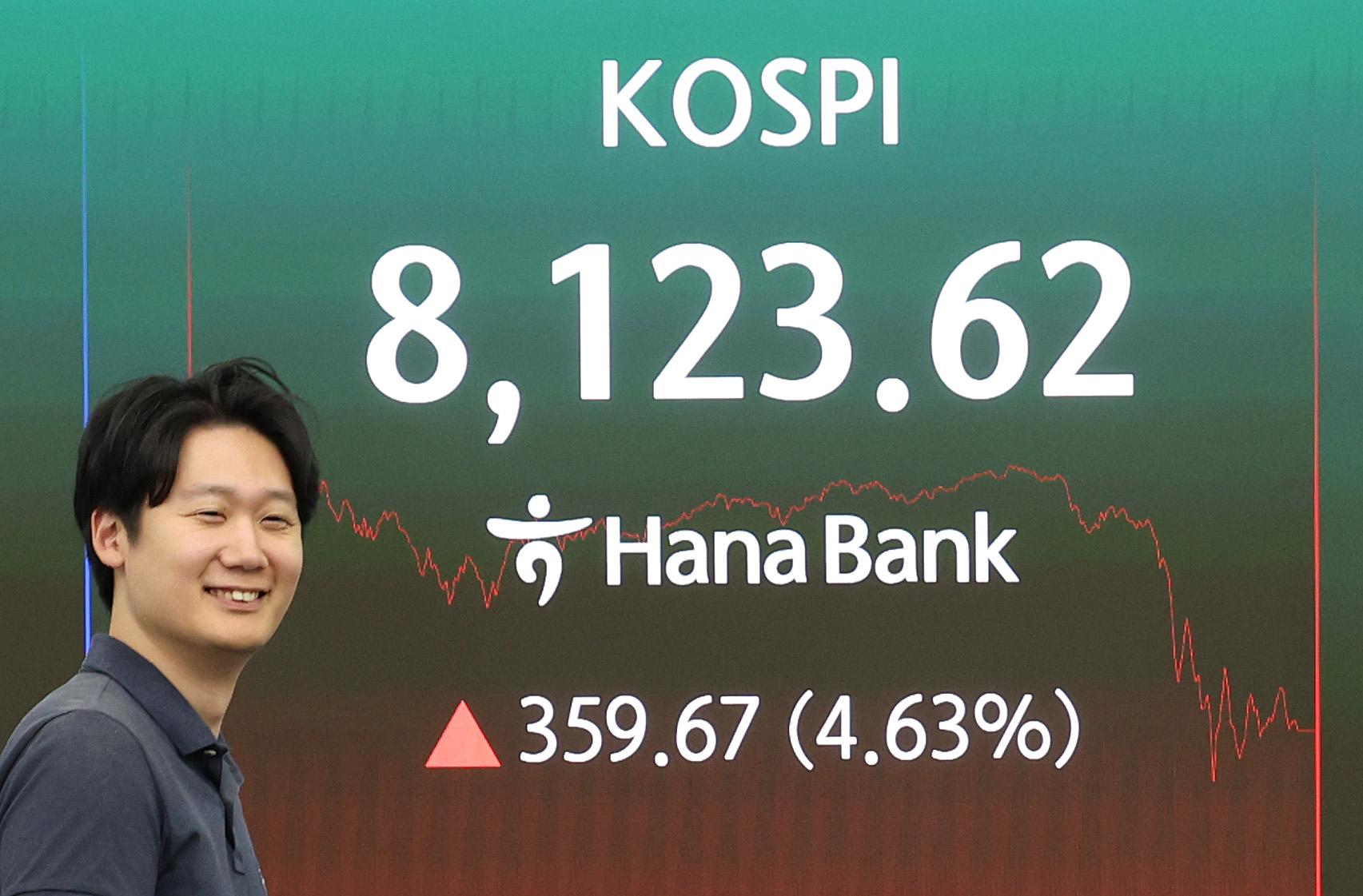

On Friday, June 13, the KOSPI closed at 8,123.62 (+4.63%), while the KOSDAQ rose to 996.93 (+4.76%). Foreign investors returned with a net buy of 2.1 trillion KRW for the first time in 25 trading sessions, driven by easing Middle East tensions and renewed optimism for AI and semiconductor stocks.

Korean Market Briefing — 2026-06-14

Current Index Status

| Index | Closing Price | Daily Change | Change (%) | Note |

|---|---|---|---|---|

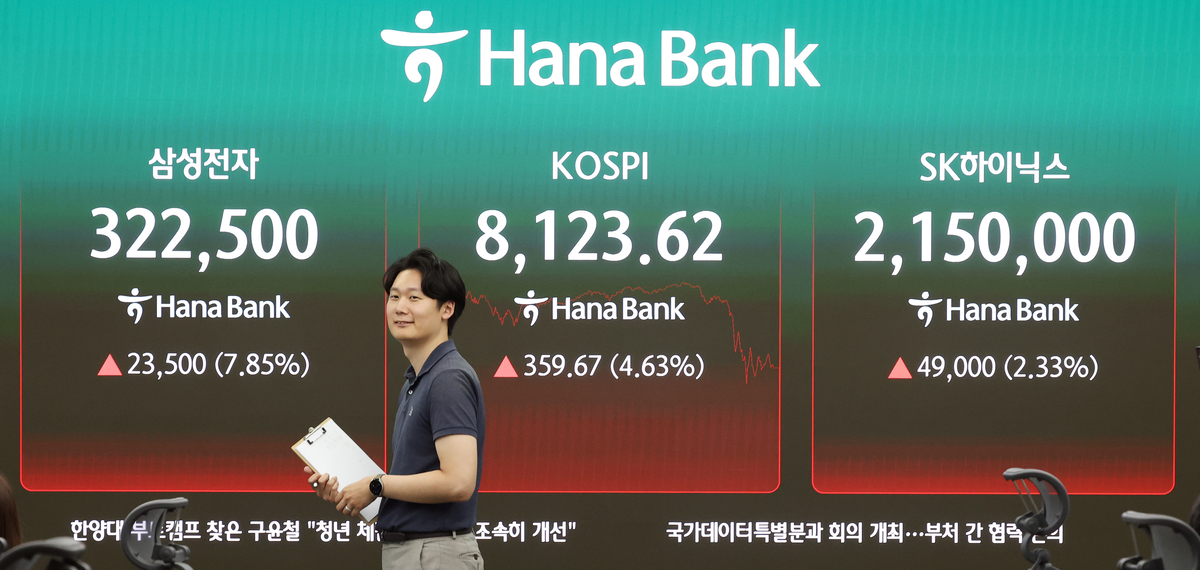

| KOSPI | 8,123.62 | +372.69 | +4.63% | Easing Middle East risk, AI tech rally |

| KOSDAQ | 996.93 | +45.3 | +4.76% | Mid-cap and growth stocks surge |

The KOSPI reclaimed the 8,100 level, ending up 4.63% after hitting an intraday high of 8.6%. The shift from net selling to net buying by foreign investors—breaking a 25-session streak—served as the primary trigger for improved market sentiment. Factors included reduced geopolitical tension in the Middle East and signs of recovering AI demand.

Market Inflow by Investor Type

- Foreigners: Returned as net buyers with 2.1 trillion KRW, marking the first move in 25 sessions. Focused on semiconductors (SK Hynix, Samsung Electronics) and AI-related tech stocks. Driven by stabilized U.S. employment data and easing concerns over Fed interest rate hikes.

- Institutions: Specific volume not disclosed, but observed moving in tandem with foreigners to accumulate tech stocks.

- Individuals: Active trading in small-cap stocks within leading sectors due to recovering sentiment.

Top Movers

Top 3 Gainers

SK Hynix – Continued strength fueled by signs of a semiconductor cycle recovery and foreign buying, reflecting investor expectations for rising AI chip demand.

Samsung Electronics – Rose alongside its peers due to news of memory chip price stabilization and expanded foundry orders. Led the market as a preferred blue-chip stock for foreign investors.

General Tech Stocks – Shared the rally with global partners like Kioxia; domestic AI-related material and equipment companies also saw synchronized gains.

Decliners

While no specific top decliners or percentage drops were highlighted, defensive sectors like financial services (Samsung Life Insurance -0.82%) and energy (LG Energy Solution -0.26%) showed relative weakness.

Sector Trends

Strong Sectors: Semiconductors (+), IT/Telecom (+) – Expected recovery in AI chip demand and global economic cycle improvements. Memory price hikes supported major industry players.

Weak Sectors: Finance (±0%), Energy (slight -) – Lagged despite reduced interest rate hike concerns, as they are classified as defensive assets.

Key Issues & Drivers

1. Foreigners Return After 25 Days

- Details: Foreign investors, who were net sellers for 25 sessions, returned to net buying (2.1 trillion KRW) on Friday (June 13).

- Market Impact: KOSPI reclaimed 8,100; a signal of psychological recovery. Future foreign inflow will be crucial for the KOSPI trend.

2. Semiconductor and AI Tech Strength

- Details: SK Hynix, Samsung Electronics, and partners like Kioxia rallied together on AI chip demand and memory price stabilization.

- Market Impact: Tech stocks served as the main driver, widening the performance gap between them and smaller, non-tech stocks.

3. Easing Middle East Geopolitical Tensions

- Details: Reduced risk in the Middle East lowered the preference for safe-haven assets, prompting capital to flow back into riskier Korean tech stocks.

- Market Impact: KOSPI volatility cooled; shifted to a potential rotation market environment.

Macro & External Variables

KRW/USD Rate: While specific figures were not reported, the resolution of Fed hike concerns likely led to a weaker dollar/stronger won, improving the export competitiveness of Korean tech firms.

U.S. Interest Rates/Fed: Although initial strong employment data raised fears of hikes, the spot market shifted toward hopes for easing.

Global Tech Cycle: Simultaneous gains across the Asian semiconductor supply chain, including Japan (Nikkei 225), Korea (KOSPI), and Taiwan.

Tomorrow’s Checkpoints

- Earnings Announcements: Monitor the start of the Q2 earnings season (focus on semiconductors/IT).

- Fed Communications: Watch for any mention of further interest rate hikes.

- Currency Volatility: Keep an eye on support/resistance levels near 1,300 KRW/USD.

- Middle East Situation: Monitor for any escalation between Iran and Israel.

Investor Guidance

- Short-term: Focus on the continuity of foreign net buying. Tech stock concentration carries volatility risks; consider profit-taking.

- Mid-to-long term: Semiconductors and AI are in the early stages of recovery, favoring cyclical sectors, but watch for signs of valuation overheating.

- Risks: Potential geopolitical flare-ups in the Middle East, a resurgence of Fed hawkishness, and oversupply concerns for memory chips.

Expert Comments

"The surprise in U.S. employment data triggered a rise in bond yields, providing an excuse for correction pressure that had accumulated in the overheated market due to the surge in semiconductor stocks." – Kiwoom Securities analyst Han Ji-young

"The Korean stock market remains undervalued compared to historical valuations (about 9x based on EPS) and is attractive in terms of corporate earnings and government policy support." – Mirae Asset Securities analyst Seo Sang-young

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by