Market Strategy: KOSPI 8,000 Milestone Guide — 2026-05-25

As of Sunday, May 25, 2026, U.S. markets (NYSE/Nasdaq) are closed for Memorial Day, and South Korean markets are closed for the weekend. Market participants are focused on whether the KOSPI can cement its position at the 8,000 line when trading resumes on Tuesday, May 26. Key variables to watch include the reopening of U.S. markets, progress on Iran negotiations, and updates on the National Growth Fund.

Market Strategy: Watchlist & Trading Guide — 2026-05-25

Editor's Note: Sunday, May 25, 2026, is a non-trading day for both domestic and international markets (Memorial Day in the U.S. and the weekend in Korea). This content is based on verified public sources as of May 24, 2026, and does not include real-time closing data for today.

Market Snapshot (As of the last trading day: 2026-05-23)

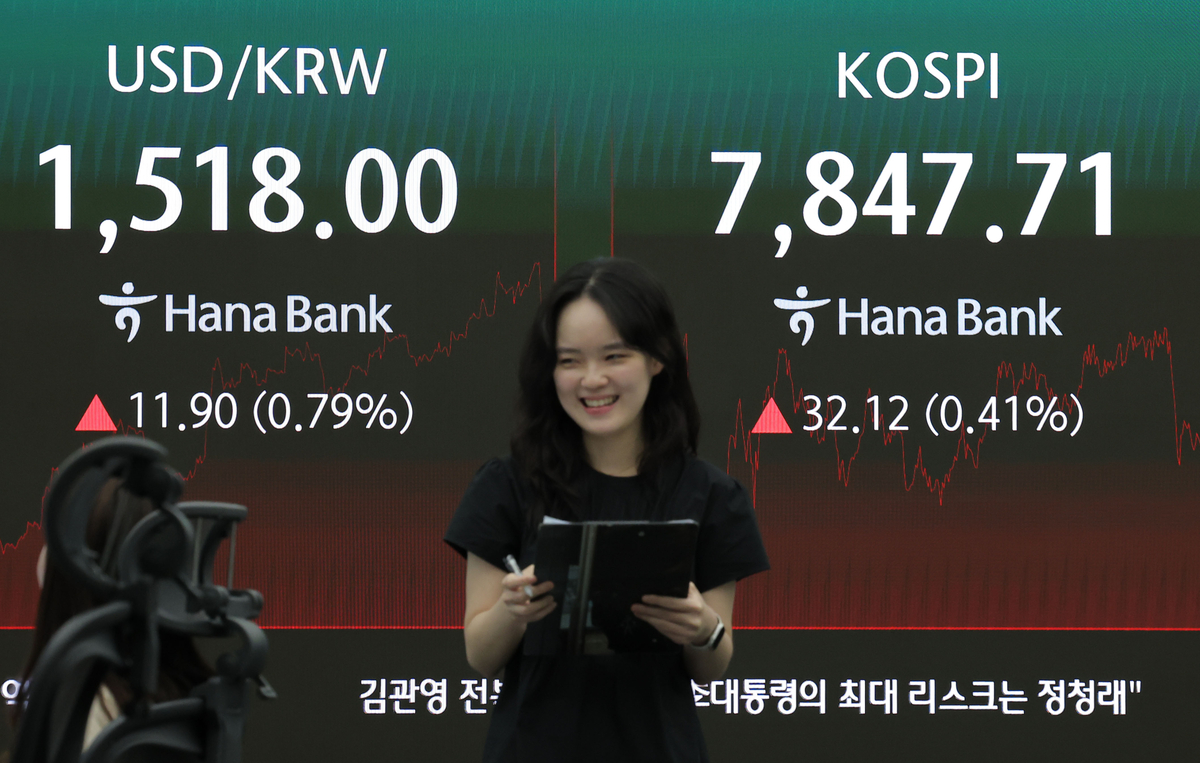

- KOSPI: Attempting to settle above the 8,000 mark (brokerage weekly forecast).

- KOSDAQ: Around 1,161 (exploring adjustments after a +4.99% surge on May 22).

- Supply & Demand: Foreigners recorded a cumulative net sell-off of 45.9 trillion KRW over 12 sessions; ETFs and pension funds are defending the index.

- Exchange Rates/Bonds: Volatility in FX and bond yields persists; specific figures require confirmation on May 26.

- Trading Volume: No new data available since May 23.

Global Context — U.S. Market (Note: Memorial Day Closure)

-

Holiday Notice: Monday, May 25, 2026 (U.S. time), is Memorial Day; both the NYSE and Nasdaq are closed. U.S. trading resumes Tuesday, May 26. Korean market participants should refer to the May 23 (Friday) U.S. closing data for Tuesday's opening.

-

Recent U.S. Market Trend: The Dow Jones reached a new closing high on May 23 (Friday) with a gain of about 300 points, and the S&P 500 closed higher for eight consecutive weeks. Volatility increased due to surging Treasury yields and oil price fluctuations.

-

Key Issues — Iran Negotiations & Treasury Yields: Expectations for U.S.-Iran ceasefire negotiations provided momentum, though rising 10-year Treasury yields (hitting highs for the year) capped the upside. Oil prices dropped significantly following news of the negotiations.

-

Kevin Warsh's Inauguration: With new Federal Reserve Chair Kevin Warsh set to take the oath of office, the market remains cautious regarding potential adjustments to interest rate policies.

Leading Sectors & Themes (Based on recent trading)

1st Priority: Semiconductors (Samsung Electronics, SK hynix)

- Trend: Brokerages have collectively raised target prices, highlighting this as a core sector.

- Key Stocks:

- Samsung Electronics (005930): Brokerage targets range from 430,000 to 500,000 KRW; Nomura suggests up to 590,000 KRW.

- SK hynix (000660): Brokerage targets range from 2.75 million to 3.1 million KRW; Nomura raised it to 4 million KRW.

- Checkpoints: The HBM (High Bandwidth Memory) price increase is the core trigger. Nomura projects SK hynix’s HBM ASP per GB will surge from approx. $12.90 in 2026 to $20.90 in 2027. Some brokerages warn of a potential slowdown in momentum.

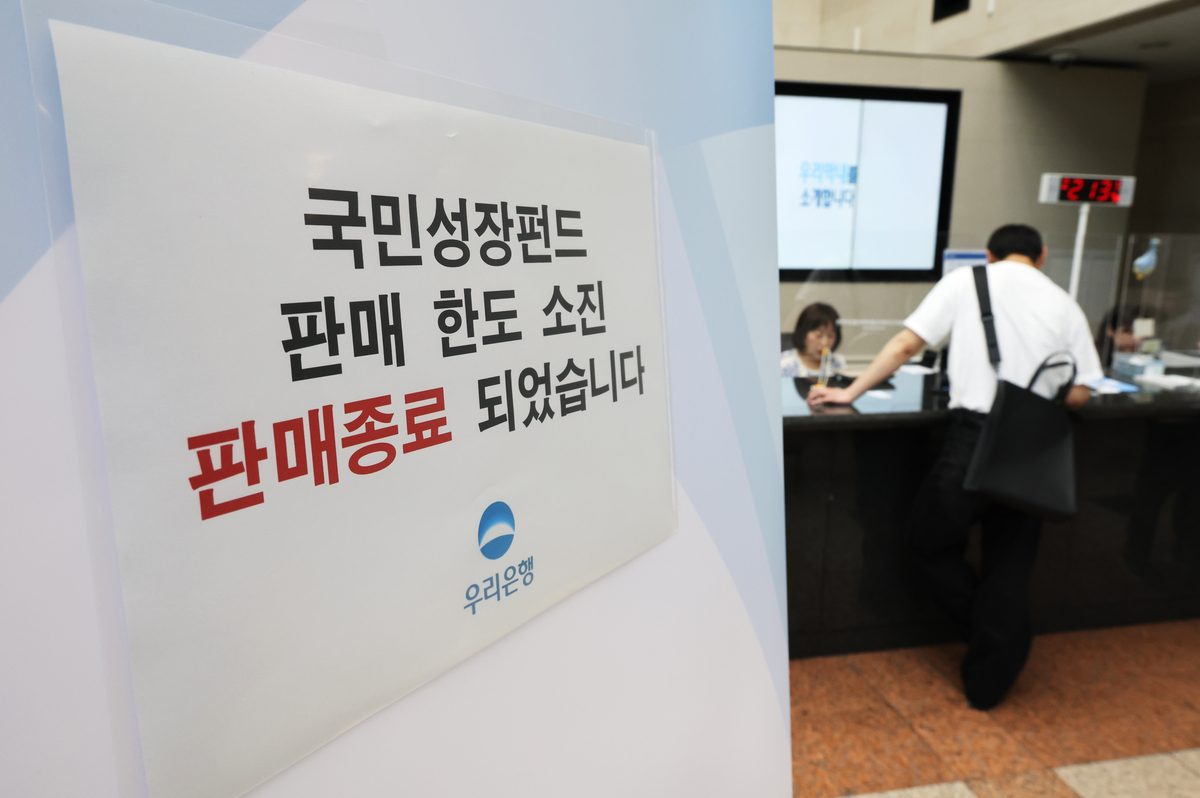

2nd Priority: National Growth Fund beneficiaries (KOSDAQ)

- Trend: On May 22, the KOSDAQ surged +4.99% to 1,161.13 amid expectations that 45 trillion KRW of the government's 150 trillion KRW National Growth Fund will be funneled into KOSDAQ high-tech sectors.

- Key Stocks: Small-to-mid-cap advanced tech stocks on the KOSDAQ.

- Checkpoints: Timing and scale of fund execution are key to sustained growth.

3rd Priority: Value-Up & Corporate Governance

- Trend: The Value-Up program and structural reforms are credited with fueling the current KOSPI rally.

- Key Stocks: Large-cap blue chips (holding companies, finance, dividend growth stocks).

Trading Guide

Prices are for reference only and are based on brokerage reports and disclosures. Investment decisions are at your own risk.

Samsung Electronics (005930)

- Trading Note: Non-trading day; refer to May 23 closing price.

- Supply & Demand: Sustained foreign net selling, defended by pension fund/ETF buying.

- Fundamental Triggers: Surge in HBM demand and AI investment cycles.

- Brokerage Targets: 430,000 – 590,000 KRW.

- Risk Factors: Extended foreign net selling or geopolitical risks from Iran negotiations.

- Scenario: Monitor 400,000 KRW support levels; watch for a break below 380,000 KRW.

SK hynix (000660)

- Trading Note: Non-trading day; refer to May 23 closing price.

- Fundamental Triggers: AI investment is seen as a "survival issue," keeping demand robust.

- Brokerage Targets: 2.75 – 4 million KRW.

- Risk Factors: HBM price erosion or tighter U.S. export regulations.

- Scenario: 3 million KRW is the key resistance-turned-support line; watch for a break below 2.6 million KRW.

KOSDAQ Advanced Tech (National Growth Fund basket)

- Trading Note: KOSDAQ index closed at 1,161.13 on May 22.

- Fundamental Triggers: Large-scale inflow of government policy funds.

- Scenario: Observe support at 1,150; watch 1,100 for short-term signs of cooling.

Must-Watch Events

- 🇺🇸 U.S. Market Reopening (2026-05-26, Tue, 09:30 AM EST / 10:30 PM KST): Resumption after Memorial Day.

- 🇰🇷 KOSPI 8,000 Threshold (2026-05-26, Tue, 09:00 AM KST): Foreign net buying and ETF inflows are critical.

- 🇰🇷 National Growth Fund Updates: Potential for more specific details on funding allocations this week.

- 🌏 Iran Negotiations: Impact on oil prices and global risk-on sentiment.

- 🇺🇸 Kevin Warsh Speech: Any initial remarks on monetary policy.

Brief Strategy

The market opening on Tuesday, May 26, is the turning point for the week. If foreign selling eases and U.S. Treasury yields stabilize, a risk-on stance toward semiconductors and KOSDAQ growth stocks is appropriate. Conversely, if Iran negotiations stall or Fed Chair Warsh sounds hawkish, be prepared to reduce positions and move to the sidelines.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by