Forex & Currency Watch — 2026-05-12

The U.S. Dollar Index (DXY) is holding firm near the 97.90–97.95 region, consolidating after months of broad weakness, as investors adopt a cautious stance ahead of Tuesday's key U.S. CPI release and monitor escalating Middle East tensions. The single biggest mover among majors is the Hungarian forint (USD/HUF), which surged -1.52% on the day and is down over 16% year-on-year, reflecting acute Central European risk-off dynamics. The primary macro catalyst driving the tape is a combination of geopolitical tension in the Middle East — with Trump rejecting Iran's response to a peace proposal — and anticipation of the U.S. CPI print, which will shape near-term Fed policy expectations.

Forex & Currency Watch — 2026-05-12

Market Snapshot

| Pair | Level | Daily % | Weekly % |

|---|---|---|---|

| DXY | 97.900 | -0.17% | -0.26% |

| EUR/USD | 1.1786 | +0.51% | +0.56% |

| USD/JPY | 157.04 | +0.24% | -0.11% |

| GBP/USD | 1.3628 | -0.04% | +0.69% |

| USD/CHF | 0.7776 | +0.14% | -0.78% |

| AUD/USD | 0.7256 | +0.12% | +1.17% |

| USD/CNY | 6.7970 | -0.17% | -0.49% |

Note: TradingEconomics data as of May/08 close; Investing.com intraday levels updated May 11 at ~13:21 GMT. Daily % from Investing.com real-time feed.

Top Movers

Winners and Losers — Past 24 Hours

-

USD/HUF → USD strengthening vs. HUF (-1.52% daily; -16.57% YoY): The Hungarian forint remains one of the steepest losers in the G20 FX space, dragged by Central European risk aversion and a widening rate-differential narrative as the ECB/Fed policy paths diverge.

-

USD/NOK → NOK outperforming (-1.06% daily; -11.17% YoY): The Norwegian krone is among the session's strongest gainers against the dollar, supported by firmer oil prices which remain elevated amid Middle East geopolitical risk.

-

USD/MXN → Peso outperforming (-0.75% daily; -11.65% YoY): The Mexican peso extended its strong year-to-date gains, benefiting from carry-trade flows and resilient domestic fundamentals; down over 4.6% on the month alone.

-

USD/CNY (loser side of dollar): At 6.7970, the yuan is firmer vs. the dollar (-0.17% daily, -2.57% YTD) as PBOC guidance keeps the fix anchored and BofA analysts flag potential for "mild yuan strength" following geopolitical engagements between Washington and Beijing.

-

GBP/USD (laggard): Sterling edged lower intraday (-0.04%) as the Middle East impasse weighed on risk sentiment; markets now focus on Tuesday's U.K. CPI as the next near-term catalyst.

What Moved the Tape

-

Middle East tensions cap risk appetite: Breaking news that President Trump rejected Iran's response to a peace proposal kept safe-haven demand simmering. USD/JPY bounced to 157.04 (up ~0.24%) as haven flows partially offset yen strength; GBP/USD was knocked back from session highs as sterling absorbed geopolitical risk-off selling. Oil prices firming on the back of the standoff supported commodity-linked currencies like NOK and CAD.

-

US CPI countdown pins the dollar: The DXY is "coiling in a tight range" near 97.95 as markets wait for Tuesday's U.S. CPI print, per a May 11, 2026 FXStreet analysis. The dollar neither rallied nor sold off materially overnight, with investors unwilling to take large directional bets ahead of the data. The FXStreet note highlights that "rising Middle East tensions and oil prices continue supporting" a cautious tone, while CPI outcomes could decisively break the range.

-

BofA flags mild yuan appreciation post Trump-Xi summit: Investing.com reported May 11 that Bank of America analysts see scope for mild USD/CNY downside following a Trump-Xi Beijing summit, a signal that currency diplomacy is a live factor. USD/CNY traded around 6.7970, near multi-month yuan highs.

Central Bank Watch

-

Federal Reserve: The Fed is firmly on hold, but Tuesday's CPI data is a crucial input. Markets are watching for any sign of renewed inflation that could push back already-delayed rate-cut expectations. The DXY's continued consolidation near 97.90 reflects that traders see the Fed as the dominant swing factor this week.

-

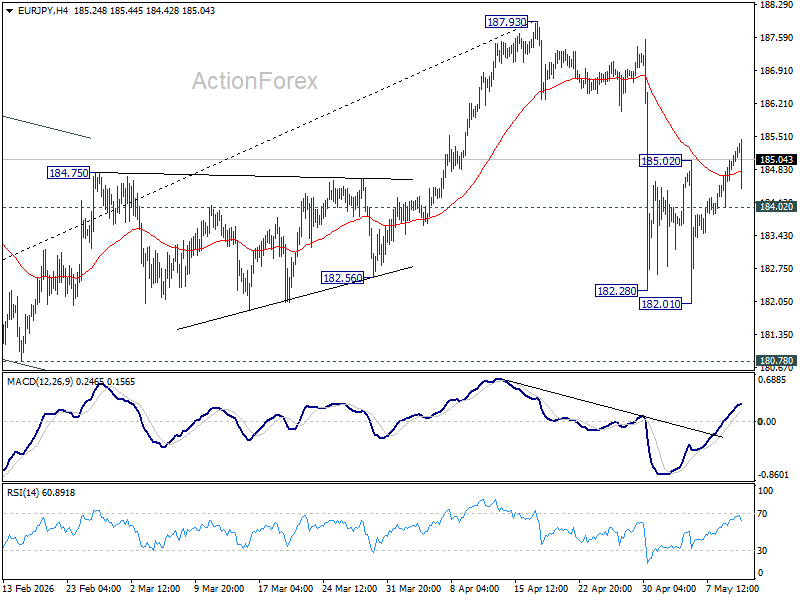

Bank of Japan (BOJ): USD/JPY remains elevated near 157 and is back inside the "MoF intervention zone" flagged in recent weeks by analysts at forex.com. Japan's Ministry of Finance stepped into the FX market as recently as April 30, 2026 (Reuters) to support the yen near multi-year lows. With USD/JPY bouncing +0.24% intraday to 157.04, the intervention risk is elevated. EUR/JPY technical outlook (ActionForex, May 12, 2026) places key support at 184.02 and sees a possible retest of the 187.93 high.

-

People's Bank of China (PBOC): The yuan continues to firm, with USD/CNY at 6.7970 (-0.17% daily; -6.13% YoY). BofA strategists cited by Investing.com (May 11, 2026) see further mild yuan appreciation as the base case post-Washington-Beijing diplomatic engagement. The PBOC is expected to keep its daily fixing anchored supportively.

-

Bank of England: GBP/USD slipped marginally intraday to 1.3628. Markets await the U.K. CPI release on Tuesday as the primary determinant of the BOE's next move. Sterling's YTD performance (+1.12%) remains healthy, but the Middle East risk backdrop has capped upside for now, per Investing.com's May 11 sterling note.

Emerging Markets & Asia FX

-

USD/CNY — 6.7970 (-0.17% daily): The Chinese yuan is on firm footing, down 2.57% YTD vs. the dollar and 6.13% year-on-year, marking a material yuan appreciation. BofA flagged "mild yuan strength" as the base case following high-level U.S.-China diplomatic contacts; PBOC daily fixings continue to guide USD/CNY lower in a controlled fashion.

-

USD/KRW — 1,461.91 (+0.22% daily): The South Korean won gave back some recent gains against the dollar, rising slightly. However, UBS analysts are bullish on the won medium-term, citing favorable balance of payments flows, per an Investing.com note published May 11, 2026. The pair is down 0.63% on the week and the won's YTD move is still a 1.48% decline vs. the dollar (i.e., won weaker YTD).

-

USD/MXN — 17.1797 (-0.75% daily): The peso continued its impressive rally, now down 11.65% year-on-year vs. the dollar (peso has strengthened markedly). The pair shed another 1.57% on the week, reflecting strong carry demand and positive domestic fundamentals. USD/MXN is near multi-year lows for the dollar-peso cross.

-

USD/BRL — 4.9145 (-0.56% daily): The Brazilian real is the standout EM performer this year, with USD/BRL down 13.09% year-on-year and 10.92% YTD — one of the steepest dollar declines in the EM universe. Commodity-export strength and improved risk appetite for Brazil have powered the real's rally.

-

USD/ZAR — 16.3923 (-0.67% daily): The South African rand firmed on Monday amid broader dollar softness and firmer commodity prices. The pair is down 9.70% year-on-year (rand has strengthened vs. dollar), though the ZAR remains sensitive to global risk sentiment shifts.

Strategist Takes

-

Bank of America on USD/CNY (paraphrased, Investing.com, May 11, 2026): BofA analysts see "mild yuan strength" as the most likely outcome following a Trump-Xi Beijing summit, citing historical FX dynamics around high-level diplomatic engagements. The bank's strategists analyzed past patterns of yuan movement around U.S.-China summits, concluding the base case favors further modest USD/CNY downside from current levels near 6.80.

-

UBS on USD/KRW (paraphrased, Investing.com, May 11, 2026): UBS maintains a bullish view on the Korean won relative to the U.S. dollar, with the call underpinned by favorable balance-of-payments dynamics. The bank sees structural current-account surplus flows as a persistent tailwind for won appreciation, arguing the currency remains undervalued relative to fair-value models despite recent volatility.

-

Günay Caymaz / Investing.com Analysis (May 11, 2026): In a fresh piece titled "US Dollar Coils in a Tight Range as Markets Watch CPI, Fed Signals This Week," the analyst argues that "rising Middle East tensions and oil prices continue supporting" a cautious tone in FX markets, with the DXY stuck between competing forces: geopolitical safe-haven demand on the one side, and structural dollar-negative forces (twin deficits, Fed hold) on the other. The piece flags CPI and subsequent Fed commentary as the decisive near-term catalysts.

What to Watch Next

-

U.S. CPI (May 13, Tuesday) — The single most important event for FX this week. A hotter-than-expected print would re-anchor rate-hold expectations more firmly and likely support DXY recovery; a soft print could reinvigorate EUR/USD bulls toward 1.19. Most sensitive pairs: EUR/USD, USD/JPY, DXY.

-

U.K. CPI (Tuesday) — Sterling is watching this print closely after slipping on Monday. GBP/USD at 1.3628 is vulnerable to a downside miss; a hot reading could push cable back toward the 1.3750 area. Most sensitive pair: GBP/USD.

-

Middle East Geopolitics (ongoing) — Trump's rejection of Iran's peace-proposal response keeps the risk premium elevated. Any escalation (military action or sanctions) could spike oil, support NOK and commodity currencies, and trigger yen safe-haven buying. Most sensitive: USD/JPY, USD/NOK, AUD/USD.

-

BOJ Intervention Threshold / USD/JPY (ongoing, elevated risk this week) — With USD/JPY back at 157, the pair is squarely inside the zone where Japan's Ministry of Finance intervened on April 30, 2026. Any further dollar strength toward 158–160 risks a fresh intervention. Watch for sharp intraday reversals in USD/JPY.

Reader Action Items

-

Watch EUR/USD at the 1.18 level: The pair is pressing multi-month highs near 1.1787. Tuesday's U.S. CPI is the binary event — a soft print could push EUR/USD decisively through 1.18 toward the 1.19 area, while a hot number may pull it back toward 1.165–1.170 support. Position sizing should account for above-average volatility around the data release.

-

USD/JPY intervention risk is live at 157: The MOF has shown its hand at these levels (April 30 intervention). Long USD/JPY positions face asymmetric risk — modest upside if the dollar edges higher, but sharp reversal risk if Japanese authorities act. Consider tight stop-loss placement above 158.

-

EM carry trades (MXN, BRL) remain in focus: Both the Mexican peso and Brazilian real have posted exceptional YTD and year-on-year gains. High carry still attracts flows, but with geopolitical risk simmering and CPI data pending, a sudden risk-off move could unwind these positions quickly. Monitor risk sentiment indicators alongside EM currency positions this week.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by