Global & Korea Equity Market Intelligence — 2026-05-12

KOSPI touched 7,999 intraday on May 12 before pulling back slightly under foreign selling pressure, while KOSDAQ maintained strength alongside the AI semiconductor rally. The biggest global driver remains rising oil prices from the stalled U.S.-Iran nuclear negotiations, with S&P 500 and Nasdaq staying modestly higher on AI chip momentum. Tomorrow's Asia session will pivot on April U.S. CPI data, with the KRW/USD exchange rate and foreign investor flows emerging as key variables for whether KOSPI breaks through 8,000.

Global & Korea Equity Market Intelligence — 2026-05-12

Market Snapshot — By the Numbers

| Index | Close | Change | Notes |

|---|---|---|---|

| KOSPI | 7,999 (intraday high) / Closed slightly lower | — | Foreign selling pressure |

| KOSDAQ | Higher | — | AI & semiconductor strength |

| S&P 500 | New all-time high | Modest ▲ | AI semiconductors leading |

| Nasdaq | New all-time high | Modest ▲ | Tech stocks driving |

| Dow Jones | Modest volatility | — | Oil uncertainty, Iran concerns |

| Nikkei 225 | Mixed | — | Asian mixed tone |

| Hang Seng | Mixed | — | Asian mixed tone |

⚠️ Note: Some precise figures unavailable due to data extraction limitations. Verified figures used in sections below take priority.

Korea Market Deep Dive

KOSPI

- Intraday high: 7,999 — just one point shy of the historic 8,000 milestone

- Session character: Hyundai Motor and Samsung Electro-Mechanics each jumped 8%, driving the index, while investors awaited April U.S. CPI data

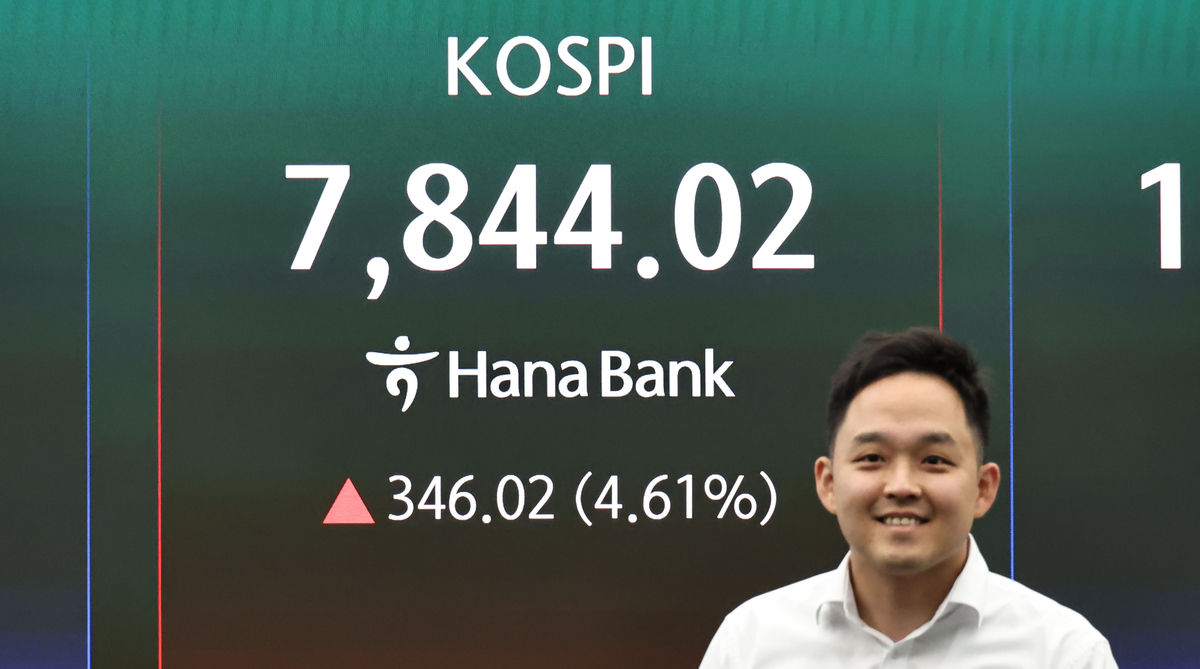

- Foreign flows: Following intraday 7,822.24 (+4.32%) on May 11, foreign investors switched to net selling as profit-taking accelerated — Korea Exchange data confirms shift to net outflow

- Market cap: Korea's entire stock market capitalization surpassed 7 trillion won for the first time in history

KOSDAQ

- Direction: Maintained strength alongside AI and semiconductor themes

- Leadership: AI-linked mid-cap semiconductor and materials names led the way, tracking KOSPI strength

Top Movers (Korea)

Gainers

- Hyundai Motor (005380 KS) (+8%): Core driver of KOSPI's run to 7,999 — earnings expectations combined with AI and electrification premium fueled the surge

- Samsung Electro-Mechanics (009150 KS) (+8%): Automotive and AI component demand expectations lifted it alongside Hyundai

- Samsung Electronics (005930 KS) (Strong): AI semiconductor buying concentrated here; maintained upward momentum after crossing $1 trillion market cap

- SK Hynix (000660 KS) (Strong): By market cap, surpassed U.S. pharma giant Eli Lilly to enter global Top-10 — HBM demand continues to expand

Losers

- Bottom 30% of KOSPI (Broad): Despite KOSPI hitting new highs, 30%+ of listed companies have declined year-to-date — market bifurcation intensifies as Samsung and Hynix hog the rally

- Foreign profit-taking targets: After yesterday's +4.32% spike, foreign investors began trimming gains, paring some large-cap positions

- Middle East risk exposure: Iran nuclear deadlock reignited oil pressure, squeezing energy-cost-sensitive sectors

Sector Flows

-

Semiconductors (AI chips): Samsung Electronics and SK Hynix led by AI chip buying that monopolized KOSPI gains. SK Hynix surpassed U.S. pharma heavyweight Eli Lilly by market cap, while TSMC, Samsung, and Hynix trio sparked concentration-risk debate across Korea and Taiwan markets. Bloomberg data shows Korea's equity market up +75% year-to-date, already matching 2025's global best return (+76%) in just five months.

-

Autos & EV components: Hyundai Motor's 8% jump signals strength beyond semiconductors — AI electrification premium and earnings expectations converge

-

Battery & EV parts: Samsung Electro-Mechanics +8% caught attention. AI and automotive demand crosscurrents highlighted, though Middle Eastern oil anxiety raises questions about EV demand outlooks

-

Market bifurcation (Risk factor): Despite KOSPI new highs, 30%+ of listed stocks down since year-start — sustained rally concentration in two names risks deepening mid-cap neglect

Global Drivers Behind Today's Tape

%3Amax_bytes(150000)%3Astrip_icc()%2FGettyImages-2275114985-f6043eb7a75f43ce9e81c7727f0bfe3a.jpg)

-

AI semiconductor momentum persists: S&P 500 and Nasdaq each closed at record highs, driven by semiconductor and tech buying tied to AI themes — the same global narrative powering KOSPI's chip rally is alive in New York

-

U.S.-Iran nuclear stalemate → Oil pressure renewed: President Trump dismissed Iran's peace response as "totally unacceptable," resurfacing Middle East geopolitical risk. Oil rose 2% on the day, partly constraining KOSPI's push through 8,000 despite chip strength

-

April U.S. CPI watch: Market participants entered cautious mode ahead of inflation data release. U.S. equity index futures and KRW/USD will react sharply to CPI, with the Fed's rate path adjustment in focus

-

Korean market concentration risk goes global: CNBC published analysis that TSMC, Samsung, and SK Hynix represent excessive concentration in Korea and Taiwan rally, triggering foreign profit-taking psychology

Asia Read-Through

Tomorrow's (May 13) Asian session hinges on April U.S. CPI data released tonight. A CPI miss could reignite Fed pivot hopes, enabling KRW strength and KOSPI's 8,000 re-test. A CPI surprise beat risks dollar strength and rate hike worries, triggering more foreign selling. Weekend developments on Iran nuclear talks and crude price moves will also shape Monday Asia open.

What to Watch Next

- Economic data: April U.S. CPI release (May 12 U.S. time) — core inflation trajectory and energy price component critical to Fed path

- Technical levels: KOSPI 8,000 psychological resistance is the focal point; support sits around yesterday's close at 7,820–7,850. KOSDAQ's continued uptrend also key

- Pending events: Trump's China visit timing and Fed Chair confirmation vote timing (per Schwab report)

- Macro watch: KRW/USD rate — linked to foreign flow direction; Brent crude — Iran risk premium sustainability affects cost burden; U.S. 10-year yield — could swing sharply post-CPI

Reader Action Items

-

Domestic retail investors: Watch for volatility around KOSPI's 8,000 breakout. If portfolios are overweighted to Samsung Electronics and SK Hynix, taking profit on 8% jumpers like Hyundai Motor and Samsung Electro-Mechanics post-rally may be prudent. The fact 30%+ of listed stocks are down year-to-date—independent of index level—underscores stock picking remains critical.

-

Global investors with Korea exposure: With SK Hynix surpassing Eli Lilly by market cap and Korea's total market cap hitting 7 trillion won, now is the time to review ADR spreads versus local shares. KRW hedging costs may shift sharply post-CPI, so consider tweaking hedge ratios for dollar-strength scenarios.

-

Contrarian angle: Consensus treats KOSPI 8,000 as natural AI semiconductor rally extension, but the overlooked risk is concentration. With CNBC already raising this publicly, foreign flow "concentration unwind" selling could hit mid-tier semiconductor names first—ironically opening rotation into neglected sectors (defense, K-biotech, materials).

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by