InsurTech Innovation — 2026-05-12

The week of May 4–9, 2026 was the heaviest single week of insurtech capital deployment all year, with $820 million disclosed across just four transactions — every deal AI-native. London-based Zego landed a $150 million Series C to join the unicorn club, while CB Insights' Q1 2026 State of Insurtech report confirmed the sector is on pace for record-high deal sizes. The dominant theme is unambiguous: AI is no longer a pilot program — it is the infrastructure layer every new insurtech dollar is buying.

InsurTech Innovation — 2026-05-12

Headline Deals (at least 3)

Zego — $150M Series C

- What they do: London-based insurtech providing flexible, usage-based commercial motor insurance for fleets, gig-economy drivers, and mobility businesses

- Segment: P&C / Embedded / Commercial Motor

- Investors or partners: Not fully disclosed in available sources; round brings Zego to unicorn status

- Valuation / traction: Round propels Zego into the UK fintech unicorn club alongside Revolut and Checkout.com

- Why it matters: A unicorn milestone for a European commercial motor insurtech signals continued investor appetite for usage-based models — an area where incumbents still largely rely on annual premium structures. Competitors offering fleet or gig-economy cover should expect pricing pressure as Zego scales distribution.

Week of May 4–9 Cohort — $820M Across 4 Deals (AI-Native Stack)

- What they do: Per InsurTech.ME's Investment Intelligence Report, four transactions collectively deployed $820M into AI-native startups attacking distinct layers of insurance infrastructure: claims administration, carrier underwriting, software modernization, and catastrophe capital

- Segment: P&C / Reinsurance / Claims / Broker-tech

- Investors or partners: Not individually named in available sources

- Valuation / traction: $820M disclosed — heaviest single week of 2026 by capital deployed

- Why it matters: Every deal in the cohort is AI-native, and each targets a different infrastructure layer rather than a single product niche. This breadth signals that investors see AI as a horizontal platform play across the entire insurance stack, not a point-solution bet.

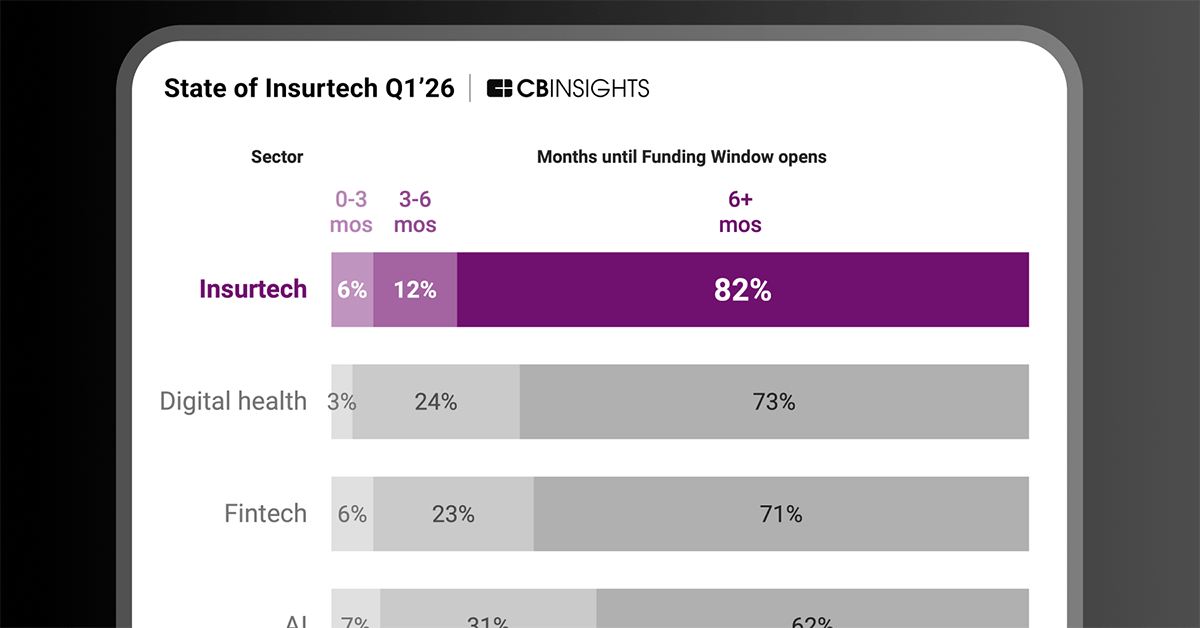

CB Insights State of Insurtech Q1 2026 — Record Deal Sizes on Track

- What they do: CB Insights' quarterly benchmark tracking insurtech funding trends globally

- Segment: Cross-segment (data / analytics)

- Investors or partners: N/A (research report)

- Valuation / traction: InsurTech is "on track for record-high deal sizes in 2026 as competitive pressure intensifies"

- Why it matters: Record deal sizes in a quarter where AI captures an outsized share of capital (Gallagher Re previously noted AI startups captured 95.2% of insurtech funding) suggests the gap between AI-native challengers and legacy carriers is widening faster than most incumbents have planned for. Strategy teams should treat this as a leading indicator, not a lagging one.

Product & Technology Launches (at least 3)

-

Zywave — Spring 2026 Release with Insurance-Specific AI Agents: Zywave announced platform enhancements featuring insurance-specific AI agents designed to power smarter selling across the insurance ecosystem, targeting brokers and carriers looking for measurable revenue growth from AI adoption. The release is positioned as moving beyond generic AI tools toward purpose-built agents trained on insurance workflows.

-

Norton Rose Fulbright — Insurathon 2026 (9th Edition): Global law firm Norton Rose Fulbright launched the ninth edition of its Insurathon competition, offering InsurTech startups and scale-ups £50,000 in combined legal support and potential investment. Structured as both a competition and an accelerator-style program, it provides a rare non-dilutive capital pathway for early-stage insurtechs seeking to validate product-market fit with legal infrastructure.

- Roots Automation — Straight-Through Claims Processing Roadmap: Roots Automation projects that by late 2026, AI will handle 70%–90% of simple claims through straight-through processing with no adjuster involvement. The company is expanding AI transformation across underwriting, claims, policy servicing, and customer experience, while beginning to extend into actuarial analysis, compliance workflows, and producer management.

Incumbent Carrier Moves

No verified fresh carrier-specific partnership or investment announcements with confirmed dates after 2026-05-05 were available in the research results for this period.

- Digital Insurance on AI in P&C: Digital Insurance published a strategic analysis this week confirming that "in 2026, artificial intelligence is no longer an experimental technology — it is a strategic necessity embedded across the insurance value chain," with P&C carriers explicitly highlighted as being in the midst of AI integration across underwriting and claims. While not a single carrier deal, this editorial consensus from the sector's leading trade publication signals that incumbent carriers are being benchmarked against AI-native standards publicly.

Theme Deep-Dive: AI as Insurance Infrastructure — Not a Feature, a Stack

The week of May 4–9, 2026 crystallized what has been building for two years: AI is not a product feature insurtech startups bolt onto an existing workflow. It is the foundational infrastructure layer on which the next generation of insurance companies is being built from the ground up.

The InsurTech.ME Investment Intelligence Report for the week noted that all four deals in the $820M cohort are AI-native, and crucially, each attacks a different layer of the insurance infrastructure stack — claims administration, carrier underwriting, software modernization, and catastrophe capital. This is a materially different pattern from 2023–2024, when AI funding tended to cluster in claims automation or chatbot-style customer service.

Two companies illustrate contrasting approaches to this AI-native paradigm.

Roots Automation is attacking the claims layer with a straight-through processing model. The company projects that by late 2026, AI will handle 70%–90% of simple claims with zero adjuster involvement. Their roadmap also extends AI into actuarial analysis, compliance audit preparation, and producer management — effectively treating the insurer's entire back office as automatable territory. This is a horizontal play that competes with legacy BPO providers and internal carrier operations teams simultaneously.

Corgi Insurance (which closed its $160M Series B at a $1.3B valuation in the prior week, covered in our May 8 issue) represents the other pole: AI embedded in underwriting and claims processing for a full-stack specialty carrier focused on startups. Rather than selling AI tools to incumbents, Corgi is the carrier, using AI to compress the underwriting cycle and expand into new verticals at speed.

The contrast matters strategically. Roots Automation's model assumes incumbents will buy AI capabilities rather than build them — a bet on enterprise sales into large carriers. Corgi's model assumes the AI advantage is so durable that it's worth building an entirely new carrier around it.

CB Insights' Q1 2026 State of Insurtech report confirms the macro context: deal sizes are on track for record highs, with competitive pressure intensifying. For incumbents, the window to acquire rather than compete is narrowing as AI-native insurtechs scale and achieve unicorn valuations — Zego's $150M Series C being the latest example.

The AI Magazine's analysis of Q1 2026 insurtech funding ($1.63 billion total) adds another dimension: AI-focused models surged specifically as "digital risks converge" — meaning the AI boom is simultaneously creating new insurable risks (AI liability, model failure, cyber-AI exposure) and providing the analytical tools to price them. This dual dynamic makes AI both the product and the underwriting engine.

M&A, Exits & Shutdowns

- Quiet week for M&A and exits. No verified acquisitions, IPO filings, down-rounds, or shutdowns with confirmed post-May 5, 2026 dates were identified in available research results.

By the Numbers

- Disclosed funding this period (May 4–9): $820M (4 transactions per InsurTech.ME) + $150M Zego Series C

- Largest round: Zego ($150M Series C, unicorn milestone)

- Most active investor(s): Not disclosed in available sources for this specific week

- Hottest sub-segment: AI-native full-stack infrastructure — every deal in the May 4–9 cohort is AI-native across claims, underwriting, software modernization, and cat capital

- Geographies in focus: UK (Zego unicorn), US (Roots Automation, Corgi context); Q1 2026 data shows global reach at $1.63B

What to Watch Next

-

CB Insights Q1 2026 Full Report release: The State of Insurtech Q1 2026 report is flagged as newly published — detailed deal-by-deal breakdowns from this report are expected to surface in trade press over the coming week, likely revealing which specific sub-segments are driving record deal sizes.

-

Roots Automation's late-2026 straight-through claims milestone: The company has set a public benchmark — 70%–90% of simple claims processed by AI with no adjuster by end of 2026. Watch for Q3 operator disclosures or case studies from carrier pilot partners that validate or challenge this projection.

-

Insurathon 2026 finalists: Norton Rose Fulbright's ninth-edition competition is now open. Finalist announcements will be an early signal of which emerging insurtech verticals are attracting legal-commercial validation from global law firm partners — often a leading indicator of regulatory readiness in new coverage categories.

Reader Action Items

-

For incumbent carrier strategy teams: The May 4–9 cohort's structure — four AI-native companies each targeting a different infrastructure layer — is a direct map of where incumbents are most exposed. Assess your claims administration, underwriting decision tooling, core software stack, and catastrophe capital modeling independently. If any layer relies primarily on human judgment without AI augmentation, a funded startup is already building your replacement. The Zego unicorn milestone also signals that usage-based commercial motor is no longer a niche experiment — fleet and gig-economy books deserve a formal competitive response.

-

For founders / operators: The gap revealed this week is in the middle layers of insurance operations — specifically software modernization (legacy core systems) and catastrophe capital modeling. These are the least glamorous but most durable moats. With $820M deployed in one week and every dollar AI-native, founders pitching legacy core replacement or AI-driven cat modeling will find the funding climate unusually receptive heading into Q3 2026. The Insurathon competition also represents a non-dilutive £50K legal-support pathway worth pursuing for pre-seed and seed-stage companies needing regulatory infrastructure before raising institutional capital.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by