Stablecoin Monitor — 2026-05-06

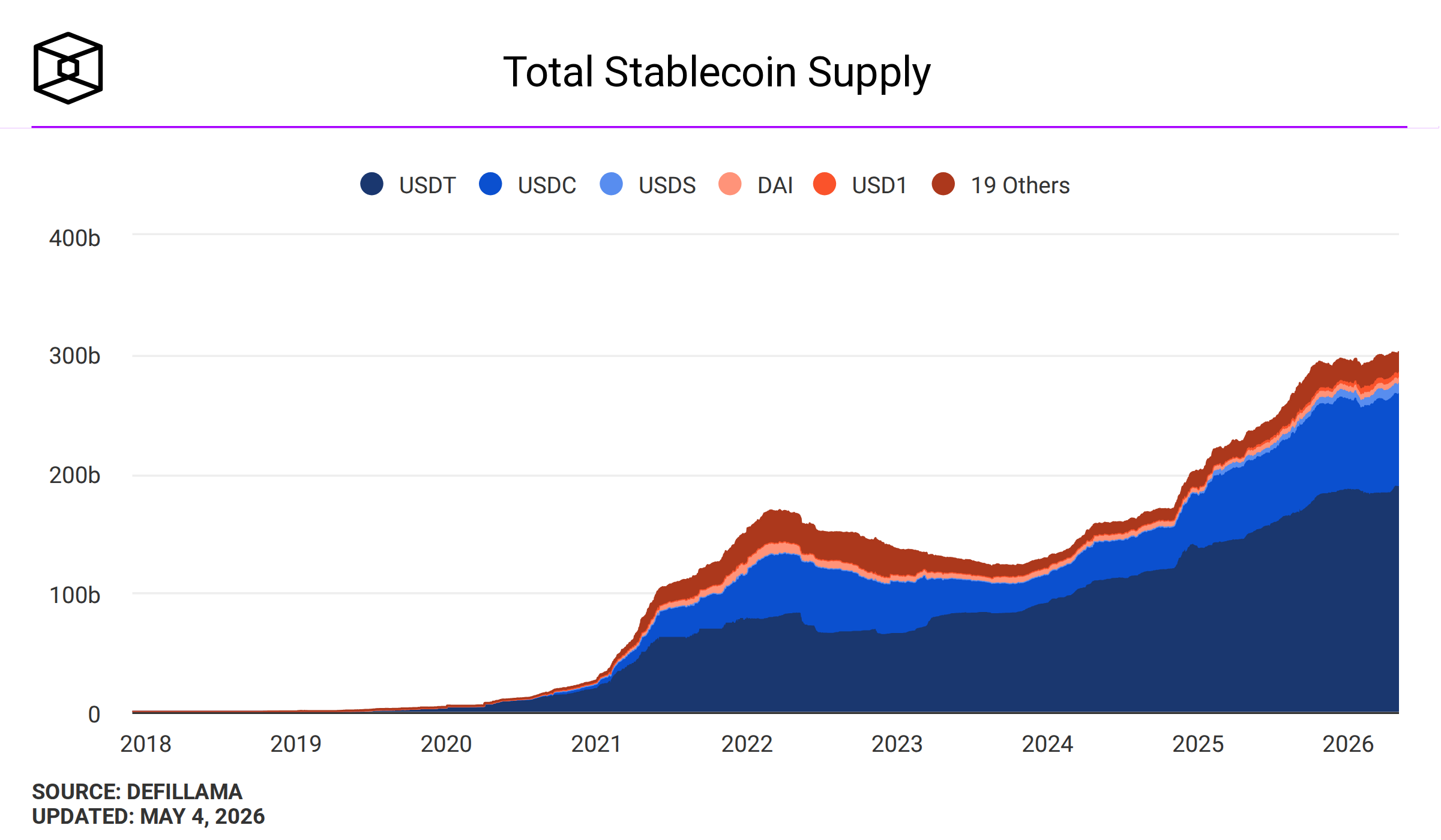

The stablecoin market continues its record-setting expansion, with USDT holding at approximately $189.5B and USDC reaching $77.6B as total supply pushes well above $320B. The biggest narrative of the day is a bold long-term forecast: Bitwise's CIO projects global stablecoin supply could surge to $4 trillion by 2030. On the regulatory front, the US GENIUS Act framework and EU MiCA compliance requirements continue to reshape competitive dynamics between Tether and Circle.

Stablecoin Monitor — 2026-05-06

Market Snapshot

| Stablecoin | Market Cap | 24h Direction | Peg Status |

|---|---|---|---|

| USDT (Tether) | ~$189.5B | Stable | $1.00 ✅ |

| USDC (Circle) | ~$77.6B | Stable | $1.00 ✅ |

| DAI/USDS (Sky) | ~$4.7B | Stable | $1.00 ✅ |

| FDUSD | Active | Stable | $1.00 ✅ |

| PYUSD (Paxos/PayPal) | Active | Stable | $1.00 ✅ |

| USDe (Ethena) | Active | Stable | ~$1.00 ✅ |

Total stablecoin supply remains above $320B following an all-time high of $321B recorded in April 2026, representing over 24 months of continuous growth.

Key Developments

1. Bitwise CIO Projects $4 Trillion Stablecoin Supply by 2030

Bitwise Chief Investment Officer Matt Hougan has issued a striking long-term forecast, arguing that global stablecoin supply could reach approximately $4 trillion by 2030 — roughly 12x the current market. Hougan cited accelerating institutional adoption, clearer US regulatory frameworks, and growing real-world payment use cases as the primary drivers.

2. April 2026 Stablecoin Report: Record $321B Market Cap, Meta USDC Payouts

A comprehensive April 2026 recap confirms the market hit a new all-time high of $321B in market cap. Among the notable milestones: Meta began paying creators in USDC via Stripe, marking a significant mainstream adoption step. The month also saw three federal agencies drop new stablecoin-related rules in a single week, signaling an accelerating US regulatory pace.

3. Liquidity Infrastructure Emerges as Critical Factor in Stablecoin Ecosystem

As the number of stablecoin issuers proliferates, B2C2's Cactus Raazi argues that seamless interoperability and deep liquidity have become central competitive differentiators. The analysis highlights that moving value efficiently across the stablecoin ecosystem — from USDT to USDC to yield-bearing variants — depends increasingly on robust liquidity infrastructure rather than the underlying peg mechanism alone.

Regulatory & Compliance Tracker

🇺🇸 United States — GENIUS Act Advances, Federal Agencies Issue Coordinated Rules

The US GENIUS Act framework — which would require 1:1 reserves in US dollars, short-term Treasury bills, overnight repos, or Federal Reserve credits — continues to advance. The April 2026 period saw three federal agencies issue coordinated stablecoin-related rules in a single week, a significant escalation in the pace of US regulatory action. Issuers under the proposed framework would be required to publish monthly reserve reports audited by registered accounting firms, with executives facing criminal penalties for violations. As of early 2026, no single federal stablecoin statute has been enacted, though multiple bills have advanced through Congress.

🇪🇺 European Union — MiCA Compliance Reshaping Market Share

Under Europe's MiCA framework, provisions covering Asset-Referenced Tokens (ARTs) and E-Money Tokens (EMTs) are in full force, imposing strict reserve requirements, whitepaper disclosures, and authorization processes for stablecoin issuers. USDC's compliance with MiCA's strictest criteria is cited as a key driver of its 220% supply surge since late 2023, while Tether's USDT faces ongoing scrutiny over its compliance posture in EU markets. Algorithmic stablecoins remain unregulated and cannot be marketed as "stablecoins" under MiCA, the GENIUS Act, or Singapore's framework.

On-Chain & DeFi Pulse

DeFi Yields Compress Below TradFi Rates

A significant structural shift is underway in DeFi: stablecoin yields in decentralized protocols have collapsed below traditional finance savings rates, according to CoinDesk analysis from April 2026. Investors are now being asked to accept higher smart contract risks for lower returns compared to a simple savings account, as regulation and exploits mount. This compression is forcing a re-evaluation of DeFi-native stablecoin strategies across major protocols.

Stablecoin Treasury Management: sUSDe, sUSDS Among Yield-Bearing Options

Enterprise treasury whitelists in 2026 now typically include USDC, USDT, USDS (formerly DAI), and PYUSD as core holdings, with yield-bearing variants including sUSDe (Ethena), sUSDS (Sky savings rate), and sFRAX (Frax) increasingly appearing in more aggressive yield-seeking treasury policies. This diversification signals that stablecoins are maturing beyond simple dollar-pegged instruments into a tiered ecosystem of risk-adjusted products.

Analysis: What It Means

The stablecoin market is in a remarkable dual-track moment: structurally expanding at the macro level while facing yield compression at the protocol level. Bitwise's $4 trillion forecast for 2030 — if accurate — would represent a near 12x growth from today's ~$321B market, driven by the same regulatory clarity that is currently squeezing out non-compliant players. This is the essential paradox: the very regulation that is constraining some actors (particularly Tether in EU markets) is also the foundation for institutional confidence that could fuel the next wave of adoption.

The Meta/Stripe USDC payment rollout announced in April stands as perhaps the most consequential development of the past month — mainstream consumer platforms embedding stablecoins into payout infrastructure represents a qualitatively different kind of adoption than trading or DeFi collateral use. The Federal Reserve Kansas City report finding that stablecoins are "rarely used for payments" may soon become outdated, as this real-world integration accelerates.

The compression of DeFi yields below TradFi rates creates a strategic dilemma for the ecosystem. Yield-bearing stablecoins like sUSDe and sUSDS are emerging as a bridge — but they carry smart contract risk that pure-play institutional buyers are unlikely to accept at scale. The battle for the next $3 trillion in stablecoin growth will be won on the TradFi-native side: reserve transparency, regulatory compliance, and fiat on/off-ramp depth, not DeFi yield optimization.

What to Watch Next

- US GENIUS Act vote timeline: No single federal stablecoin statute has been enacted as of May 2026 — the next committee action or floor vote could trigger significant market re-pricing of USDC vs. USDT competitive dynamics

- Monthly reserve audit publications: Both Tether and Circle publish reserve attestations on a monthly cadence; the next scheduled reports will be scrutinized for any shifts in reserve composition given Treasury yield movements

- Meta/Stripe USDC creator payout expansion: Whether Meta's USDC payout pilot scales to a broader user base is a key indicator of real-world stablecoin payment adoption

- MiCA enforcement actions: Watch for the first significant EU regulatory enforcement actions against non-compliant stablecoin issuers under the full MiCA framework

- DeFi TVL trajectory: With yields compressing, monitor whether stablecoin TVL in major DeFi protocols (Aave, Curve, Morpho) stabilizes or continues declining as capital rotates to TradFi alternatives

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by