Stablecoin Monitor — 2026-05-07

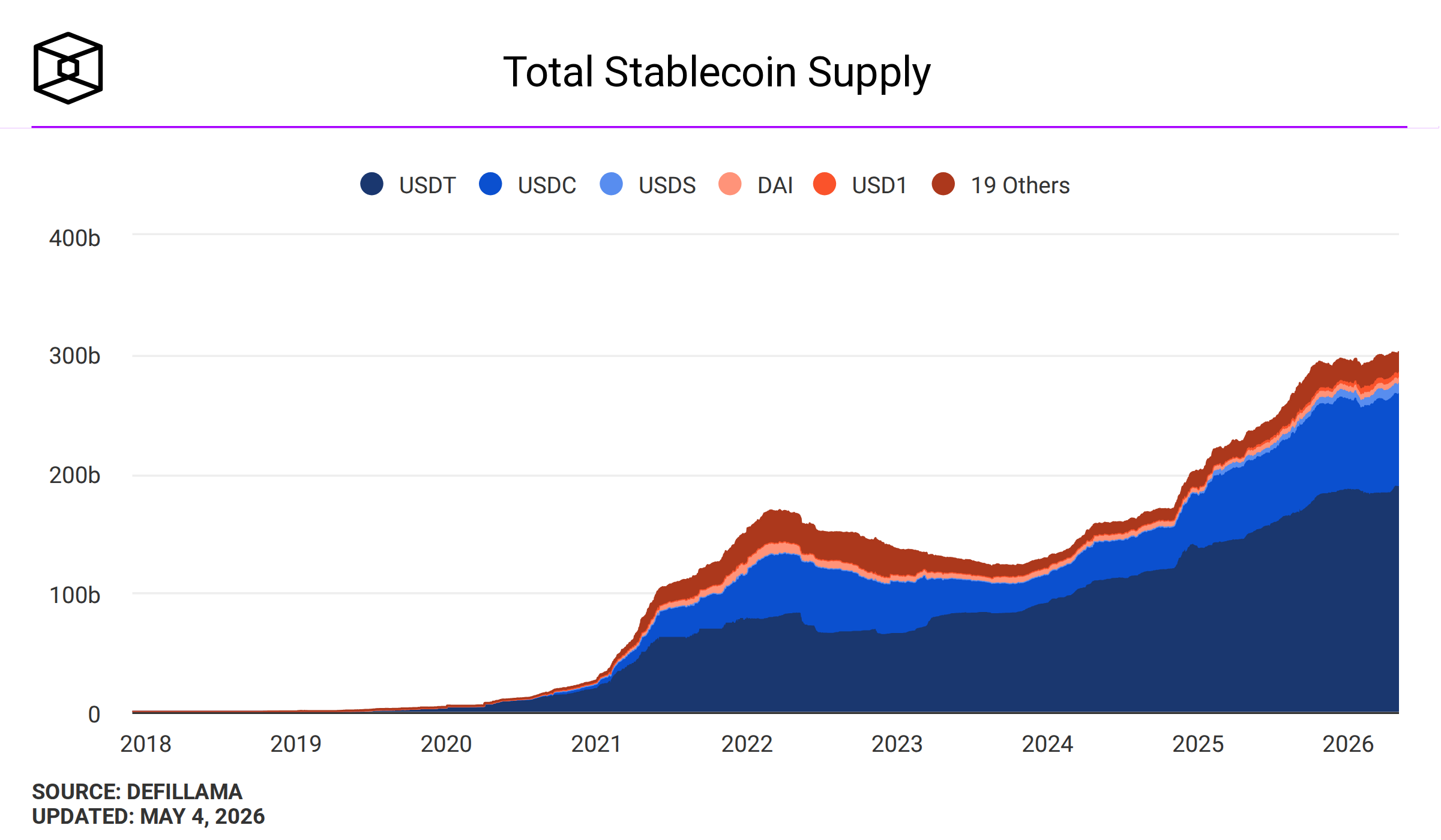

The total stablecoin market has crossed $260 billion in combined supply, with Tether (USDT) and Circle (USDC) continuing to dominate. The biggest story of the day is a pointed critique from payments firm Bridge, whose head of money movement argues that the duopoly of Tether and Circle is actively harmful to stablecoin adoption — while Bitwise's CIO separately forecasts the market could reach $4 trillion by 2030.

Stablecoin Monitor — 2026-05-07

Market Snapshot

| Stablecoin | Est. Market Cap | 24h Direction | Peg Status |

|---|---|---|---|

| USDT (Tether) | ~$189.5B | Stable | On-peg |

| USDC (Circle) | ~$77.1B | Stable | On-peg |

| DAI/USDS (Sky) | Data unavailable | — | On-peg |

| FDUSD | Data unavailable | — | On-peg |

| PYUSD (PayPal/Paxos) | Data unavailable | — | On-peg |

| USDe (Ethena) | Data unavailable | — | On-peg |

Combined, Tether and Circle now control approximately $260 billion of the stablecoin market, representing an overwhelming share of total supply. USDT holds roughly 73% of the two-token combined total, with USDC at ~27%.

Key Developments

1. Bridge Executive Calls Tether-Circle Dominance a "Net Bad" for Stablecoins

Ben O'Neill, head of money movement at payments infrastructure firm Bridge, publicly argued that the concentration of the stablecoin market in just two players — Tether's USDT and Circle's USDC — is harmful to the broader ecosystem. O'Neill contends that their dominance is making it harder for stablecoins to "feel like money," with rising burn fees cited as a specific drag on mainstream adoption. The critique arrives as the combined market cap of the two firms approaches $260 billion.

2. Bitwise CIO: Stablecoin Supply Could Hit $4 Trillion by 2030

Bitwise Chief Investment Officer Matt Hougan issued a bullish long-term forecast, projecting that global stablecoin supply could surge to approximately $4 trillion by 2030. The prediction reflects accelerating institutional adoption, expanding use cases in payments and treasury management, and improving regulatory clarity across major jurisdictions.

3. April 2026 Stablecoin Report: Record $321B Market Cap, Meta Pays Creators in USDC

A comprehensive April 2026 stablecoin report published this week highlights several milestones: a record $321 billion market cap was reached during the month, Meta began paying creators in USDC via Stripe, and three separate U.S. federal agencies issued new stablecoin-related rules within a single week. The report marks April as a pivotal month for institutional integration of dollar-denominated stablecoins.

Regulatory & Compliance Tracker

United States: Reserve Requirements and Monthly Audits Now Expected

Emerging U.S. legislative frameworks — including the advanced GENIUS Act — are coalescing around a strict 1:1 reserve requirement, mandating that stablecoin issuers back every token with high-quality liquid assets such as U.S. Treasuries, cash equivalents, short-term Treasury bills, overnight repos, or Federal Reserve credits. The frameworks also require issuers to publish monthly reserve reports audited by registered accounting firms, with executives facing potential criminal penalties for non-compliance. As of early 2026, no single federal stablecoin statute has been fully enacted, but multiple bills have advanced through congressional committees.

European Union: MiCA Provisions Now in Full Force for Stablecoin Issuers

Under the EU's Markets in Crypto-Assets (MiCA) regulation, provisions covering Asset-Referenced Tokens (ARTs) and E-Money Tokens (EMTs) are now active. The rules impose strict reserve requirements, mandatory whitepaper disclosures, and formal authorization processes for any stablecoin issuer operating in the EU. Algorithmic stablecoins remain explicitly excluded from the MiCA framework — they cannot be marketed as "stablecoins" — a distinction that continues to shape competitive dynamics globally. USDC has emerged as a primary beneficiary of MiCA compliance standards, with its supply surging 220% since late 2023 as it satisfies MiCA's strictest criteria.

On-Chain & DeFi Pulse

Treasury Whitelists Standardizing Around Core Stablecoins

A 2026 treasury management guide published this week indicates that enterprise stablecoin whitelists are rapidly standardizing. The typical institutional whitelist now includes USDC (Circle), USDT (Tether), USDS (Sky, formerly DAI), and PYUSD (Paxos). Yield-bearing variants including sUSDe (Ethena), sUSDS (Sky savings rate), and sFRAX (Frax) are appearing in policies that permit yield-bearing positions, signaling that institutional DeFi integration is deepening beyond simple treasury holds.

L2 Stablecoin Liquidity: Ethereum Dominates, But Gaps Persist

Data from DefiLlama's chain pages and Curve's pool registry (as of April 24, 2026) shows significant liquidity fragmentation across Layer 2 networks. Established L2s can execute large stablecoin swaps with under 0.05% slippage in deep USDC, USDT, DAI, USDS, FDUSD, and PYUSD pools — while lower-liquidity chains like Scroll show slippage as high as 1.2% for equivalent swaps. This fragmentation presents ongoing challenges for cross-chain stablecoin usability and arbitrage efficiency.

Analysis: What It Means

The stablecoin market finds itself at an inflection point defined by concentration and contestation. With Tether and Circle jointly controlling roughly $260 billion — and a combined dominance that is arguably more entrenched today than at any prior point — the critique from Bridge's Ben O'Neill carries practical weight. If payment network fees rise as dominant issuers extract more value from their positions, challenger stablecoins face a structural headwind: they must compete on compliance and liquidity while the incumbents benefit from deep integrations and brand recognition.

The regulatory picture is pushing in a direction that paradoxically could entrench the big two even further. In both the U.S. and EU, emerging rules favor issuers with the capital and compliance infrastructure to meet strict 1:1 reserve mandates, monthly audits, and formal authorization processes. Tether's ambiguous reserve transparency has long been a liability in European markets; MiCA's active enforcement could accelerate further USDC gains in the EU while leaving USDT dominant in emerging market corridors where MiCA has less reach.

At the same time, Bitwise's $4 trillion projection for 2030 reflects genuine market optimism that is not unfounded: Meta paying creators in USDC, enterprise treasury whitelists formalizing around institutional stablecoins, and DeFi protocols integrating yield-bearing variants all point to a market that is maturing from trading-desk infrastructure into something closer to genuine monetary plumbing. The outstanding question is whether regulatory clarity arrives fast enough — and equitably enough — to allow meaningful competition to emerge alongside the incumbents.

What to Watch Next

- U.S. GENIUS Act progress: Congressional committees are advancing multiple stablecoin bills; any floor vote or markup session would be a major catalyst for both compliance timelines and market structure.

- Tether reserve audit disclosures: As U.S. frameworks mandate monthly audited reserve reports, Tether faces increasing pressure to match Circle's reporting cadence — watch for any voluntary or compelled disclosures.

- MiCA enforcement actions: Now that EU rules are fully active for EMTs and ARTs, the first formal enforcement actions against non-compliant issuers could arrive in coming weeks.

- Bridge and payment-layer stablecoin challengers: Following Ben O'Neill's public critique, watch for Bridge or similar firms to announce competing stablecoin products or integrations designed to undercut USDT/USDC fee structures.

- Ethena (USDe) and yield-bearing stablecoin inflows: As institutional whitelists increasingly include sUSDe and similar instruments, on-chain TVL data in the coming days will reveal whether April's record market cap has translated into sustained DeFi inflows.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by