Stablecoin Monitor — 2026-06-15

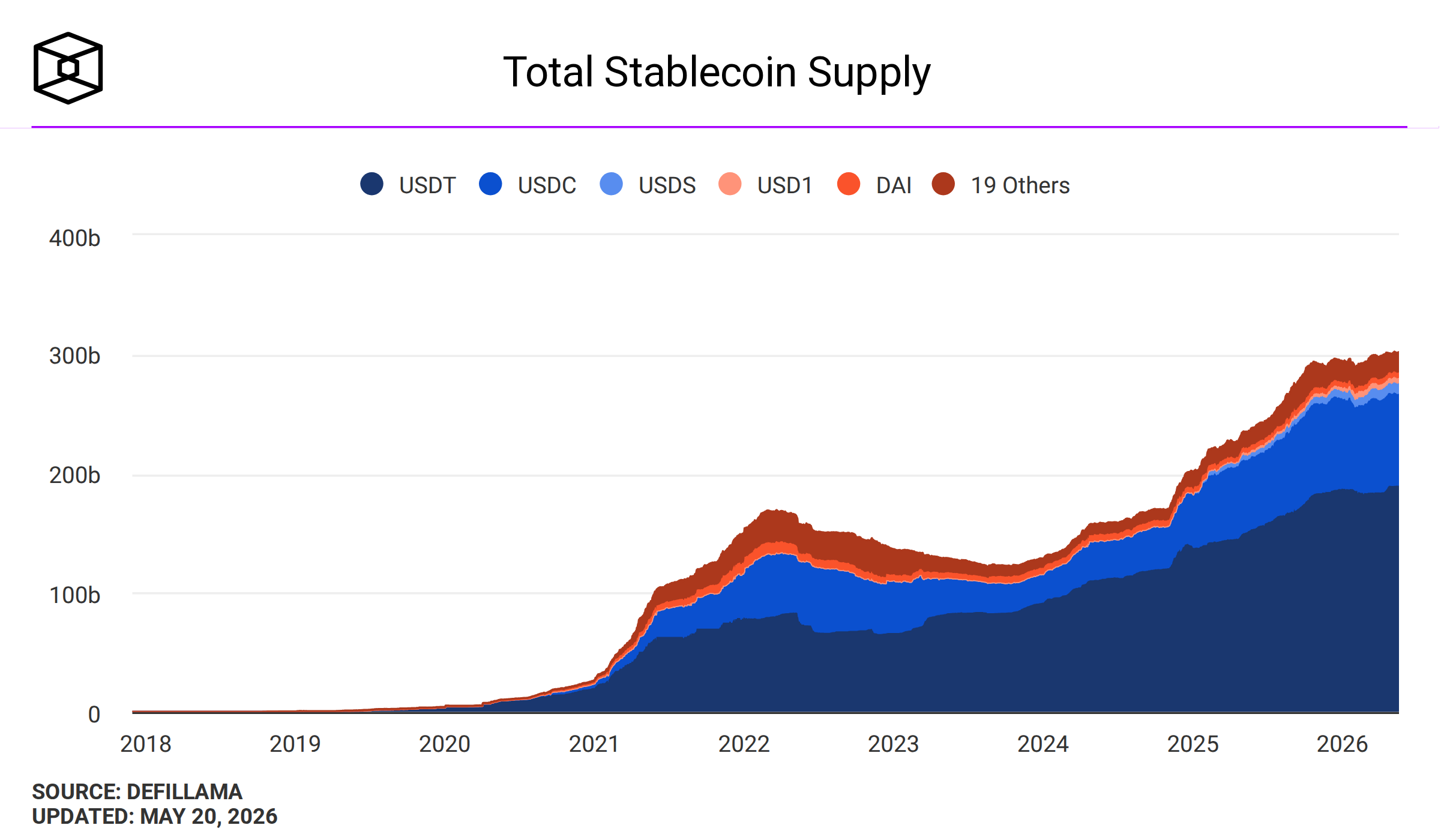

The stablecoin market briefly crossed a historic milestone as USDT briefly overtook Ethereum in market cap (both ~$187B), signaling massive institutional adoption. Despite duopoly pressures, USDT and USDC continue to dominate, though emerging competitors and DeFi yield products are intensifying competition. Regulatory compliance gaps persist globally, with no single U.S. federal stablecoin statute enacted as of June 2026.

Stablecoin Monitor — 2026-06-15

Market Snapshot

| Stablecoin | Market Cap (Est.) | 24h Change | Peg Status |

|---|---|---|---|

| USDT (Tether) | ~$187B | +0.5% | ✓ Stable |

| USDC (Circle) | ~$77B | Flat | ✓ Stable |

| DAI (MakerDAO) | ~$4.7B | Flat | ✓ Stable |

| USDe (Ethena) | Growing (yield-bearing) | — | ✓ Stable |

| PYUSD (PayPal) | Declining | -35% (from recent highs) | ✓ Stable |

Note: For live data, consult DeFi Llama or The Block's stablecoin dashboards.

Key Developments

USDT Briefly Overtakes Ethereum in Market Value For a few hours earlier this week, Tether's USDT held a higher market cap than Ethereum ($187B vs. $183–188B range across trackers), marking the first time in eight years a stablecoin has surpassed Ethereum by valuation. The crossover underscores the explosive growth in institutional stablecoin adoption and on-chain dollar demand.

Hyperliquid Records $4B USDC Inflow—Liquidity Surge Hyperliquid saw record stablecoin inflows, with $4 billion in USDC flowing into the derivatives exchange. The massive liquidity injection signals growing institutional interest in decentralized derivatives and sustained demand for on-chain dollar settlement.

Ethena & Coinbase Launch USDe High-Yield Vault on Morpho Ethena and Coinbase introduced a Steakhouse High Yield Vault offering DeFi yield directly within the Coinbase app, bringing yield-bearing stablecoins closer to mainstream retail users. This partnership signals the mainstreaming of yield-based stablecoin products.

Regulatory & Compliance Tracker

U.S.: No Federal Stablecoin Statute Enacted (As of June 2026) The United States continues to regulate stablecoins through overlapping state and federal authorities. Multiple bills, including the proposed GENIUS Act, have advanced but no single comprehensive federal stablecoin law has been enacted. Key requirements under various frameworks include 1:1 reserve backing in U.S. dollars or Treasury instruments, monthly audited reserve reports, and instant redemption rights for issuers.

EU & Global: MiCA in Effect; Tether Avoided Authorization The EU's Markets in Crypto-Assets Regulation (MiCA) is now in force, requiring stablecoin issuers to obtain authorization and maintain full reserves. Notably, Tether (USDT) did not seek MiCA authorization, while Circle's USDC and PayPal's PYUSD have pursued full compliance. Algorithmic stablecoins are excluded from most major regulatory frameworks due to lack of full reserve backing.

On-Chain & DeFi Pulse

Stablecoin Yields Climbing: DeFi Platforms Competing on Rates Yield-bearing stablecoins (USDe, Sky, Ondo) are driving a multi-billion-dollar competitive segment. Ethena's USDe leverages basis trading yield; Sky (formerly MakerDAO) distributes protocol surplus; Ondo distributes Treasury yield. Stablecoin lending platforms (Aave, Morpho, Compound, Spark) are offering yields up to 15% APR on various stablecoins, pulling liquidity into DeFi.

PYUSD Loses 35% of Market Cap Despite Circle's USDC Strength PayPal's PYUSD saw a significant decline, dropping 35% of its stablecoin-denominated capital, while Circle's USDC made one of the largest single transfers in history. This consolidation reflects ongoing market concentration around the USDT-USDC duopoly despite new entrants.

Analysis: What It Means

The brief overtaking of Ethereum by USDT signals a watershed moment for stablecoins as critical financial infrastructure. The $300B+ stablecoin market is no longer a niche crypto asset class—it now rivals or exceeds the market value of major blockchain networks. This reflects genuine institutional demand for on-chain dollar settlement, cross-border payments, and DeFi collateral.

However, the market remains heavily concentrated. Despite warnings from investors like Dragonfly's Rob Hadick that competition will eventually break the USDT-USDC duopoly, these two tokens control roughly 90% of the USD-pegged stablecoin supply. Emerging competitors (USDe, PYUSD, GHO) are growing, but PYUSD's 35% decline and USDT's continued dominance underscore the staying power of first-mover advantage and liquidity concentration.

The real innovation is shifting toward yield-bearing stablecoins and DeFi integration. Ethena-Coinbase's partnership is a critical inflection point: bringing DeFi yields into mainstream custody (Coinbase) makes stablecoin returns accessible to retail users, not just protocol sophisticates. This trend will likely drive further consolidation around yield-optimized products rather than marginal stablecoin issuers.

Regulation remains fragmented. The U.S. lacks a single federal framework, the EU has MiCA (with Tether notably absent), and Asia is developing parallel regimes. This regulatory patchwork creates arbitrage opportunities but also compliance costs that favor large, well-capitalized issuers like Circle and PayPal.

What to Watch Next

- U.S. Stablecoin Bill Progress: No federal bill is law yet; watch for legislative movement in Congress over the next 6 months. The GENIUS Act and competing proposals may face final votes.

- Tether's Reserve Audits: USDT leadership, despite regulatory scrutiny, depends on transparent reserve attestations. Quarterly audits are critical credibility markers.

- DeFi Yield Compression: As more capital flows into USDe vaults and Morpho, yields will compress. Monitor whether yield-bearing stablecoins remain competitive as basis trading normalizes.

- Stablecoin Cross-Chain Migration: Watch for further consolidation on Ethereum, Solana, and Polygon as users chase yield and liquidity; the Block's cross-chain supply metrics are a key leading indicator.

- New Entrant Viability: GHO (Aave's stablecoin), SKY (MakerDAO's tokenomics shift), and other protocol-issued stablecoins will face survival tests in the next 12 months.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by