Streaming Wars — 2026-05-16

Paramount Skydance is pressing its case that without the Warner Bros. Discovery merger, neither Paramount+ nor HBO Max can realistically close the gap on Netflix, Disney, or Amazon — a regulatory argument that reshapes the competitive map. Disney's streaming segment posted $582 million in operating income for Q2 fiscal 2026, an 88% year-over-year surge, cementing Josh D'Amaro's debut quarter as a landmark. Viewers and analysts alike are watching whether rising subscription prices — Netflix's standard ad-free plan now sits at $20/month — will finally push mass cancellations or simply accelerate the migration to cheaper ad-supported tiers.

Streaming Wars — 2026-05-16

Today's Headlines

-

Paramount+ / Max — Merger Justification Goes Public: Paramount Skydance filed regulatory arguments asserting that without the Warner Bros. Discovery merger, neither Paramount+ nor HBO Max can realistically compete with Netflix, Disney, or Amazon at scale. The combined entity, the company argues, would bring "new competitive energy to the entertainment ecosystem." If approved, the deal would create a genuine third-place challenger to the streaming duopoly.

-

Disney — Q2 FY2026 Earnings Beat on Streaming Surge: Disney's streaming segment (Disney+ and Hulu combined) generated $582 million in operating income in the second fiscal quarter of 2026, up 88% year-over-year, while total company revenue rose 7%, beating Wall Street estimates. It marks the first full quarter under new CEO Josh D'Amaro. The result signals that Disney's painful streaming transition is paying off, with profitability now a durable trend rather than a one-quarter anomaly.

-

Netflix — $20 Standard Plan Signals Ad-Tier Endgame: Netflix's standard ad-free plan has reached $20/month, and analysts note the economics of the cheaper ad-supported tier are now approaching parity with premium plans in per-subscriber revenue. The pricing move is accelerating what CNBC describes as streaming's "tipping point into old TV."

-

WBD / Multiple Platforms — Subscriber Disclosure Era Ending: Warner Bros. Discovery has joined Netflix and Disney in scrapping quarterly subscriber disclosures. Meanwhile, Comcast executives said Peacock is "approaching" profitability next quarter. The transparency retreat makes third-party measurement and advertising negotiations significantly more complex for the industry.

-

Cord Cutters — Streaming Deals Roundup Updated (May 15): Cord Cutter Weekly's comprehensive list of live streaming deals was updated on May 15, 2026, noting that in a competitive 2026 market "there should be ways to do better than sticker price" through bundles, promotions, and cashback options. As prices rise, deal-hunting behavior is intensifying among subscribers.

thewrap.com

variety.com

variety.com

variety.com

How the Streamers Stack Up in Subscribers, Revenue and Profits | Analysis

How the Major Streamers Stack Up in Subscribers, Revenue

How the Major Streamers Stack Up in Subscribers and Revenue

Subscriber & Revenue Snapshot

-

Netflix: Standard plan now $20/month ad-free. Ad-supported subscribers are generating revenue approaching premium-tier parity per user, per CNBC analysis (May 10, 2026). Netflix stopped disclosing subscriber counts quarterly; the most recent public figure placed global subscribers well above 300 million.

-

Disney+ / Hulu: Streaming operating income hit $582 million in Q2 FY2026 (quarter ended ~April 2026), up 88% year-over-year. Total Disney company revenue rose 7%, beating Wall Street estimates. Disney stopped reporting subscriber counts as of Q1 2026, following Netflix's lead.

-

Max (WBD): WBD has joined Netflix and Disney in eliminating quarterly subscriber disclosures as of May 2026. The company had previously forecast reaching at least 150 million subscribers globally by end of 2026 through Max's international expansion. Most recent disclosed figure: not available post-disclosure change.

-

Paramount+: Q1 2026 earnings met most Wall Street targets but subscriber gains at Paramount+ "fell slightly short" of expectations, per Deadline (published ~2 weeks ago, within context window for background). The most recent disclosed global subscriber figure from November 2025 stood at 79.1 million.

-

Peacock (Comcast): Comcast executives stated Peacock is "approaching" profitability next quarter (as of May 2026 reporting). Hard subscriber numbers were not disclosed in the most recent update.

Content Battleground

Most-Watched This Week

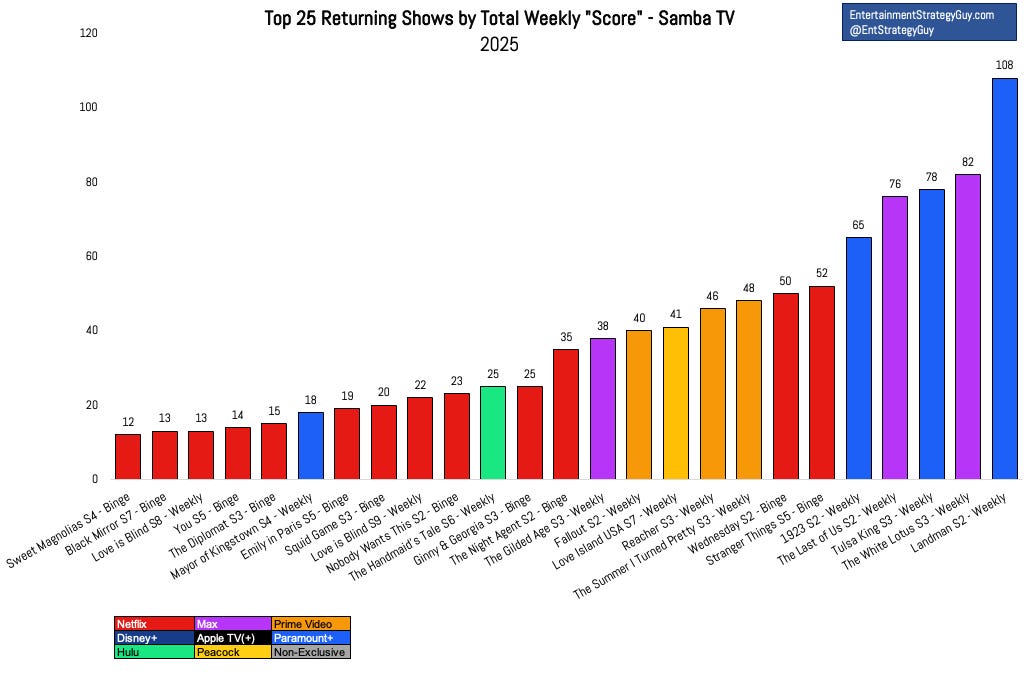

A new Samba TV / Luminate / Nielsen synthesis published May 15, 2026 reviewed the year's biggest streaming performers and current rankings:

-

Wednesday (Netflix) — Cited alongside Untamed as one of the "giant hit shows" of the current streaming cycle, with strong Samba TV and Nielsen performance confirmed in the latest annual streaming ratings analysis.

-

Untamed (Netflix) — Ranked alongside Wednesday as a standout performer across Samba TV, Luminate, and Nielsen metrics in the 2025–2026 streaming season, per the May 15 Entertainment Strategy Guy / Substack analysis.

-

Landman (Paramount+) — Highlighted as a show that challenged Netflix's streaming dominance on Samba TV charts; the analysis notes it "comes for Netflix's streaming crown" and spent multiple weeks in the top ten, peaking at #2 overall.

Notable Releases & Renewals

-

Paramount+ / Max Merger Content Case — Paramount+/Max: Paramount Skydance's regulatory push argues that combined content libraries and production scale are essential to compete. If approved, the deal would reshape which originals land on which platform and could accelerate catalog consolidation.

-

Streaming Bundle Deals Refresh — Multiple platforms: Cord Cutter Weekly updated its comprehensive streaming deals list on May 15, 2026, noting that annual plans, bundles, promotions, and third-party cashback options can materially undercut sticker prices in the current competitive environment.

-

The Last of Us Season 2 (HBO/Max) — Max: Per the May 15 streaming ratings analysis, The Last of Us "opened big" but had a "low completion rate and seemed to disappoint its fans," making it a notable 2025 under-performer despite large opening-week Samba TV numbers.

Strategic Moves

-

Subscriber Disclosure Blackout — Netflix, Disney, WBD: All three have now ended quarterly subscriber count disclosures. The industry-wide retreat from transparency shifts competitive intelligence to third-party firms (Nielsen, Samba TV, Luminate) and makes it harder for advertisers and investors to benchmark platform health. Peacock and Paramount+ remain the last major players still reporting some subscriber data.

-

Netflix Ad-Tier Price Ladder Push — Netflix: The $20 ad-free standard plan is designed to nudge subscribers toward the lower-cost ad-supported tier, where Netflix now generates comparable revenue per user through advertising. Analysts describe this as Netflix deliberately engineering a "tipping point into old TV" — mirroring cable's dual revenue model of subscriptions plus ads.

-

Paramount+/Max Merger Regulatory Push — Paramount+, Max (WBD): Paramount Skydance is actively lobbying regulators, arguing the merger is pro-competitive. The argument: scale is a prerequisite for survival against Netflix and Disney, and a combined Paramount+/Max entity is the only realistic path to closing the gap.

-

Peacock Profitability Milestone Approaching — Peacock (Comcast): Comcast executives publicly stated Peacock is "approaching" profitability next quarter — a significant signal for a service that has been a sustained money-loser. If it achieves breakeven, it removes a major overhang on Comcast's stock and validates the sports-heavy content strategy.

Platform Scorecard

| Platform | Today's News | Momentum |

|---|---|---|

| Netflix | $20 standard plan accelerates ad-tier migration; subscriber disclosures ended | → Stable dominance, but price resistance building among loyal subscribers |

| Disney+ / Hulu | $582M streaming operating income in Q2 FY2026, up 88% YoY | ↑ Strongest profitability signal yet under new CEO D'Amaro |

| Max | Joined Netflix/Disney in ending subscriber disclosures; merger case active | → Awaiting merger outcome; disclosure blackout clouds visibility |

| Amazon Prime Video | No new data published after 2026-05-14 | → No fresh catalyst this cycle |

| Apple TV+ | No new data published after 2026-05-14 | → No fresh catalyst this cycle |

| Paramount+ | Merger regulatory arguments public; subscriber gains slightly below expectations | ↓ Dependent on WBD deal approval for long-term viability per own argument |

| Peacock | "Approaching" profitability next quarter per Comcast execs | ↑ Closest to a breakeven milestone in service history |

Viewer Verdict

-

"I'm done with the constant price hikes. After years of loyalty, I'm out and finally cancelled. The content isn't even that…" — r/cordcutters

-

"Their goal is to drive most or all subscribers to the ad-supported plans. Then they'll raise those prices and it will be cable TV all over again." — r/netflix

-

"In 2026 the streaming market is competitive enough that there should be ways to do better than sticker price" through bundles, promotions, and cashback options. — r/cordcutters

Market Analysis

Disney is the clearest winner of the current moment. An 88% jump in streaming operating income — to $582 million in a single quarter — is not a rounding error; it signals that the painful, loss-generating build phase is over and that Disney's dual-platform strategy (Disney+ for franchises, Hulu for general entertainment) is generating genuine returns. CEO Josh D'Amaro's debut quarter sets a high bar, and investor sentiment is likely to remain constructive as long as streaming income holds.

Netflix continues to play a longer, more complex game. The $20 standard ad-free tier is structurally designed to make the ad-supported plan look like the rational choice — and the economics now support that thesis, with ad-tier ARPU approaching parity. The strategic endgame, as Reddit users have bluntly identified, resembles the old cable bundle: dual revenue from subscriptions and advertising. The critical question is whether the price elasticity ceiling has been reached, given the wave of cancellation sentiment visible on social platforms.

The merger chess match between Paramount+ and WBD is the biggest structural wildcard. Both companies have now publicly admitted — in regulatory filings — that they cannot independently close the gap on the top three. That admission is extraordinary and changes how advertisers, content partners, and talent will weigh commitments to either platform. The disclosure blackout spreading across Netflix, Disney, and now WBD simultaneously makes it harder to track who is actually winning the subscriber race in real time, shifting power to whoever controls third-party measurement data.

What to Watch Next

-

Next quarter (Q3 FY2026 ~August) — Disney streaming profitability follow-through: Investors will watch whether the $582M Q2 result is sustainable or inflated by seasonal content. A second strong quarter would cement the turnaround narrative.

-

Pending regulatory decision — timeline TBD — Paramount+/WBD merger ruling: Regulators will respond to Paramount Skydance's competitive-necessity argument. Approval reshapes the entire mid-tier of the streaming market; rejection forces both companies into standalone survival mode.

-

Next quarter (Comcast Q2 2026 earnings ~July) — Peacock profitability milestone: Comcast executives have telegraphed breakeven is "approaching." Confirmation would mark the end of the last major streaming service running at a sustained operating loss.

Reader Action Items

-

For subscribers: If you're on Netflix's $20 ad-free standard plan, check whether the ad-supported tier now offers everything you watch — the content gap has narrowed significantly and the price differential has widened. Cord Cutter Weekly's May 15 deals list is worth checking for live bundle discounts that can undercut sticker prices.

-

For investors and industry watchers: Disney's 88% streaming income surge makes it the strongest near-term trade in legacy media streaming. The Paramount+/WBD merger outcome is the highest-stakes binary event in the sector — regulatory filings are now the most important documents to track.

-

For content creators and producers: The disclosure blackout at Netflix, Disney, and WBD means third-party viewership data (Nielsen, Samba TV, Luminate) is becoming the de facto negotiating currency for talent and licensing deals. Familiarity with those metrics is now a material business skill.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by