Stablecoin Monitor — 2026-05-14

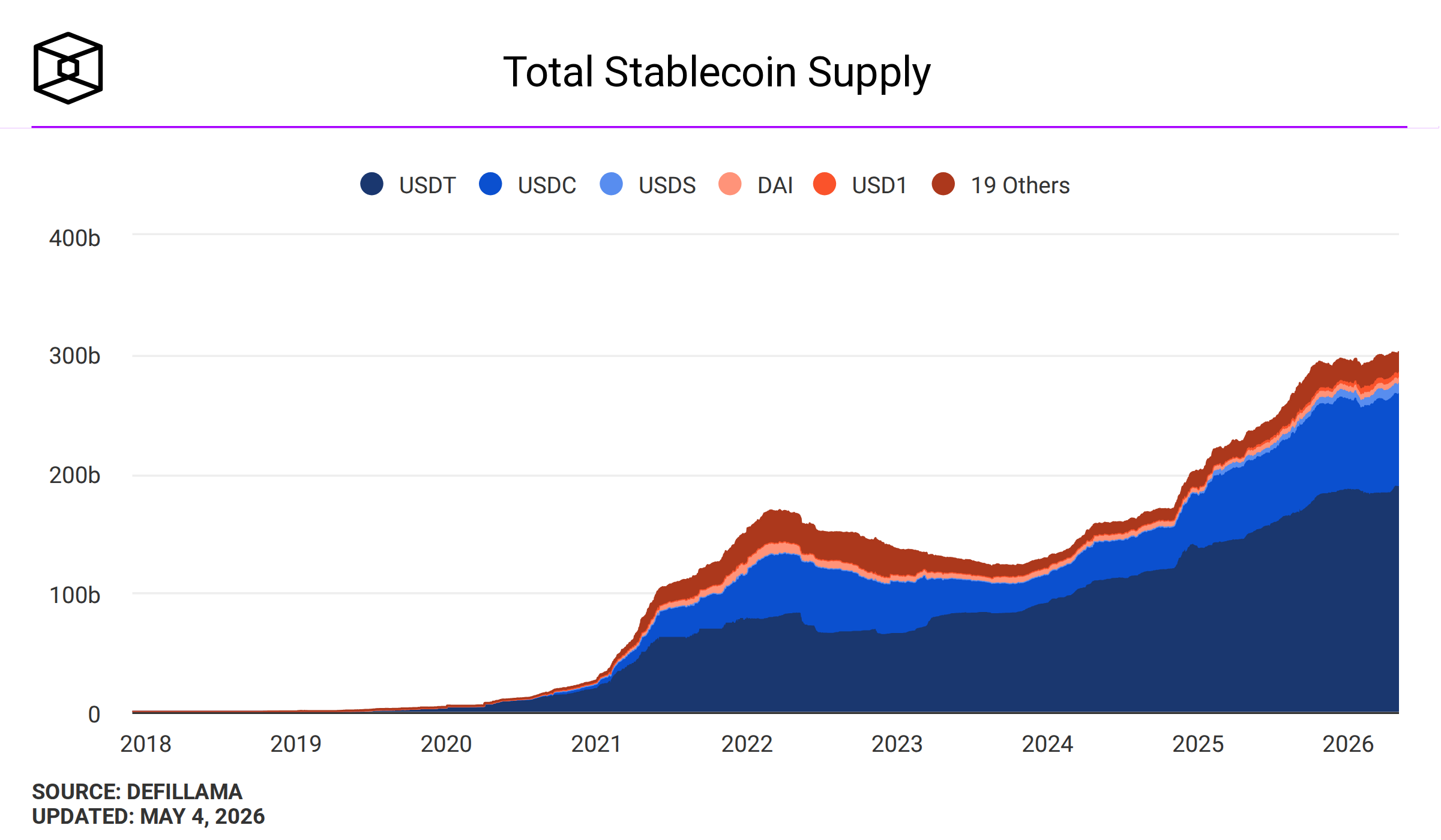

The total stablecoin market cap has crossed $321 billion, holding near all-time highs set at the end of April, with USDT maintaining dominance while USDC continues to gain transaction volume. Circle reported a dip in Q1 revenue and profit despite a $222M presale of its new ARC token, signaling a shift in its revenue strategy. On the regulatory front, Tether's USDT faces continued MiCA non-compliance pressure in Europe, while the US GENIUS Act advances as a leading federal stablecoin framework.

Stablecoin Monitor — 2026-05-14

Market Snapshot

The stablecoin market recently hit a new all-time high of $321 billion, capping April with a 1.63% monthly gain — the third consecutive end-of-month record, per CoinDesk's Stablecoins and Tokenized Asset Report.

| Stablecoin | Market Cap (approx.) | Peg Status | Notes |

|---|---|---|---|

| USDT (Tether) | ~$189.6B | Stable ($1.00) | Dominance intact; MiCA compliance issues in EU |

| USDC (Circle) | ~$77.6B | Stable ($1.00) | Growing transaction volume; Q1 revenue dipped |

| DAI (MakerDAO) | ~$4.7B | Stable ($1.00) | Decentralized, overcollateralized |

| FDUSD | Est. top-5 | Stable ($1.00) | Active on Binance ecosystem |

| USDe (Ethena) | Tracking | Stable ($1.00) | sUSDe supply down 49% over 90 days; institutional shift underway |

Key Developments

1. Circle Q1 Revenue Falls Despite $222M ARC Token Presale

Circle reported that Q1 USDC revenue and profit declined, but the company's presale of its new ARC token generated $222 million, partially offsetting the shortfall. USDC nonetheless posted gains in market share and transaction volume during the quarter, suggesting the underlying utility of the stablecoin remains strong even as interest income softens.

2. Jupiter Taps Bitwise for Institutional USDe Lending Market on Solana

Jupiter Lend, in partnership with Fluid and Bitwise, launched an institutional-grade lending market for Ethena's USDe synthetic stablecoin on Solana. The move is designed to create a regulated, curated venue for institutional yield-seeking on Solana, marking a step toward bridging DeFi liquidity with institutional capital flows around USDe.

3. Stablecoins in 2026: Becoming Crypto's Biggest Story

A new analysis from Crypto Daily describes stablecoins as "crypto's biggest story" in 2026, citing the $321B market cap milestone and the sector's increasing role in cross-border payments and DeFi infrastructure. The piece notes that stablecoins now settle more value annually than Visa and Mastercard combined, reflecting a structural shift in global finance.

Regulatory & Compliance Tracker

EU — MiCA Compliance Pressure Intensifies on Tether

Tether's USDT remains non-compliant with the EU's Markets in Crypto-Assets (MiCA) regulation, which governs Asset-Referenced Tokens (ARTs) and E-Money Tokens (EMTs). MiCA requires strict reserve requirements, whitepaper disclosures, and authorization processes for stablecoin issuers. Because Tether's reserve composition and audit transparency do not meet these standards, multiple European exchanges have restricted or removed USDT for EU users. The regulatory split is increasingly forcing users and institutions operating in Europe toward MiCA-compliant alternatives.

US — GENIUS Act Emerges as Leading Federal Framework

As of mid-May 2026, no single federal stablecoin statute has yet been enacted in the United States, but the GENIUS Act has emerged as the leading bill moving through Congress. The proposed law would require 1:1 reserves in U.S. dollars, short-term Treasury bills, overnight repos, or Federal Reserve credits. It mandates monthly reserve reports audited by registered accounting firms, with criminal penalties for executives in the event of non-compliance. Algorithmic stablecoins — lacking full reserve backing — are excluded from the framework's protections, consistent with MiCA's approach.

On-Chain & DeFi Pulse

Ethena's sUSDe Supply Drops 49% in 90 Days — Capital Rotates to RWA-Backed Yield

A new Tiger Research report highlights a significant structural shift within DeFi's yield-bearing stablecoin landscape. Ethena's sUSDe supply has fallen 49% over the past 90 days, as capital rotated toward lower-yielding but more predictable instruments like USYC and sUSDS. The report concludes that raw APY is no longer the primary driver of stablecoin allocation — collateral composition, institutional adoption, and return predictability are now the defining factors. This signals a maturation of the yield-bearing stablecoin segment from speculative to institutional-grade.

CoinGecko 2026 RWA Report Maps the Six Largest Stablecoins Across Two Tracks

CoinGecko's latest RWA report, published within the past 48 hours, compares the six largest stablecoin issuers across backing, transparency, regulation, and yield — identifying a clear split between regulated fiat-backed stablecoins and yield-bearing synthetic/DeFi instruments. This "two tracks, one regulatory split" framing is increasingly influencing how institutional allocators approach stablecoin portfolios.

Analysis: What It Means

The stablecoin market's push past $321 billion is not accidental — it reflects a confluence of structural tailwinds. Regulatory clarity (or the pursuit of it) is pushing capital toward compliant instruments, as evidenced by the MiCA squeeze on USDT in Europe and the GENIUS Act's momentum in the US. Circle's Q1 revenue dip tells a nuanced story: traditional interest income from reserve portfolios is compressing, but USDC's transaction volume is growing, suggesting that the utility model — not just the yield model — is what sustains long-term stablecoin adoption.

The DeFi landscape is undergoing its own maturation. The sharp 49% decline in Ethena's sUSDe supply over 90 days is a bellwether. Institutions are no longer chasing the highest APY; they want predictable, auditable returns backed by real-world assets. The capital rotation from sUSDe into USYC and sUSDS reflects a preference for composability and risk-adjusted stability over raw yield. Jupiter's partnership with Bitwise to create an institutional USDe lending market on Solana is a direct response to this shift — building the regulated infrastructure institutional DeFi requires.

Together, these trends paint a picture of an industry at an inflection point. The "two tracks" identified by CoinGecko — regulated fiat-backed stablecoins on one side, yield-bearing synthetic instruments on the other — will increasingly diverge as regulatory frameworks solidify. The winners will be issuers who can offer compliance and yield, or at minimum, compliance and sufficient liquidity to justify institutional trust.

What to Watch Next

- US GENIUS Act progress: Senate movement on the bill could trigger immediate reactions in USDC and USDT supply dynamics; watch for committee votes or floor scheduling in the coming weeks.

- Tether's MiCA response: Whether Tether pursues European licensing or formally cedes EU market share to compliant competitors (likely Circle and Société Générale's EURCV) will be a defining story for Q2 2026.

- Circle ARC token trajectory: The $222M presale is a fundraising milestone, but how ARC integrates with USDC's infrastructure — and whether it faces securities scrutiny — remains to be seen.

- Ethena sUSDe stabilization: Watch whether the 49% supply drop continues or reverses as DeFi funding rates shift; a recovery would signal renewed risk appetite in the basis trade.

- Jupiter/Bitwise USDe market performance: Early TVL and yield data from the new Solana-based institutional lending venue will be a live test of whether DeFi can truly attract institutional capital at scale.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by