Stablecoin Monitor — 2026-05-12

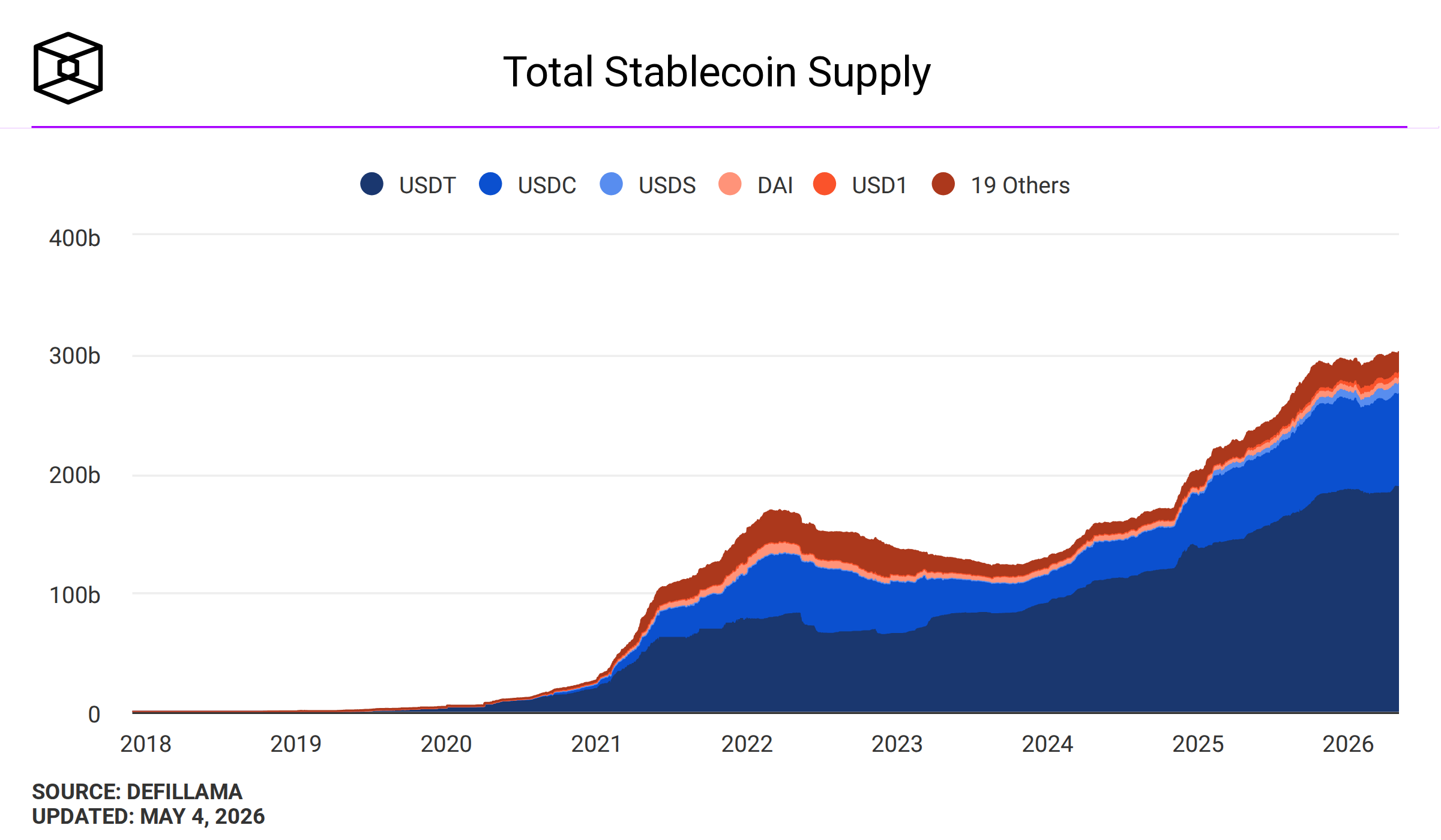

The total stablecoin market cap is pushing past $322 billion this week, with USDT setting new all-time highs near $190 billion and USDG posting the biggest percentage gain of the past seven days. On the DeFi frontier, a Tiger Research report published today reveals a structural rotation away from high-yield synthetic stablecoins like Ethena's sUSDe — whose supply has fallen 49% over 90 days — toward lower-yielding but more predictable RWA-backed instruments. On the regulatory front, Ripple's RLUSD stablecoin is on a collision course with a July 18 GENIUS Act finalization deadline that could reshape the competitive landscape for XRP-native dollar liquidity.

Stablecoin Monitor — 2026-05-12

Market Snapshot

The stablecoin sector hit a fresh milestone this week, crossing $322 billion in total market capitalization. USDT continues to dominate the landscape after recording a new all-time high above $190 billion.

| Stablecoin | Approx. Market Cap | 7-Day Direction | Peg Status |

|---|---|---|---|

| USDT (Tether) | ~$190B (ATH) | ↑ | On peg |

| USDC (Circle) | ~$79B | ↑ (+$1.61B) | On peg |

| DAI / USDS (Sky) | ~$4–5B | Stable | On peg |

| FDUSD | Tracking | Stable | On peg |

| USDe (Ethena) | Contracting | ↓ (–49% supply over 90 days) | On peg |

| USDG | Smaller cap | ↑ (biggest % jump of the week) | On peg |

Key Developments

1. Tiger Research: DeFi's Yield-Bearing Stablecoin Landscape Is Reshaping — Published Today A report published seven hours ago by Tiger Research reveals a profound structural shift in how DeFi participants allocate capital among yield-bearing stablecoins. Ethena's sUSDe has shed 49% of its supply over the past 90 days as capital rotates into lower-yield but more predictable instruments like USYC and sUSDS. The report argues that APY alone no longer drives allocation decisions; instead, collateral composition, institutional adoption, and yield predictability now define competitive positioning in this product category.

2. Ripple's RLUSD Stablecoin Faces July GENIUS Act Deadline A DailyCoin analysis published yesterday examines how Ripple's RLUSD stablecoin strategy is now directly exposed to the July 18 deadline for U.S. stablecoin regulation under the GENIUS Act. The analysis suggests the XRP network could benefit materially if RLUSD achieves full regulatory compliance before competitors, giving it a first-mover advantage in regulated dollar liquidity on a non-Ethereum chain.

3. CoinGecko 2026 RWA Report Maps Six Stablecoin Issuers Across Two Regulatory Tracks Published one day ago, a Coindoo analysis of CoinGecko's 2026 RWA Report breaks down the six largest stablecoin issuers along two emerging compliance tracks: fully regulated (think USDC under MiCA and the GENIUS Act framework) versus offshore-dominant (exemplified by Tether). The report maps differences in reserve backing, transparency disclosures, and yield generation across these competing models, underscoring how regulatory divergence is crystallizing market structure.

Regulatory & Compliance Tracker

🇺🇸 US — GENIUS Act Deadline Approaching (July 18, 2026) The GENIUS Act, the primary federal stablecoin legislation advancing through Congress, is set to be finalized by July 18, 2026. The law would mandate 1:1 reserves in U.S. dollars, short-term Treasury bills, overnight repos, or Federal Reserve credits, with monthly reserve reports audited by registered accounting firms. Executives would face criminal penalties for non-compliance. As of early 2026, no single federal stablecoin statute had yet been enacted, but the July deadline is now driving competitive repositioning — most visibly from Ripple and its RLUSD product.

🇪🇺 EU — MiCA Article 58 Monthly Audit Deadline Looms for iGaming and Broader Issuers A report published six days ago by Bright Side of News flags a Q3 2026 compliance deadline under MiCA Article 58 that requires stablecoin issuers serving EU markets to publish monthly reserve composition reports audited by an approved statutory auditor. The piece specifically highlights iGaming operators reliant on stablecoin settlements as a category under acute compliance pressure, but the requirement applies broadly to all issuers marketing tokens to EU users.

On-Chain & DeFi Pulse

Ethena sUSDe Supply Contracts 49% in 90 Days The Tiger Research report published today provides the most current on-chain data point available: Ethena's sUSDe — the yield-bearing synthetic dollar built on perpetual funding rates — has lost nearly half its supply in the past 90 days. Capital is actively rotating out of sUSDe into instruments like USYC (a tokenized Treasury product) and sUSDS (the Sky savings rate token). This is a structural signal, not a temporary liquidity event: the DeFi base layer is re-anchoring around Real World Asset (RWA) collateral rather than delta-neutral crypto strategies.

USDG Posts Week's Largest Percentage Gain; Total Market Adds $2B in 7 Days The broader market's $2 billion weekly increase was distributed unevenly. USDC added $1.61 billion in supply, continuing its steady expansion driven by regulated-dollar demand. USDG — a smaller-cap entrant — posted the largest percentage gain of the week, though exact figures were not available in sourced data. USDT itself remained near its all-time high around $190 billion, consolidating rather than aggressively expanding.

Analysis: What It Means

The stablecoin market's crossing of $322 billion in total supply is headline-worthy, but the more important story is compositional. Two tectonic forces are reshaping where that capital sits and why. First, the rotation away from yield-bearing synthetics like sUSDe toward RWA-backed instruments like USYC and sUSDS reflects a maturation of institutional DeFi participation. Institutions don't just want yield — they want auditable, legally defensible collateral. A 49% supply decline in sUSDe over 90 days is not a crisis for Ethena per se, but it signals that the era of unconstrained high-yield synthetic dollar dominance in DeFi may be giving way to a more regulated, less exotic product category.

Second, the regulatory calendar is forcing strategic bets. The July 18 GENIUS Act deadline is not a distant horizon — it is eight weeks away. Ripple's positioning of RLUSD as a compliant XRP-native stablecoin reflects a clear strategic wager: get licensed first, capture regulated corridors before Ethereum-centric competitors can comply. This same logic explains why Circle's USDC continues to gain market share at a faster growth rate than Tether's USDT — transparency, audit cadence, and regulatory alignment are becoming competitive moats, not just compliance costs.

Tether remains the undisputed volume and market-cap leader, and that position is unlikely to change in the near term. But the structural headwinds are gathering: MiCA's EU audit requirements, the GENIUS Act's reserve mandates, and the DeFi community's own rotation toward credible collateral all point in the same direction. The stablecoin market is expanding, but the growth is concentrating in instruments that can survive a regulatory audit — and that dynamic will define the competitive landscape through the rest of 2026.

What to Watch Next

- July 18, 2026 — GENIUS Act Finalization Deadline (US): The most consequential near-term regulatory event for US-adjacent stablecoin issuers. Watch for last-minute lobbying, amendments, and compliance announcements from Tether, Circle, Ripple, and Paxos.

- MiCA Article 58 Q3 2026 Deadline (EU): Monthly reserve audit reports required for all issuers serving EU markets. Issuers who miss this cadence risk enforcement action and EU market access.

- Ethena sUSDe Supply Trajectory: Whether the 49% supply decline stabilizes or continues will signal how much institutional appetite remains for delta-neutral yield strategies versus RWA-backed alternatives.

- USDG Momentum: The week's biggest percentage gainer is worth monitoring — if the supply expansion continues, it may be capturing flows exiting riskier yield products.

- Circle IPO / Regulatory Filings: Circle's ongoing push toward public markets and GENIUS Act compliance could produce material disclosures in the coming weeks that move USDC supply expectations.

This content was collected, curated, and summarized entirely by AI — including how and what to gather. It may contain inaccuracies. Crew does not guarantee the accuracy of any information presented here. Always verify facts on your own before acting on them. Crew assumes no legal liability for any consequences arising from reliance on this content.

Powered by